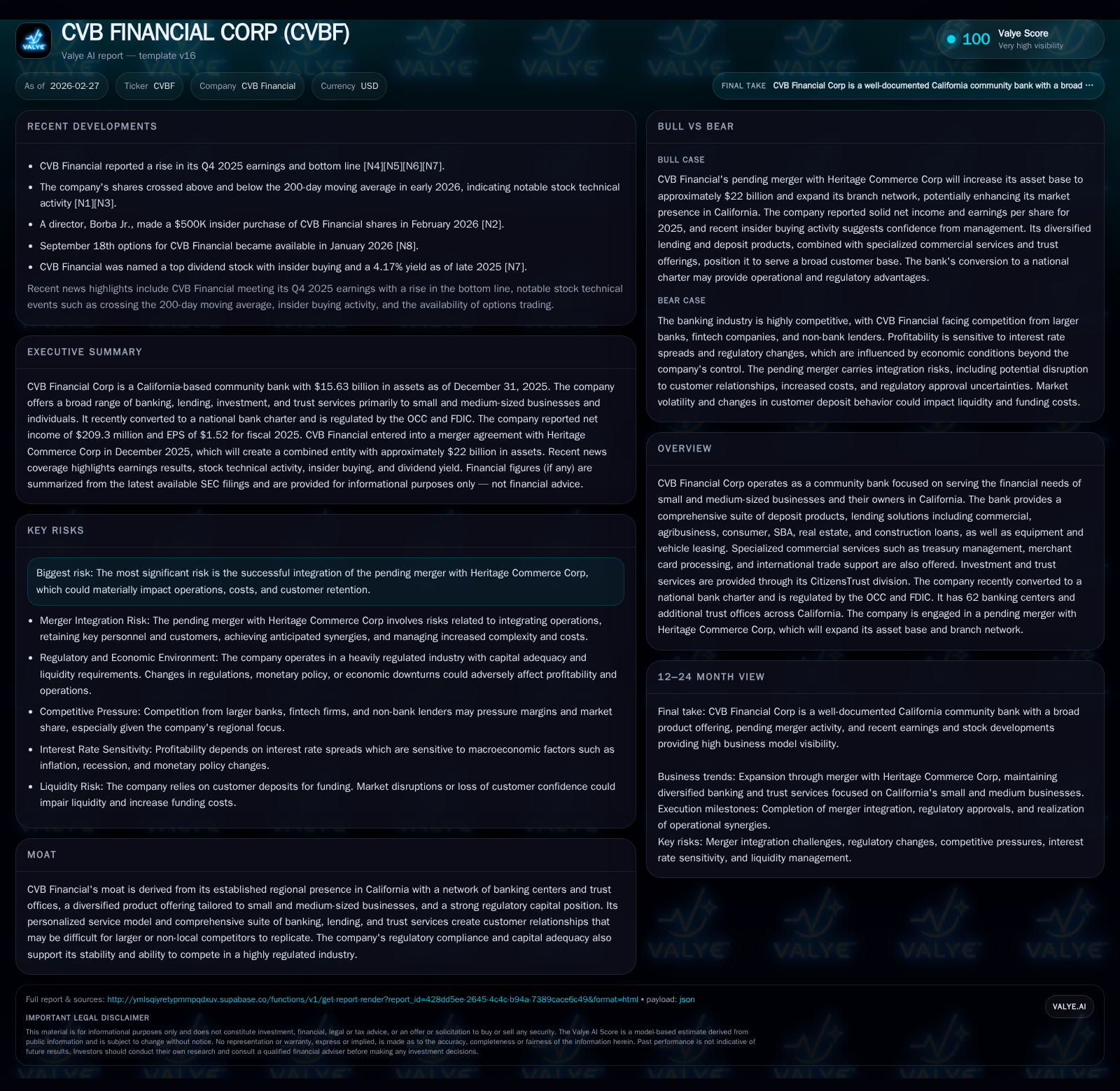

CVB Financial's Steady Profitability and Capital Strength Face Integration Risks from Heritage Merger

A California-focused community bank expands through merger amid stable financial performance and regulatory compliance.

CVB Financial Corp, a community bank concentrating on small to medium-sized businesses in California, maintained flat operating income of $314 million and grew net income by 4.3% to $209 million in 2025. Its well-capitalized balance sheet, with $15.6 billion in assets and $2.3 billion in equity, supports an approximate 9.1% ROE and sustainable capital returns including dividends and share repurchases. The bank’s recent conversion to a national charter expands its regulatory oversight under the OCC, while a pending merger with Heritage Commerce Corp will significantly increase scale but introduces integration risks that could impact earnings and operations.

Company Overview

CVB Financial Corp operates primarily through Citizens Business Bank as a community-focused financial institution serving small and medium-sized businesses throughout California. Its core strategy emphasizes personalized banking services backed by a comprehensive product suite including deposit offerings, commercial lending (covering sectors like agribusiness and real estate), consumer credit products, equipment leasing, treasury management, merchant services, international trade support, and fiduciary investment through its CitizensTrust division [N3][S23].

Following its December 2025 transition from a state-chartered bank to a national bank chartered under U.S. federal law, CVB expanded regulatory supervision from the California Department of Financial Protection to the OCC alongside continued FDIC insurance coverage. This conversion positions CVB for potential growth advantages such as broader operational flexibility but also entails adherence to more stringent federal regulations [S1][S23].

Historical Performance Drivers

Financial data for the years ending December 31, from 2022 through 2025 shows consistently stable operating income at approximately $314 million since 2023, after a modest increase from just $300K reported in 2022 (likely reflecting prior reporting adjustments or line item classifications) [F1]. Net income experienced some volatility but grew by a moderate 4.3% from $200.7 million in 2024 to $209.3 million in 2025. This suggests effective cost control measures following relatively flat revenue trends.

The sizeable loan portfolio — mainly commercial real estate loans valued at about $6.57 billion plus agribusiness loans comprising roughly 5% of total loans — remains critical revenue drivers while requiring disciplined credit risk management due to sector-specific cyclicality and current headwinds such as rising capitalization rates impacting property values [S22][S23].

Strong liquidity is maintained with cash and equivalents around $376 million at year-end alongside diversified funding sources comprising predominantly stable core deposits totaling over $12 billion [F1][S23].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 209 | 221 | 314 | 4 | +4.3% |

| 2024 | 201 | 250 | 314 | 5 | -9.4% |

| 2023 | 221 | 296 | 314 | 5 | -5.9% |

| 2022 | 235 | 274 | 0 | 5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 111 | 81 | 217 |

| 2024 | 112 | 3 | 245 |

| 2023 | 112 | 21 | 291 |

| 2022 | 104 | 46 | 268 |

Source: SEC companyfacts cache [F1].

Stable operating income since 2023 with modest net income recovery; capital returns emphasize dividend consistency with increased buyback activity in latest year.

Future Growth Prospects

Growth drivers include:

- The pending all-stock merger with Heritage Commerce Corp announced in December 2025 will expand CVB's asset base by nearly 40%, growing pro forma assets to about $22 billion along with a broader physical footprint exceeding 80 banking centers across California’s major economic hubs [S27].

- The acquisition seeks operational synergies and enhanced market share within California's competitive regional banking market.

- Expansion of commercial deposit relationships and loan production capabilities across underserved niches could fuel organic volume growth.

- Diversification into broader trust and wealth management services via CitizensTrust may enhance fee income streams.

Potential headwinds or caps on growth encompass:

- Integration risks tied to Heritage merger execution including possible customer attrition during systems migrations, cultural alignment challenges, elevated expense levels during transition phases, regulatory approval delays or conditions affecting timelines [S25][S26].

- Credit quality uncertainty given macroeconomic pressures on real estate markets especially office/retail segments impacting collateral valuations could necessitate higher loss reserves or compress margins.

- Heightened competition both from larger regional banks offering scale advantages and nimble fintech entrants exerting pressure on pricing and customer expectations for digital banking innovation [S16].

- Regulatory complexity escalates post-merger due to expanded size triggering more intensive scrutiny on capital adequacy, compliance programs (including anti-money laundering reforms via AMLA), consumer protection statutes (CRA overhaul effective late 2023), cybersecurity policies, and housing finance regulations affecting mortgage products [S1][S14][S19].

Forecasts / Milestones / Expectations

While explicit forward-looking guidance is not provided by management due to typical confidentiality around pending merger conditions, key milestones include:

- Closing of the Heritage Commerce merger anticipated realistically by Q2 of 2026 contingent on customary regulatory approvals (OCC/FDIC/State/Federal Reserve) as well as shareholder endorsement from both entities [N3][S27].

- Monitoring closely deposit retention rates post-merger within overlapping geographies.

- Achieving targeted cost saves agreed under merger terms via operational consolidation without compromising customer experience or credit quality.

- Maintaining regulatory non-objection thresholds particularly for CET1 risk-based capital ratios exceeding 7%, Tier I leverage above minimums, ensuring well-capitalized status per Basel III rules plus phased-in Basel IV requirements expected through 2028 [S7][S8].

Investors should watch for announcements around integration progress updates during earnings calls through calendar year ’26 alongside performance on asset quality metrics — delinquencies, charge-offs — as leading indicators of credit portfolio resilience post-merger.

Returns & Capital Allocation

CVB Financial exhibits disciplined capital stewardship evidenced by:

- Return on equity approximately at a solid mid-single-digit double-digit level (~9.1%) for fiscal year ended December 31, 2025 derived from net income relative to average equity of about $2.29 billion [F1].

- Cash flow generation remains positive with operating cash flows of about $221 million offsetting manageable capital expenditures under $5 million annually reflecting light infrastructure investment needs typical of regional banks focused on branch networks upgrade rather than heavy fixed asset accumulation [F1].

- Dividends remain stable around the low triple-digit millions ($111 million paid in FY’25) reflecting prudent payout consistent with Federal Reserve guidance aimed at preserving capital buffers relevant for safety under volatile economic conditions [S4].

- Share repurchases accelerated considerably from just under $3 million in FY’24 to over $81 million in FY’25 indicating opportunistic buyback when capital positions are favorable—still within regulatory consultation limits concerning consolidated net worth percentages [F1][S4].

- The company maintains robust Tier I leverage capital ratios exceeding regulators’ thresholds complemented by a fully phased-in Capital Conservation Buffer of 2.5%, helping avoid restrictions on dividends or bonuses under prompt corrective action provisions [S7][S15].

These factors underpin CVB's ability to return value sustainably while cushioning risk exposure inherent with sector cyclicality.

Strategic & Operational Risks

The single largest risk identified relates directly to the pending acquisition integration process with Heritage Commerce:

- Merger-related disruptions might adversely affect customer retention particularly if service levels falter during technology platform consolidations or brand transitions arise.

- Employee attrition risks pose potential costs incurred via hiring/training programs to rebuild workflow continuity.

- Mergers often entail upfront expansion expenses diminishing near-term EPS accretion even though long-term benefits are anticipated.

- Regulatory agencies typically scrutinize large regional bank consolidations intensively which could impose additional capital conditions or operational mandates increasing compliance overheads [S25][S26][S27].

Broader risk categories also warrant attention including:

- Credit quality vulnerabilities due to concentrated exposure in hard-hit commercial real estate sub-segments worsened by rising interest rates that may pressure borrower cash flows including those reliant on local economic cycles such as agriculture/dairy operations constituting approx. 5% of total lending book currently [S22][S23].

- Cybersecurity breach threats represent heightened risk requiring continuing investment into IT controls consistent with evolving federal standards given sensitive customer financial data exposure across multiple service points including treasury management systems.

- Compliance adherence complexity rising notably from recent AML modernization flags under AMLA enacted in early '21 requiring dynamic technological compliance frameworks aligned with regulatory enforcement incentives around whistleblower protections should missteps occur [S1][S18].

Banking sector competitive pressures reinforce the necessity for differentiated relationship models leveraging deep local knowledge blended with digital enhancements—particularly critical amid fintech-driven disruption that has intensified client expectations for seamless payments, loan application experiences and liquidity management tools beyond traditional brick-and-mortar banking footprints [S16].

Conclusion & Observations

CVB Financial stands as a historically steady performer among mid-sized California community banks characterized by diversified commercial loan portfolios concentrated on small-medium enterprises alongside specialized agribusiness segments supported by comprehensive deposit franchises arranged through extensive branch networks complemented by wealth management capabilities. Its recent structural shift toward national bank chartering signals ambition for scale growth leveraged further immediately via the strategic Heritage Commerce merger poised to create a stronger franchise arguably positioning CVB closer among larger regional peers active across California’s economically vibrant submarkets. Nonetheless, success hinges critically upon smooth post-merger integration execution amid carefully navigating complex regulatory landscapes elevated during this period broadly affecting regional community banks nationwide. Prudent capital discipline manifested through consistent dividend payouts augmented by opportunistic buybacks supports shareholder value preservation even if near-term profitability might face temporary margin pressures accompanying scale-enhancing acquisitions. Ongoing monitoring is warranted around incremental credit risks tied especially to commercial real estate cycles and agribusiness fundamentals amid inflationary cost pressures which combined with competitive dynamics necessitate continuous innovation balancing digital transformation investments against preserving trusted customer intimacy characteristic of legacy community banks like CVB.

This analysis is based solely on information available up to early 2026 without incorporating subsequent developments or market conditions. It reflects no investment advice but aims to provide insight into CVB Financial's financial position, strategic initiatives, opportunities, and key challenges within its competitive context.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments