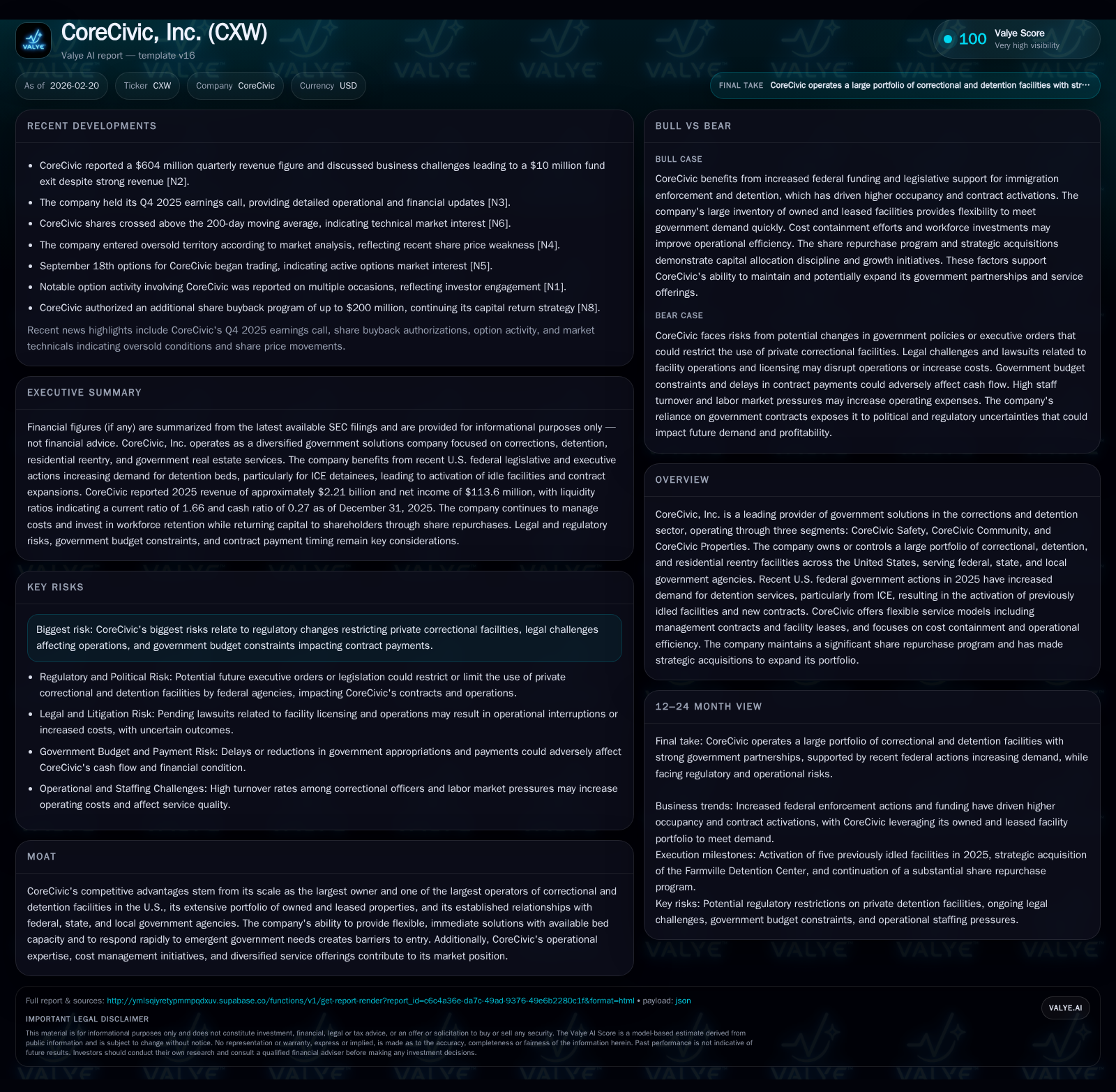

CoreCivic Expands Capacity Driven by Federal Policy Shift and Facility Activations

CoreCivic leverages regulatory tailwinds and asset deployment to accelerate growth and capital returns.

CoreCivic, Inc. has benefited from U.S. federal government policy changes enacted in 2025 which increased demand for detention services, particularly through ICE, leading to the activation of idle facilities and new contract wins. The company’s historical growth has been fueled by strategic acquisitions and operational efficiencies, with revenues growing over 12% in 2025. Capital expenditures surged in 2025 as CoreCivic prepared facilities for rapid deployment, although operating cash flow declined due to working capital changes. The firm maintains a robust share repurchase program while managing a complex capital structure with no near-term debt maturities. Looking ahead, future growth hinges on sustaining government contracts amid regulatory risk and optimizing capital allocation between buybacks and expansion.

Historical Performance and Growth Drivers

CoreCivic has demonstrated steady revenue growth over recent years, culminating in a significant acceleration during fiscal year 2025. Revenue climbed from approximately $1.96 billion in 2024 to $2.21 billion in 2025, marking a robust year-over-year increase of roughly 12.7% [F1]. This top-line expansion reflects the activation of five previously idled facilities during 2025, newly awarded government contracts, and higher utilization primarily within its federal customer base.

The company’s ability to respond quickly to emergent government needs was catalyzed by a series of executive orders issued early in the Trump administration's second term starting January 2025. These included directives to intensify immigration enforcement—specifically detaining removable aliens—and reversing prior limitations on private correctional contracts within DOJ agencies [S1]. The legislative enactment of the Laken Riley Act further codified ICE’s mandate to hold certain non-U.S. nationals charged or convicted of specific crimes in detention facilities operated under CoreCivic’s management [S1]. These regulatory shifts created palpable demand spikes that CoreCivic tactically met through reactivating dormant capacity.

Operating income data prior to FY2025 is limited within tagged XBRL disclosures; however, historically CoreCivic exhibited variation attributable to changes in occupancy rates and cost management initiatives [F1]. The notable jump in revenue during FY2025 corresponded with an increase in facility net operating income by approximately $50 million versus prior years as reported [S14].

Historical performance (annual)

| FY | Rev ($bn) | CFO ($mm) | Capex ($mm) | Rev YoY |

|---|---|---|---|---|

| 2025 | 2.2 | 195 | 142 | +12.7% |

| 2024 | 2.0 | 269 | 70 | +3.4% |

| 2023 | 1.9 | 232 | 68 | +2.8% |

| 2022 | 1.8 | 154 | 83 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Net, OpInc, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 45000 | 229 | 53 |

| 2024 | 136000 | 77 | 199 |

| 2023 | 131000 | 43 | 164 |

| 2022 | 886000 | 80 | 70 |

Source: SEC companyfacts cache [F1].

Net income figures for FY2023–25 are not fully available from tagged data; FY2022 net income was approximately $122 million per SEC filings [F1]. Dividends have been nominal since CoreCivic ceased REIT distributions after tax status change.

Strategic Capital Allocation

Capital deployment reflects a deliberate strategy balancing growth investment with shareholder returns through buybacks. Capital expenditures surged over twofold from $70 million in FY2024 to about $142 million in FY2025 [F1], primarily related to reactivation and preparation of currently idled facilities alongside transportation assets supporting detainee movement [S4][S12]. Notably, the acquisition of Farmville Detention Center worth approximately $71 million adds around $40 million annual incremental revenue via an intergovernmental service agreement with ICE expiring March 2029 [S4].

Operating cash flow declined nearly 28% in FY2025 compared with the prior year largely due to working capital fluctuations despite increased facility operating income improvements [F1][S14]. This divergence highlights timing effects linked to government payment cycles and invoice approvals that introduce cash flow volatility.

The Board-approved share repurchase program exemplifies proactive capital return policy: initially authorized at $225 million it was expanded multiple times during mid-2025 reaching an aggregate ceiling of $700 million [S4][S7]. In calendar year 2025 alone, CoreCivic repurchased approximately $229 million worth of common shares at an average price near $19.48 per share [F1][S4], signaling management confidence amidst market volatility.

Dividend payments remain minimal post-REIT revocation effective January 2021; dividends paid dropped sharply from nearly $886k in FY2022 down to only $45k in FY2025—reflecting prioritization of debt reduction and buybacks over distributions [F1][S21].

Financial Position & Capital Structure

CoreCivic manages a sizable capital structure blending unsecured senior notes ($739 million combined principal for two tranches at fixed rates of approximately 4.75% and 8.25%), non-recourse secured mortgage notes ($134 million), term loans (~$112 million), and a recently expanded revolving credit facility sized at $575 million following late-2025 amendments [S6][S8][S16]. The weighted average interest rate across debt tranches is about 7.4%, with weighted average maturity around four years extending into October 2027 or later—mitigating near-term refinancing risk [S6][S18].

Cash on hand stood at nearly $98 million at year-end alongside over $311 million available under revolving credit lines ensuring ample liquidity buffer for operations and strategic investments [F1][S12]. The company maintains compliance with financial covenants typical for rated corporate borrowers including total leverage thresholds below stipulated maxima and adherence to fixed charge coverage ratios [S18].

Long-term liabilities include scheduled repayments but no material upcoming maturities before late-2027 easing pressure on refinancing while preserving flexibility for opportunistic uses of free cash flow such as additional buybacks or accretive acquisitions.

Business Model & Competitive Positioning

Operating through three principal segments—Safety (correctional & detention facility operations), Community (residential reentry centers), and Properties (real estate ownership)—CoreCivic claims status as the nation’s largest owner/operator combined platform serving federal/state/local governments across U.S correctional needs [S1]. With over roughly ~68,000 beds designed via owned or leased assets including recent additions like Farmville Detention Center (736 beds), the company offers unmatched scale relative to peers.

Its competitive advantages derive from:

- Extensive nationwide footprint enabling rapid activation or contractual scaling as government demand fluctuates;

- Long-standing relationships with multiple agencies including DOJ bureaus (BOP/USMS) and DHS (ICE);

- Ability to deliver cost efficiencies via economies of scale—bulk purchasing of medical supplies, food services—and operational expertise;

- Flexible contracting structures balancing leases vs management contracts tailored per jurisdictional requirements;

- Readiness investments prepping idled sites for quick population ramp-ups reducing lead times compared with publicly owned facilities.

These elements create barriers against new entrants owing primarily to upfront capital intensity plus stringent regulatory approvals governing secure detention operations.

Industry Catalysts & Risks Affecting Future Growth Prospects

Legislative and regulatory environment constitutes the single largest determinant shaping CoreCivic's medium-to-long-term trajectory:

- Aggressive immigration enforcement policies under current federal administration bolster utilization levels among its ICE-related contract portfolio [S1][N1]; acts like the Laken Riley Act codify detention mandates supporting bed demand.

- Past presidential directives restricting private prison use under DOJ agencies have been reversed but remain political overhangs susceptible to reversal following election cycles or administrative changes.

- Government budgetary constraints or appropriations delays risk payment timing impacting cash flow stability; recent invoice approval delays by DHS post-shutdown exemplify this exposure [S12][N3].

- Potential legal challenges targeting private correctional companies represent ongoing risk factors affecting reputational standing or contract viability.

- Societal shifts pushing reform toward decarceration could curb demand volumes despite current volume gains.

Growth opportunities include:

- Continued modernization of aging public correctional infrastructure presenting avenues for property segment developments or acquisitions complementing existing portfolio;

- Expansion into community-based alternatives addressing recidivism aligns with existing segment capabilities that can diversify revenue streams beyond traditional incarceration models [S10];

- Additional facility activations could be undertaken if visibility on contract pipeline improves enabling preemptive capital deployment [S12];

- M&A activity focused on complementary assets can bolster market share or geographic footprint.

What To Watch Next (Analysis)

Key near-term milestones include:

- Actual occupancy trends at newly activated facilities versus projections tied to ICE contractual volume growth;

- Pace of further capital expenditure spend given estimated reduction planned from ~$75m in FY25 down toward ~$35-$40m guide for FY26 making operational efficiency gains pivotal;

- Management’s incremental decisions on share repurchases vis-à-vis alternative uses such as debt repurchases or acquisitions particularly as liquidity profile strengthens;

- Government policy signals that could alter contracting norms especially federal DOJ/ICE renewal practices;

- Quarterly operating cash flow trends reflecting ability to stabilize seasonal working capital swings impacting free cash flow generation.

Monitoring these data points will illuminate trajectory sustainability beyond one-off policy-driven boosts witnessed through early FY25.

Disclaimer: This report is for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments