Upbound Group Expands Financial Wellness While Lease-to-Own Margins Contract

Upbound Group pursues growth through financial wellness acquisition amid lease-to-own margin pressures.

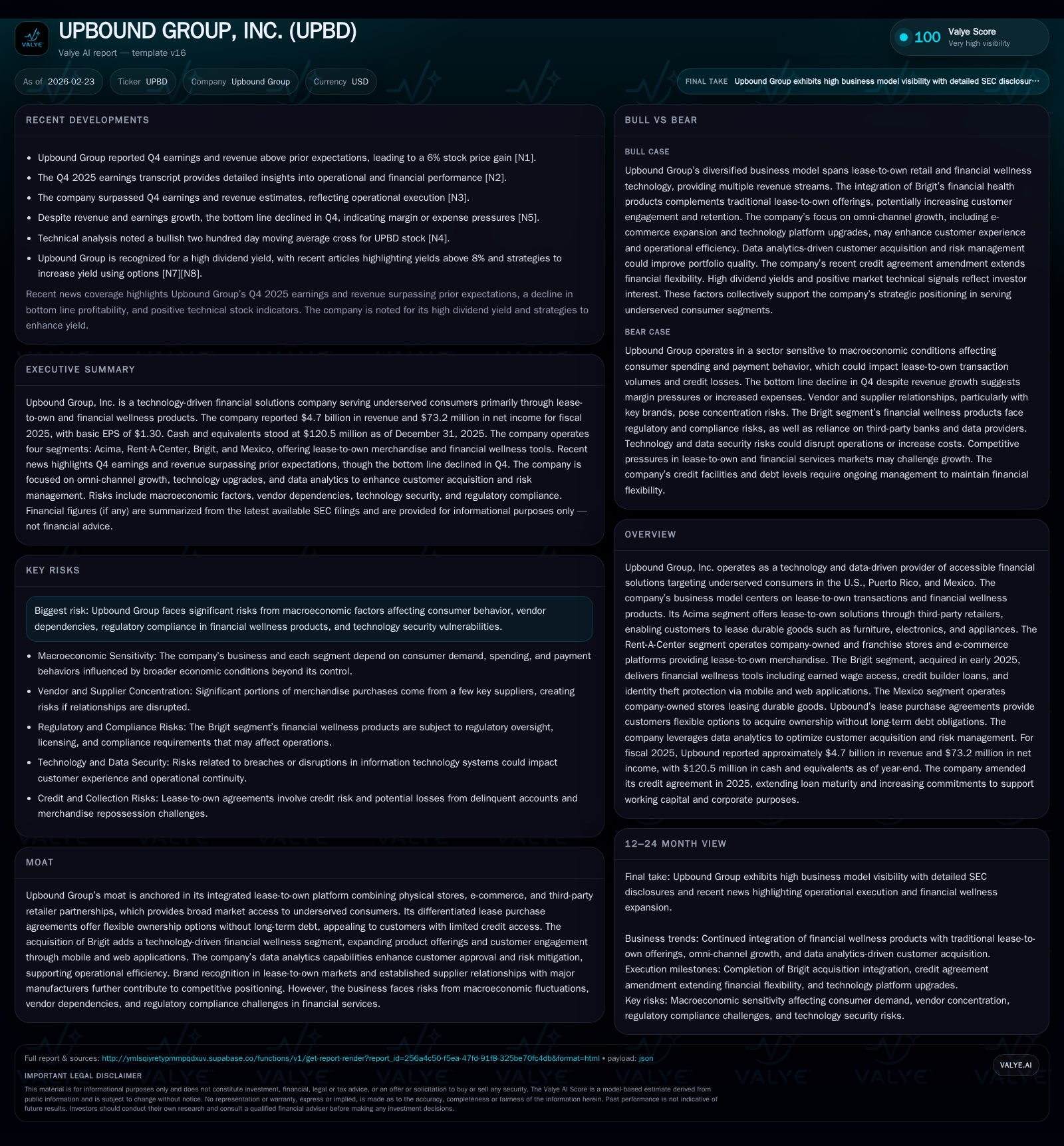

Upbound Group, a technology-driven lease-to-own provider targeting underserved consumers, posted 8.7% revenue growth to $4.7 billion in 2025 despite a 23.4% operating income decline and 40.7% net income drop, driven by longer lease durations and cost pressures. The acquisition of Brigit in early 2025 strategically diversifies Upbound’s offerings into financial wellness products like earned wage access and credit building, expanding customer engagement via digital platforms. Steady dividends alongside suspended buybacks reflect cautious capital allocation amid evolving macroeconomic and regulatory challenges. Monitoring upcoming earnings, margin trends post-Brigit integration, and regulatory developments will be key for assessing the company’s trajectory.

Lease-to-Own Foundation Drives Revenue Growth but Margins Diverge

Upbound Group continues to solidify its position as a leading provider of lease-to-own solutions tailored predominantly for underserved consumers across the U.S., Puerto Rico, and Mexico. The company's business hinges on flexible lease purchase agreements allowing customers to acquire durable goods without upfront full payment or long-term debt obligations [S5][S7]. In fiscal 2025, Upbound delivered a robust topline performance with revenues rising approximately 8.7% year-over-year to $4.695 billion [F1], driven by sustained demand in core Acima and Rent-A-Center segments.

However, contrasting with top-line strength, operating income contracted sharply by 23.4% to $223 million while net income fell even more sharply by over 40% to $73 million [F1]. This divergence reflects multiple unit economic headwinds notably longer lease durations that delay ownership timing under lease purchase agreements, resulting in increased exposure to credit loss allowances and elevating cost pressures [S5][S7]. Moreover, inflationary factors contributed to higher merchandise costs and operational expenses such as labor and delivery fees that are only partially recoverable through rents [S10][S11].

These dynamics underscore the delicate balance Upbound must strike in managing operating leverage; while higher revenues demonstrate market penetration, margin compression highlights the inherent challenges in scaling the lease-to-own model amid changing customer payment behavior and macroeconomic conditions [S6]. The characteristic rental product turnover—where merchandise is leased multiple times before eventual ownership—requires effective inventory management and loss mitigation programs to sustain profitability [S28].

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 4.7 | 73 | 306 | 223 | +8.7% | -40.7% |

| 2024 | 4.3 | 123 | 105 | 292 | +8.2% | +2484.2% |

| 2023 | 4.0 | -5 | 200 | 163 | -6.0% | -141.9% |

| 2022 | 4.2 | 12 | 468 | 149 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 88 | 0 | 239 |

| 2024 | 82 | 0 | 48 |

| 2023 | 83 | 50 | 147 |

| 2022 | 79 | 75 | 407 |

Source: SEC companyfacts cache [F1].

Note: Data from company XBRL filings; some YoY growth not calculated due to insufficient prior data.

Diversifying with Financial Wellness: Brigit Acquisition Impact

In a strategic portfolio expansion completed on January 31, 2025, Upbound acquired Brigit—a financial health technology platform offering earned wage access (EWA), credit builder loans, identity theft protection, budgeting tools, and other financial wellness services via mobile and web applications [S1][S5][N2]. This move extends Upbound's reach beyond physical lease-to-own merchandise into digital financial products aimed at improving the economic resilience of underserved customers.

Brigit's core offerings include Instant Cash advances which assess users' earned wages without traditional credit checks or FICO score impact, targeting liquidity needs between pay periods [S25]. Its Credit Builder loans serve dual purposes: providing a savings vehicle while establishing positive credit history reported to major bureaus—a critical differentiator in an industry often constrained by conventional underwriting barriers [S21]. Paid subscription tiers unlock enhanced features such as identity theft protection and personalized deals.

This technological foray deepens customer engagement beyond transactional leases toward holistic financial health support—a potentially powerful stickiness factor that complements the physical goods leasing ecosystem [N2][S7]. Early integration milestones emphasize data-driven underwriting improvements across segments leveraging Brigit’s analytics capabilities [N2]. Although reporting commenced just over one year ago with no full-year standalone comparables prior to acquisition, initial contribution has been promising while also introducing new operational complexities inherent in fintech regulation [S8][N18].

Segment Performance Breakdown and Geographic Footprint

Upbound organizes operations into four reporting segments: Acima (third-party retailer-based virtual/staffed lease-to-own), Rent-A-Center (company-owned/franchise stores plus e-commerce), Brigit (financial wellness products), and Mexico (company-operated stores) [S7][S14]. Substantially all revenues derive from the U.S., including Puerto Rico; Mexico represents a smaller but strategic geographic extension focusing on culturally adapted product assortments sourced locally [S26][S28].

- Acima Segment: This segment leverages partnerships with thousands of third-party retailers enabling broad product availability across furniture, consumer electronics, appliances, wheels & tires, and jewelry categories [S10][S26]. Customers unable to access traditional credit can obtain leases via kiosks or online platforms with minimal upfront requirements [S11]. Transition from acceptance brands to unified Acima platform was completed during 2024.

- Rent-A-Center Segment: Operating company-owned plus franchised storefronts along with integrated e-commerce channels rentacenter.com among others, this segment provides a fully omnichannel customer experience emphasizing name-brand durable goods with options for early ownership purchase or lifetime reinstatement protections [S10][S11][S14]. Approximately one-third of merchandise purchases are from Ashley Furniture Industries highlighting supplier concentration risks.

- Brigit Segment: Newly established post-acquisition in early 2025 this division delivers technology-driven financial tools mainly via digital interfaces focusing on earned wage access and credit enhancement products designed for low-to-moderate income consumers [S7][S25].

- Mexico Segment: Company-owned stores leasing durable goods within Mexican markets adjust their offerings based on local tastes including appliance assortments sourced domestically rather than primarily imported as in U.S. channels [S10][S28].

This diversified footprint allows Upbound to capture various subsegments of underserved consumers while balancing physical retail presence with scalable virtual offerings.

Macroeconomic and Regulatory Challenges Reshaping Operations

Upbound operates amidst intensifying macroeconomic headwinds influencing disposable incomes and consumer borrowing behaviors—including elevated inflation persistence dampening spending power—as well as significant regulatory scrutiny across lease-to-own transactions and emerging fintech services like those offered by Brigit [S6][S12][N5].

Key risk factors identified include:

- Regulatory environment: With nearly all U.S. states maintaining rental purchase statutes recognizing these transactions as distinct from traditional credit sales—but some states imposing caps or additional compliance burdens—Upbound faces ongoing costs related to disclosures, capped fees and consumer protections that could tighten further [S27][S6][S8]. The possibility that enforcement agencies or litigation may recharacterize leases as credit sales could materially increase compliance costs or alter business models.

- Vendor dependencies: Substantial reliance on suppliers such as Ashley Furniture Industries introduces risks should contractual relationships deteriorate or tariffs shift cost structures adversely affecting pricing strategies [S24][S26].

- Technology security: Both physical and digital operations maintain exposure to cybersecurity threats requiring ongoing investments in IT infrastructure to safeguard sensitive customer data especially within Brigit’s digital platform context [S6][S17].

- Macro conditions: Consumer risk appetites are highly correlated with unemployment rates, credit availability external interest rate environments impacting both demand for lease purchases and credit builder loans offered digitally [S16][S20].

These intersecting challenges shape operational flexibility while elevating capital needed for compliance readiness.

Capital Allocation Focus: Dividends Steady, Buybacks Halted

From a shareholder returns perspective, Upbound maintains consistent dividend payments signaling commitment to returning cash amidst profitability headwinds—$87.9 million paid in dividends during FY2025 versus $82.3 million in FY2024—even as net income contracted substantially [F1][S19]. Concurrently, share repurchases were suspended entirely from FY2024 onward following modest buybacks ($50 million) in FY2023 compared with earlier years indicative of prudent cash use prioritizing growth investments or debt service over buybacks amid uncertain economic outlooks [F1].

Operating cash flows surged impressively by nearly +192% YoY reaching approximately $306 million supporting dividend coverage ethos despite reported earnings weakness highlighting possible non-cash charge distortions or working capital improvements that bolster liquidity profiles going forward [F1]; capital expenditures rose moderately (+18.8%) reflecting reinvestment into property plant & equipment aligned with store network optimization efforts.

Return on equity remains around an approximate ~10.5%, illustrating relatively efficient equity utilization even as bottom-line pressure persists—underpinning balanced capital deployment between sustaining core leasing operations while incubating growth through fintech adjacencies enabled by Brigit’s acquisition [F1]. Leveraging data analytics for risk-adjusted approvals also aids portfolio quality underpinning this metric [N2][S21].

What Investors Should Watch: Upcoming Milestones and Market Signals

Looking ahead from an analytical lens absent explicit formal guidance disclosures [N2], several pivotal factors warrant close monitoring:

- Continued quarterly earnings trajectory to evaluate whether recent Q4 beats (+6% stock gain post-report) translate into sustainable margin recovery or if elevated cost structures persistently weigh on operating leverage outcomes [N1,N3,N5].

- Integration progress of Brigit segment reflecting capacity to cross-sell financial wellness products effectively alongside legacy lease-to-own offerings measuring shifts in customer acquisition dynamics or retention benefits deriving from digital engagement tools deployed post-acquisition [N2,S7,S25].

- Regulatory developments both at state and federal levels probing consumer finance practices targeting plausible reclassification risks impacting capital intensive lease models versus fintech service providers require ongoing attention given potential compliance cost escalation or forced structural changes [S6,S8,S18].

- Broader macroeconomic indicators shaping disposable income trends including wage pressures influencing EWA product demand as well as changing unemployment rates that impact customer default risk profiles central to portfolio asset quality assumptions embedded throughout proprietary decisioning algorithms leveraged across segments[S16,S20,N2].

- Strategic innovation within the financial wellness space particularly around AI-driven personalization enhancements or augmented underwriting capabilities may provide differentiation potentials albeit accompanied by emerging compliance frameworks increasing operational complexity[S18,N2].

These elements collectively form critical barometers of Upbound's ability to balance revenue growth opportunities against margin pressures within its dual-platform ecosystem serving financially underserved populations.

Disclaimer: This analysis is informational only and does not constitute investment advice or recommendations. It relies solely on provided SEC filings, transcripts, news sources cited herein without extrapolation beyond stated data points.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments