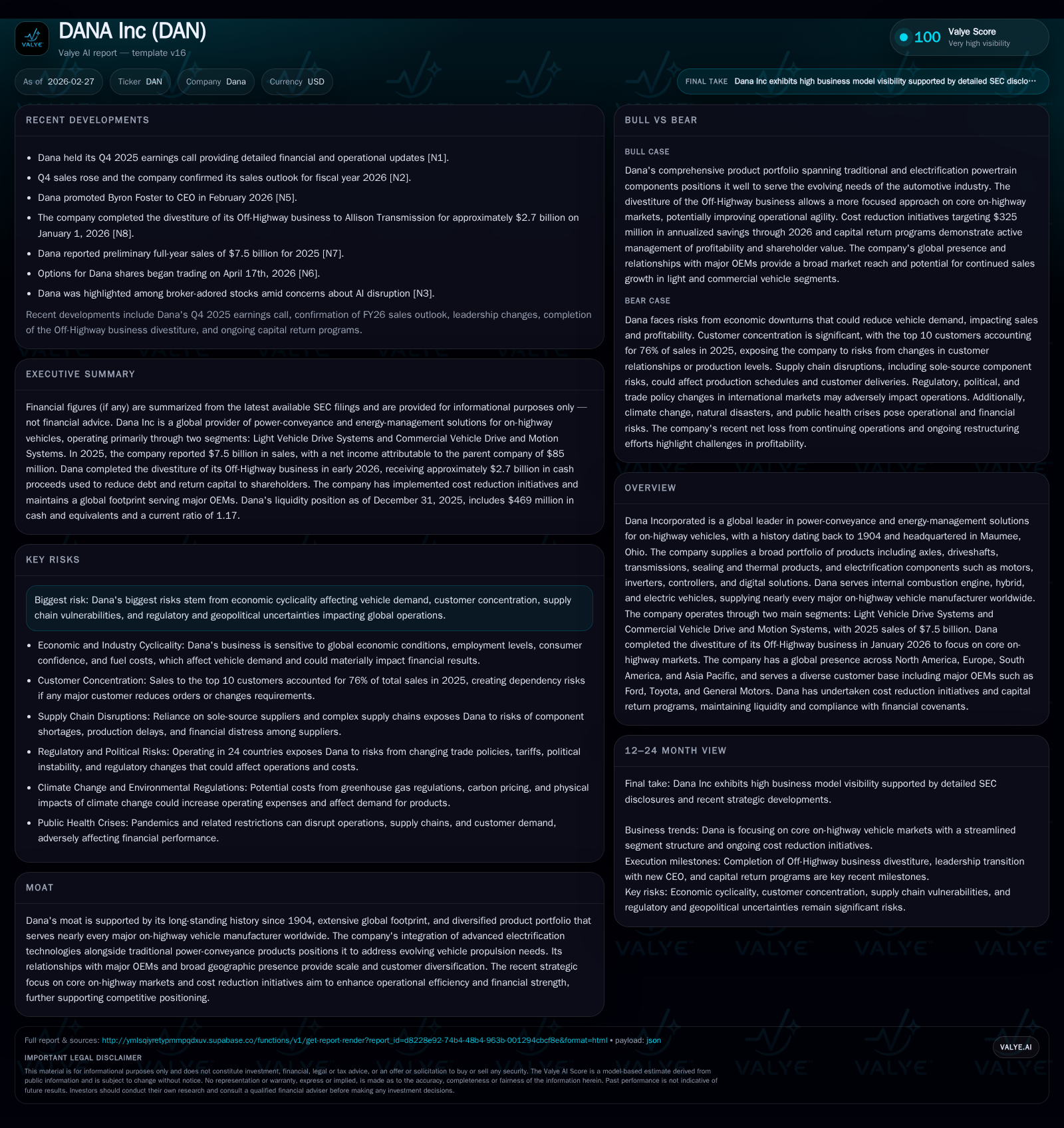

Dana Inc’s Strategic Focus on On-Highway Markets and Cost Efficiency Amid Challenging Profitability

Dana Inc sharpens its operational focus post-Off-Highway divestiture as revenue grows but profitability pressures persist.

Dana Inc, a century-old global supplier to major on-highway vehicle manufacturers, reported a 23.7% revenue increase in 2025 reaching $7.5 billion driven by stable light vehicle volumes and strategic divestiture of its Off-Highway business. Despite top-line growth, operating income declined significantly by 38.5%, reflecting margin compression from market delays in EV adoption and restructuring costs. The company's refined segment alignment and $325 million in annualized cost savings aim to restore earnings momentum while managing cyclical demand and supply chain risks. Dana's strong cash flow generation supports an expanded $2 billion share repurchase program through 2030, reflecting confidence in capital returns amid ongoing industry headwinds.

Company Overview and Historical Growth

Dana Incorporated is a globally recognized provider of power-conveyance and energy-management solutions tailored for on-highway vehicles, anchored by over a century of engineering expertise since its founding in 1904. Headquartered in Maumee, Ohio, it operates two main segments exposing it primarily to light vehicle drive systems and commercial vehicle drive/motion systems worldwide [S1]. In 2025, Dana's revenue reached approximately $7.5 billion—an increase of about 23.7% from prior years—reflecting growth driven by the company's concentrated exposure to its core on-highway OEM customer base functioning predominantly across North America, Europe, South America, and Asia Pacific [F1][S7].

Dana historically operated four segments but restructured in early 2025 by absorbing its Power Technologies segment into Light Vehicle and Commercial Vehicle divisions. This realignment was designed to streamline operations and enhance customer-focused efficiencies attributed largely to OEM relationships requiring integrated offerings spanning traditional mechanical driveline products alongside electrification components such as electric motors and controllers [S1][S18]. Additionally, the company divested its Off-Highway business at the start of 2026—a critical strategic pivot aiming to sharpen operational focus exclusively toward the more stable on-highway sector [S1][S27].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -50 | 512 | 139 | +12.3% |

| 2024 | -57 | 450 | 226 | -250.0% |

| 2023 | 38 | 476 | 316 | +115.7% |

| 2022 | -242 | 649 | 86 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 54 | 650 | -6.0 |

| 2024 | 58 | 25 | -4.3 |

| 2023 | 58 | 25 | 2.4 |

| 2022 | 58 | 25 | -15.6 |

Source: SEC companyfacts cache [F1].

Revenue reflects continuing operations after excluding the divested Off-Highway business; operating income shows significant contraction despite sales growth highlighting margin challenges.

Drivers Behind Historical Performance

The marked revenue growth over recent years primarily reflects continued engagement with leading global OEMs across multiple geographies as well as partial contribution from macroeconomic recovery cycles supportive of light trucks, SUVs, vans, and commercial trucks production volumes especially in North America which accounts for nearly two-thirds of overall sales [F1][S7]. Large customers such as Ford Motor Company, Stellantis N.V., Toyota Motor Corporation, General Motors Company, Volkswagen AG, and Mercedes-Benz Group AG anchor Dana’s contracts with high content per vehicle given focus on rear-wheel drive platforms favorable for axle-drive systems integration [S7].

Simultaneously however, profitability metrics have deteriorated from peak levels seen circa FY2023 due largely to elevated raw material costs exacerbated by supply chain disruptions along with operational headwinds arising from delayed electric vehicle uptake impacting planned volume ramp-ups for electrification product lines [F1][S22]. In Q4 2024 Dana announced substantial cost reduction programs targeting $325 million in annualized savings through better alignment of selling/general administrative expenses and engineering investments consistent with revised industry dynamics involving slower EV adoption than originally envisaged [S1]. These actions delivered approximately $260 million savings realized through FY2025 with incremental benefits expected in FY2026.

Pressure from input costs related to labor shortages and transportation logistics also weigh on margins as rising commodity prices cannot be fully passed onto customers due to OEM pricing pressures amidst fierce competition particularly in the light-duty market segment where EV technology transitions are unsettled [S20]. This dynamic is evident given the operating income decrease of nearly 40% year-on-year despite record revenues illustrating margin compression requiring active management.

Future Growth Prospects

Looking ahead into FY2026 and beyond, growth prospects hinge on multiple factors. Continued penetration into hybrid/electric driveline components positions Dana well within the broader automotive electrification landscape where rising regulatory mandates for emission reductions enhance demand for e-axle modules, inverter technology, digital controls and thermal management products for electrified powertrains [N5][S1]. The company’s strategy emphasizes leveraging deep OEM integrations combined with digital solutions aimed at predictive analytics improving system reliability—a crucial competitive advantage as vehicle platforms become increasingly software-defined.

Moreover, full focus on on-highway vehicles post-Off-Highway divestiture allows Dana to allocate capital more efficiently toward innovation pipelines relevant to core customers without dilution from unrelated off-road markets historically subject to more cyclicality and regulatory scrutiny [N5][S1]. Likewise, the aftermarket channel continues presenting growth opportunities supported by strong brand recognition globally delivering wide-ranging service parts under names like Spicer® Electrified™, Victor Reinz®, enhancing long-term revenue stability outside OEM production cycles.

Conversely, growth is capped by persistent risks including macroeconomic cyclicality impacting fleet replacement cycles especially in commercial trucking dependent regions; concentrated sales reliance where top ten customers constitute about three-quarters of total revenues raising vulnerability if program awards or production volumes shift unexpectedly; ongoing supply chain fragility highlighted by single-source components that may trigger shortages; geopolitical uncertainties affecting operations across multiple countries including Argentina exposure underlying currency volatility concerns; plus regulatory compliance costs related to evolving environmental mandates globally including carbon pricing risks which may escalate operating expenses unpredictably [S15][S21].

Forecasts and Operational Milestones

The company reaffirmed its full-year FY26 sales outlook consistent with prior guidance following a strong Q4 performance marked by sales increases reflecting solid order books from key OEMs combined with forecast stability across major regions including North America and Europe albeit tempered by cautious inventory replenishments at certain customers [N5]. Dana aims to close the fiscal year delivering further progress on cost savings targets set forth in late-2024 initiatives fully coming on stream this year validating restructuring outcomes.

Investors should monitor upcoming quarterly results focusing on margin trends tied closely to raw material price pass-through effectiveness along with new business development wins particularly around emerging electric vehicle architecture collaborations documented through production launches or contract awards among major global automakers. Progress in transitioning legacy Power Technologies capabilities embedded within reallocations toward Light Vehicle electrification will also serve as a key indicator of execution pace alongside aftermarket expansion updates.

Returns and Capital Allocation

Dana’s capital allocation approach balances reinvestment needs amid technological transition phases while actively returning cash generated via shareholder-friendly programs reflecting confidence despite earnings softness. Operating cash flow advanced approximately +13.8% in FY25 reaching $512 million fueled by disciplined working capital management alongside ongoing operational efficiencies even as capital expenditures were scaled back modestly relative to prior years underscoring near-term capital expenditure prudence amid industry uncertainty [F1][S14].

Free cash flow after estimated capex approximates $348 million supporting aggressive capital returns manifested through an expanded $2 billion stock repurchase authorization extended through end-2030—up from initial lower buyback targets—and steady dividend payouts maintained around $54-$58 million annually evidencing stable dividend policy commitment despite net losses recorded recently [F1][S19]. This robust cash deployment underscores management’s intent to enhance shareholder value amid ongoing cyclical volatility while preserving balance sheet flexibility evidenced by recent debt paydowns following proceeds from Off-Highway sale reducing leverage ratios conforming well within covenant limits [F1][S4][S26].

Industry Context (Analysis)

Automotive component suppliers like Dana operate within complex ecosystems increasingly shaped by electrification mandates paired with established ICE market decline trajectories disproportionately affecting suppliers focused predominantly on traditional driveline products. The dual challenge is maintaining competitiveness during technology transitions while addressing highly competitive OEM sourcing processes increasingly prioritizing system integration capability inclusive of digital controls software proficiency alongside hardware excellence.

Procurement patterns favor consolidated vendors capable of offering breadth across electrified drivetrains engulfing motor design/inverter integration plus thermal management essential for battery pack efficacy—all areas within Dana’s scope—thus providing structural barriers but also obligating sustained R&D investments balancing costs against shrinking warranties from delayed EV volume ramps typical given broader market adoption lags.

Risks Summary

Dana faces notable risks rooted primarily in economic sensitivity affecting underlying vehicle production volumes globally intensified by concentrated customer exposure where few large OEMs dominate purchase volumes creating dependency risks if program awards wane unexpectedly. Supply chain complexity exposes vulnerability through reliance on select suppliers amid raw material pricing fluctuations susceptible to geopolitical trade policies or localized disruptions induced by natural catastrophes or health crises like pandemics causing prolonged manufacturing pauses or logistical bottlenecks negatively impacting just-in-time delivery reliant model efficiencies intrinsic within automotive supply chains.

Environmental regulations imposing stricter emission standards coupled with possible carbon penalties elevate compliance costs variably impacting manufacturing footprints worldwide increasing operational risk exposure especially if climate legislation diverges geographically complicating global supply consistency at reasonable cost thresholds.

Additionally cybersecurity threats intensify given expanded digital integration within product portfolios necessitating vigilant IT safeguard enhancement lest intellectual property or operational continuity face compromise leading to financial or reputational detriment potentially injuring competitive positioning.[S15][S21]

Conclusion

Dana Incorporated stands at a pivotal juncture reinforced by strategic portfolio pruning concentrating exclusively on on-highway light and commercial vehicles complemented by artificial rapid cost discipline promoting sustainable cash flows enabling meaningful shareholder returns while navigating transitionary challenges common across automotive supplier landscapes adapting to electrification megatrends.

Going forward the company must demonstrate resilience managing margin pressures amid evolving industry cycles while harnessing growth avenues presented by electrification platform proliferation supported through expanded product integration spanning mechanical hardware complemented with digital control capabilities foundational for future propulsion architectures.

This analysis relies solely upon publicly available data as of February 27, 2026, encompassing official SEC filings and verifiable news sources without speculative extrapolations or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments