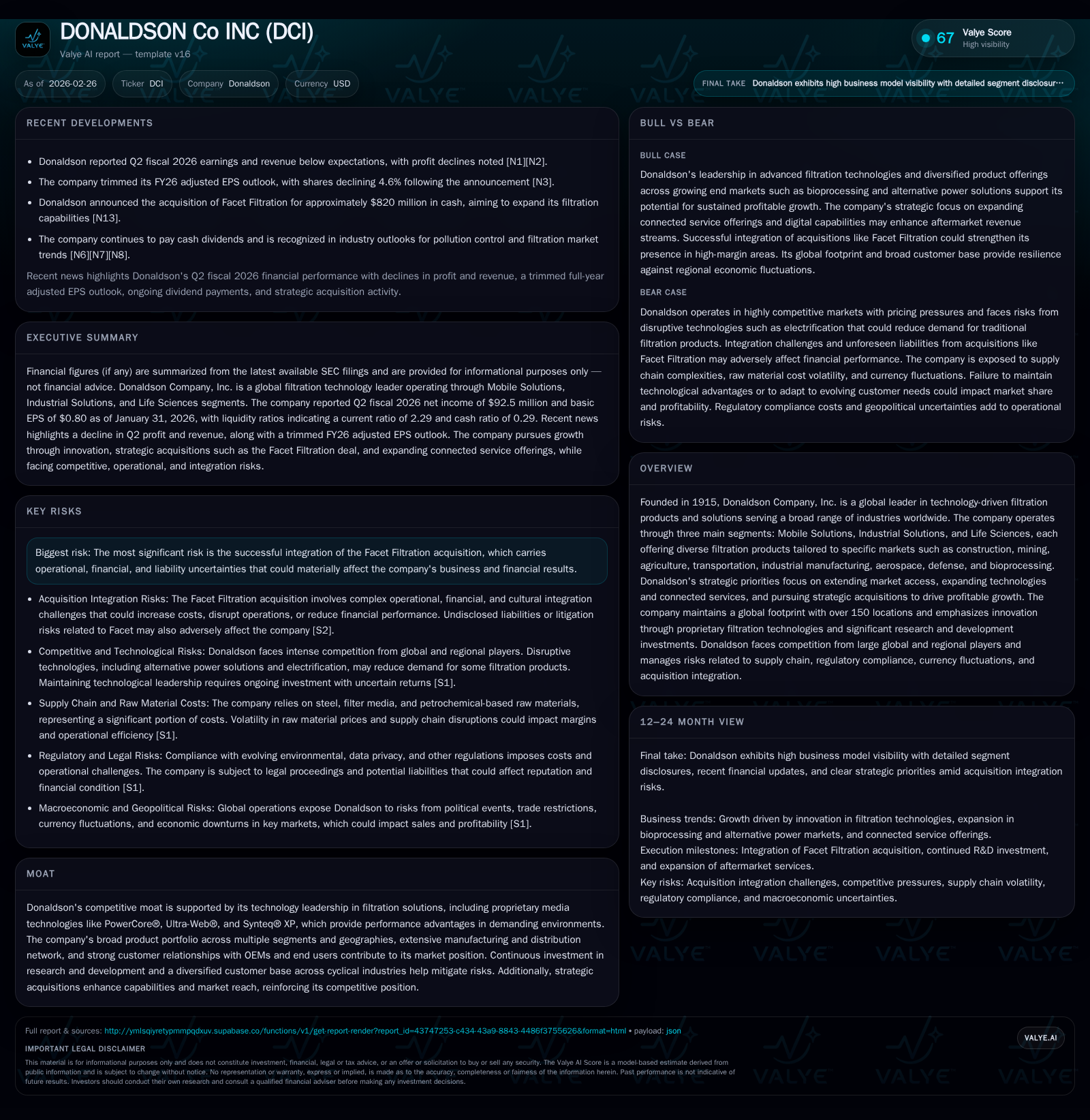

Donaldson Co Inc’s Strategic Expansion and Technology Leadership Face Integration and Market Pressures

Donaldson is navigating growth challenges following a major acquisition amid evolving filtration technology demands and competitive pressures.

Donaldson Company, Inc., a century-old leader in filtration technologies, has demonstrated steady historical revenue growth with a strong emphasis on innovation and market diversification. The company’s acquisition of Facet Filtration marks a significant strategic move to enhance its Life Sciences presence but introduces integration risks affecting near-term financials. While Donaldson maintains robust cash flow generation and disciplined capital allocation, slowed operational momentum alongside rising competition and potential market disruptions related to alternative power solutions imply cautious monitoring of upcoming quarterly milestones and integration progress.

Company Overview

Founded in 1915, Donaldson Company, Inc. is a well-established global provider of technology-led filtration products spanning multiple industries from construction and mining to aerospace and bioprocessing [S1]. Operating from over 150 locations worldwide—including 77 manufacturing or distribution centers—Donaldson serves both OEMs and aftermarket channels with highly engineered filtration systems tailored for harsh environments.

The company divides its business into three core segments: Mobile Solutions (62.1% of fiscal 2025 net sales), Industrial Solutions (29.9%), and Life Sciences (8%) [S7][S28]. Mobile Solutions focus on replacement filters for air, fuel, lube, hydraulic systems plus emissions components largely for off-road/on-road equipment; Industrial Solutions provide air filtration systems, gas purification equipment, hydraulics filtration, aerospace & defense applications; while Life Sciences encompasses bioprocessing consumables and specialty microenvironment filters for medical devices and semiconductors.

Historical Performance

Donaldson's revenue grew at a muted pace over the last few years—FY2019 top-line at approximately $727 million matches closely FY2018 levels—while more recent data from fiscal years shows better scale:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 367 | 419 | 495 | 79 | -11.4% |

| 2024 | 414 | 493 | 544 | 86 | +15.4% |

| 2023 | 359 | 545 | 480 | 119 | +7.8% |

| 2022 | 333 | 253 | 444 | 86 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 132 | 332 | 340 |

| 2024 | 123 | 163 | 407 |

| 2023 | 114 | 142 | 426 |

| 2022 | 110 | 171 | 167 |

Source: SEC companyfacts cache [F1].

Revenue figures are limited post-FY2019 by available data but the operating income dip of roughly 9% from FY2024 to FY2025 indicates margin compression potentially linked to new costs or weaker pricing environment; net income decreased accordingly by about eleven percent [F1]. Operating cash flow demonstrates volatility though remains robust enough to support free cash flow estimated near $340 million in FY2025 after capital expenditures.

Growth Drivers and Future Prospects

Donaldson emphasizes three strategic thrusts to propel profitable growth: expanding market access particularly within life sciences bioprocessing; extending technology leadership and connected services chiefly in industrial filtration; and pursuing acquisitions that meaningfully broaden high-margin capabilities or geographic reach [S13].

The recent acquisition of Facet Filtration for approximately $820 million aims to deepen Donaldson’s footprint in disruptive bioprocessing technologies within Life Sciences, including advanced membrane chromatography platforms critical for biologics manufacturing [N1][S26]. This aligns with rising demand trends driven by accelerated adoption of cell/gene therapies and increasing requirements for sustainable product outputs.

Additional growth cues lie in increasing aftermarket penetration in Industrial Solutions via connected service offerings such as iCue™ technology that monitors dust collection systems remotely to reduce downtime—a growing priority among factory automation customers focused on operational efficiency [S11][S25]. Furthermore, the Mobile Solutions segment benefits from steady demand for higher performance filters supporting stricter environmental standards across fleets in construction, agriculture, mining sectors.

Nonetheless, future growth is capped by factors including the rise of electric powertrain alternatives which threaten diesel engine replacement parts demand; economic cyclicality affecting key commoditized customer industries like mining or transportation; and tariff-induced cost volatility amid global trade tensions [S5][S14]. Manifold regulatory changes globally around emissions and sustainability also require ongoing R&D investments without assured commercial success.

Recent Performance & Outlook

Q2 Fiscal Year ’26 results reported on February 26 underscored challenges as Donaldson missed both earnings and revenue expectations amid softer end-market activity combined with integration expenses tied to Facet acquisition [N3][N8]. These setbacks triggered a downward revision of adjusted full-year EPS guidance leading to a notable share price reaction [N7].[N6]

Integration risk heightened as management highlighted complex operational alignments required post-acquisition including potential unidentified liabilities such as litigation or regulatory issues unresolved during due diligence [S2][S26]. This necessitates careful monitoring through subsequent quarters for evidence of stabilization.

Capital Allocation & Returns

Donaldson maintains a disciplined capital deployment approach balancing shareholder returns with strategic reinvestment [F1][S9]. Fiscal year ’25 saw $132 million returned via dividends alongside share repurchases totaling $331 million—more than double buyback volume versus previous year—indicating confidence in excess cash generation capacity.

Capital expenditures have moderated from elevated investment levels seen earlier this decade to under $80 million recently while R&D spending remains above two percent of sales annually supporting continued innovation leadership [F1][S10]. Based on latest annual figures for net income against equity base (~$1.45 billion), approximate return on equity stands at ~25%, reflecting solid profitability despite recent margin headwinds.

Competitive Position & Risks

Donaldson’s moat is largely technology-driven with proprietary media technologies like PowerCore® enabling compact high-efficiency air filters favored by OEMs facing stringent environmental regulations globally; Ultra-Web® technology ensures reliability in harsh climates enhancing durability against competitors’ products; Synteq® XP extends performance on liquid filtration fronts [S28].

Competition ranges from large multinational players offering broad filtration portfolios to regional specialists focusing on niche geographies or applications that may encroach especially within Aftermarket channels where price sensitivity intensifies [S4][S11]. Additionally, supply chain complexity caused by concentration in raw materials such as steel or plastic exposes Donaldson to risks of increased input costs or delivery delays impacting margins [S18].

Regulatory compliance costs continue rising amid enhanced environmental laws worldwide while cybersecurity vulnerabilities pose emerging operational threats despite existing protections [S20][S27]. Furthermore, integration risks remain elevated with Facet acquisition including cultural alignment challenges and unknown contingent liabilities potentially weighing on financial outcomes longer term if not mitigated [N1][N3][S2][S26].

Industry Context (Analysis)

Filtration technology is foundational yet evolving in response to stricter environmental standards targeting particulate matter reductions from combustion engines plus broader trends toward manufacturing cleanliness vital for biotech therapeutics production or semiconductor fabrication purity demands. Electrification poses long-term risk shrinking traditional diesel filtration markets yet opens avenues for novel filtration needs such as battery thermal management dust control or hydrogen fuel cell purifications—areas where incumbents like Donaldson must innovate swiftly or cede share.

Global supply chains remain under pressure with raw material inflation translating into customer price negotiations challenging margin preservation despite premium product positioning.

What To Watch

- Trajectory of financial results particularly operating margins during FY26 quarters amid Facet integration progress.

- Updates on any liability exposures stemming from Facet acquisition post-close disclosures.

- Execution pace of digital connected services rollout expanding Industrial Solutions aftermarket participation.

- Adoption rates of Life Sciences novel bioprocessing platforms vis-à-vis competitor innovations.

- Impact assessment related to shifts in fleet powertrains away from diesel-based engines affecting Mobile Solutions revenues.

- Responses to macroeconomic headwinds such as tariff impositions or currency fluctuations given multinational footprint.

This analysis synthesizes publicly available SEC filings up to February 26, 2026 ([F1], [S#]) alongside recent news disclosures ([N#]). It does not constitute investment advice or recommendations but aims to provide comprehensive insight into Donaldson Company’s business dynamics amid industry trends.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments