DELCATH SYSTEMS Emerges Profitable: Examining the Turnaround in Liver Cancer Therapeutics

Delcath Systems achieved its first net income in 2025, driven by its FDA-approved HEPZATO KIT and European CHEMOSAT system amid operational scaling and regulatory challenges.

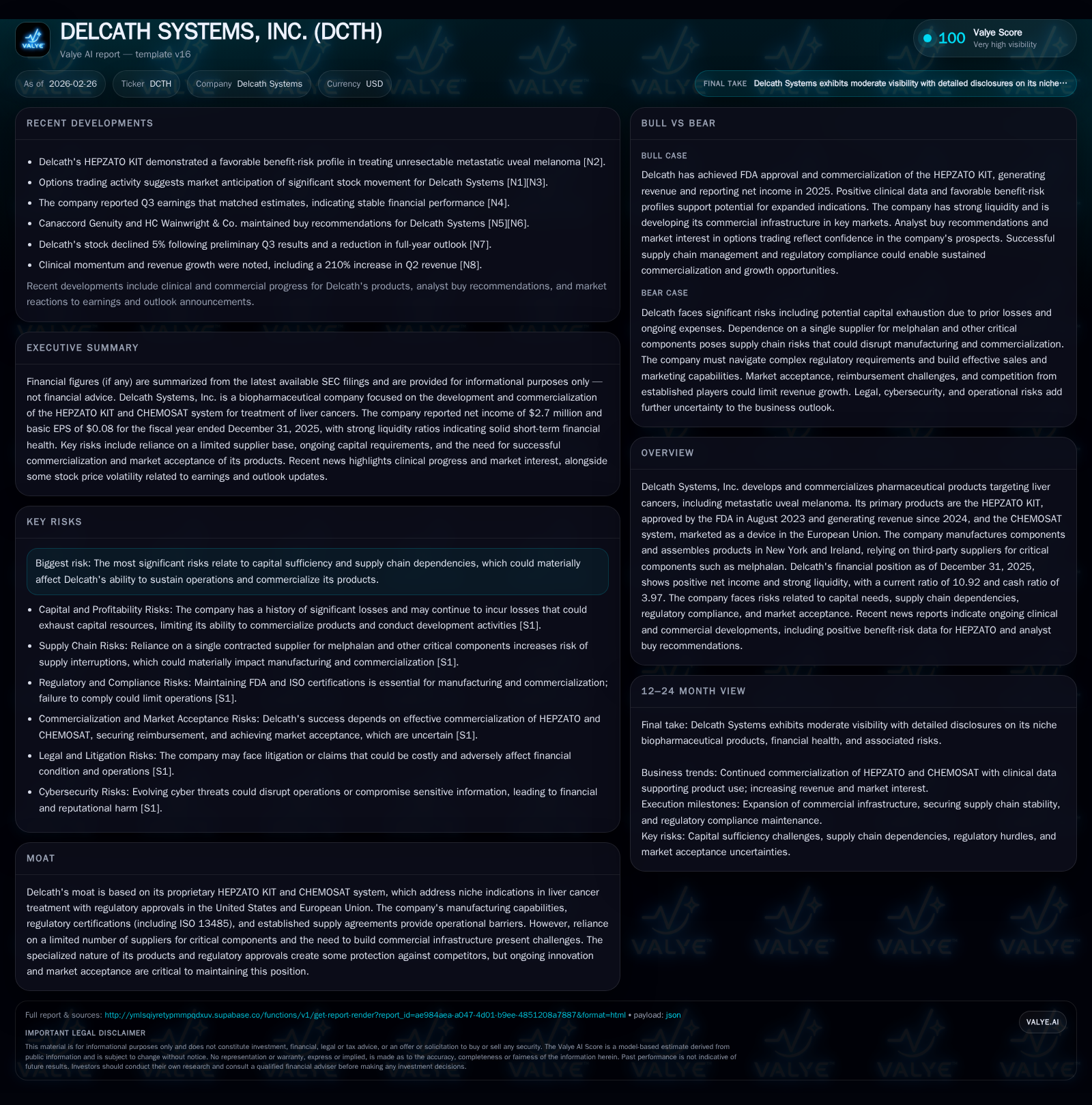

After multiple years of substantial losses, Delcath Systems recorded positive operating and net income in 2025, a pivotal inflection marked by commercial revenue from its niche liver cancer products. This profitability reflects improved manufacturing efficiency, supply chain stabilization, and expanding market acceptance of the HEPZATO KIT and CHEMOSAT system. Despite this progress, the company faces ongoing risks including dependency on limited suppliers, regulatory compliance burdens, and healthcare pricing pressures. Careful monitoring of reimbursement status, clinical adoption, and capital deployment will be key to sustaining growth momentum beyond this inaugural profit year.

Evolution of Delcath's Product Portfolio and Historical Financial Growth

Delcath Systems’ fiscal history has been characterized by substantial net losses stemming from intensive R&D investments aimed at developing novel treatments for liver cancers, notably metastatic uveal melanoma (mUM). The company's primary products—the HEPZATO KIT and the CHEMOSAT system—represent its strategic focus. HEPZATO received FDA approval in August 2023, marking a critical milestone that facilitated revenue generation commencing in calendar year 2024 [S1]. Concurrently, the CHEMOSAT system is commercially available as a medical device within the European Union under applicable device regulations.

Financially, Delcath’s multi-year pattern of losses reversed as product commercialization began yielding sales. Operating income deepened its negative trajectory from -$33.9 million in FY2022 to -$38.2 million in FY2023 but then improved markedly to -$12.4 million in FY2024 as initial revenues materialized post-HEPZATO approval; finally turning positive at $660,000 in FY2025 [F1]. Net income mirrored this arc with losses exceeding $36 million during early years before turning positive with $2.7 million reported in FY2025.

Operating cash flow followed suit but displayed sharper volatility: from negative cash flow exceeding -$31 million in FY2023 to a positive $22.5 million inflow in FY2025, evidencing an operational pivot reflecting both increased sales collections and cost containment measures [F1]. This broad financial progression underscores how pivotal product regulatory milestones directly catalyzed top-line growth and set the stage for operational leverage.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 3 | 23 | 1 | 1547000 | +110.2% |

| 2024 | -26 | -19 | -12 | 559000 | +44.7% |

| 2023 | -48 | -31 | -38 | 58000 | -30.6% |

| 2022 | -37 | -25 | -34 | 209000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 21 | 2.4 |

| 2024 | -19 | -38.4 |

| 2023 | -31 | -302.2 |

| 2022 | -25 | 623.1 |

Source: SEC companyfacts cache [F1].

Table illustrates Delcath's transition from deep losses toward profitability by FY2025 coincident with product launch timelines [F1].

Drivers Behind the 2025 Financial Turnaround: From Losses to Operating Profit

The improvement from operating losses surpassing $12 million in FY2024 to a positive operating income of $660 thousand in FY2025 reflects several intertwined factors documented within corporate disclosures:

Revenue Growth: The commercial launch of the HEPZATO KIT—the only FDA-approved therapy specifically targeting mUM—generated incremental product sales beginning mid-2024 with ongoing acceleration through calendar year 2025 [S3][F1]. Complementary contributions from CHEMOSAT sales across Europe supported overall results.

Manufacturing Optimization: Delcath’s operations include component manufacturing sites based in New York and Ireland. Improvements implemented during FY2025 stabilized production yield rates and minimized quality control reworks while managing third-party suppliers—particularly critical providers of melphalan bulk drug substance—a key cytotoxic agent utilized both standalone and within CHEMOSAT procedures [S19][S3].

Cost Controls: Tightening administrative expenses coupled with scaling efficiencies across logistics enabled margin expansion despite upfront commercial investment requirements.

Working Capital Turnaround: Positive operating cash flows surged to $22.5 million compared with prior negative cash burn trends exceeding $18 million annually by managing receivables collections more efficiently alongside inventory controls for raw materials and finished goods stockpiles [F1].

Together these drivers lifted Delcath into maiden profitability territory—a fundamental milestone validating underlying business model viability post-regulatory approvals.

Supply Chain Dependencies and Regulatory Challenges Shaping Future Prospects

Despite profitability gains Delcath faces material vulnerabilities tied to supply chain concentration and regulatory complexity:

Supplier Concentration: The company relies on limited specialized suppliers for critical inputs like melphalan. Disruptions or regulatory non-compliance at supplier facilities could constrain production capacity or incur costly remediation [S19][S1].

Regulatory Burden: Post-marketing obligations include an extensive Risk Evaluation and Mitigation Strategy (REMS) for HEPZATO mandated by FDA to monitor patient safety due to potential toxicity concerns inherent with melphalan-based therapies [S21]. Compliance requires continuous reporting and training programs which heighten operational complexity.

Healthcare Pricing Reforms: U.S. legislation such as the Medicare Drug Price Negotiation Program under the Inflation Reduction Act subjects qualifying drugs to government price negotiations potentially reducing reimbursements affecting coverage for indications like mUM therapy [S4][S9][S17].

Privacy and Fraud Regulations: Compliance with federal statutes including HIPAA alongside evolving state privacy laws governing patient data processed during promotion or clinical activities is required; failures could trigger penalties or litigation exposure [S6][S8][S22].

Balancing robust compliance frameworks while sustaining agile supply chains remains critical for future growth feasibility.

Commercial Footprint Expansion: Market Acceptance of HEPZATO and CHEMOSAT

Market penetration aligns with regulatory approvals enabling commercialization:

United States Market Dynamics: Following FDA approval CMS established a dedicated J-code (J9248) effective April 1, 2024 facilitating billing mechanisms for HEPZATO infusion procedures under Medicare Part B programs—a critical enabler of provider adoption [S17]. Market access depends on payer coverage decisions which may evolve subject to cost-effectiveness considerations.

European Commercialization: The CHEMOSAT system operates within EU device regulations but involves physicians procuring melphalan separately which may limit volume upside if adoption hesitates due to logistical or reimbursement factors [S21].

Clinical Community Endorsement: Given HEPZATO addresses an orphan indication with limited patients—the metastatic uveal melanoma subset—sustained endorsement requires continued publication of post-market clinical experience affirming safety/efficacy balance versus emerging alternatives [S4].

Thus penetration success hinges on payer policy stability as well as cultivating physician confidence through education and evidence dissemination.

Capital Deployment Strategy: Cash Reserves, Buybacks & Investments

Delcath’s balance sheet exhibits notable strength relative to immediate liquidity needs:

At December 31, 2025 cash & equivalents stood at approximately $43.5 million complemented by short-term investments totaling $47.6 million yielding strong current ratio metrics near ~10.9x evidencing conservative liability positioning versus assets available for near-term obligations [F1].

The company allocated roughly $1.55 million toward capital expenditures during FY2025 representing investments primarily focused on scaling manufacturing capabilities including facility enhancements aligned with Good Manufacturing Practices for both pharmaceutical bulk drug handling and medical device assembly lines [F1].

Share repurchases totaling $6 million reflected management’s confidence despite moderate operating earnings; signaling disciplined capital return intent amid growth investments rather than accumulation of idle cash balances [F1].

Return on equity was approximately 2.4%, indicating early profitability tempered by a significantly expanded equity base accumulated over recent years [F1]. Free cash flow (~$20.97 million calculated as CFO less capex) provides runway flexibility for further commercial expansion or R&D continuation.

Key Risks & Compliance Challenges Impacting Sustainability

Delcath identifies risk factors impacting sustained operations:

Capital sufficiency risks stem from prior accumulated deficits; ongoing profitability is not guaranteed given potentially costly post-marketing study commitments coupled with commercial scale-up expenditures that could outpace revenues absent successful market capture or pricing dynamics shifting unfavorably [S1][S26].

Pricing pressure risks arise from government initiatives targeting expensive single-source drugs including orphan therapies possibly reducing allowable reimbursements thereby compressing margins or limiting adoption incentives among providers faced with formulary constraints or substitution alternatives [S4][S9][S17][S24].

Healthcare fraud & abuse laws impose rigorous mandates restricting sales practices; violations risk penalties including exclusion from federal payor programs undermining revenue streams; Medicaid Drug Rebate Program reporting adds compliance costs yet remains mandatory [S4][S5][S6][S22].

Data privacy regulations present exposure via multiple federal/state laws regulating sensitive patient data processed during promotion or clinical database usage; breaches could provoke litigation or sanctions adversely affecting reputation or finances [S6][S8][S28].

These legal-compliance challenges underscore the delicate environment competitive biopharma enterprises face post-market approval beyond scientific advancement.

Outlook: Critical Milestones & Monitoring Points Ahead

While explicit forward-looking guidance is not provided publicly currently key areas warrant close attention:

Ongoing post-marketing safety surveillance outcomes related to HEPZATO’s REMS protocol will influence regulator confidence as well as prescriber willingness; any adverse findings could impose restrictions or limit label expansions.

Regulatory efforts toward new indications for HEPZATO or CE mark expansions within additional EU countries would expand addressable markets but involve substantial investment in clinical trials requiring timeline adherence ([S19]).

Payer coverage evolution remains critical amid potential healthcare policy shifts including cost containment strategies nationally; changes impacting reimbursement rates or formulary inclusion may alter demand abruptly.

In summary continued volume traction combined with proactive compliance stewardship will be essential for Delcath’s ability to sustain nascent profitability amidst a highly specialized therapeutic landscape.

This analysis synthesizes publicly filed SEC data alongside company disclosures without offering investment recommendations or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments