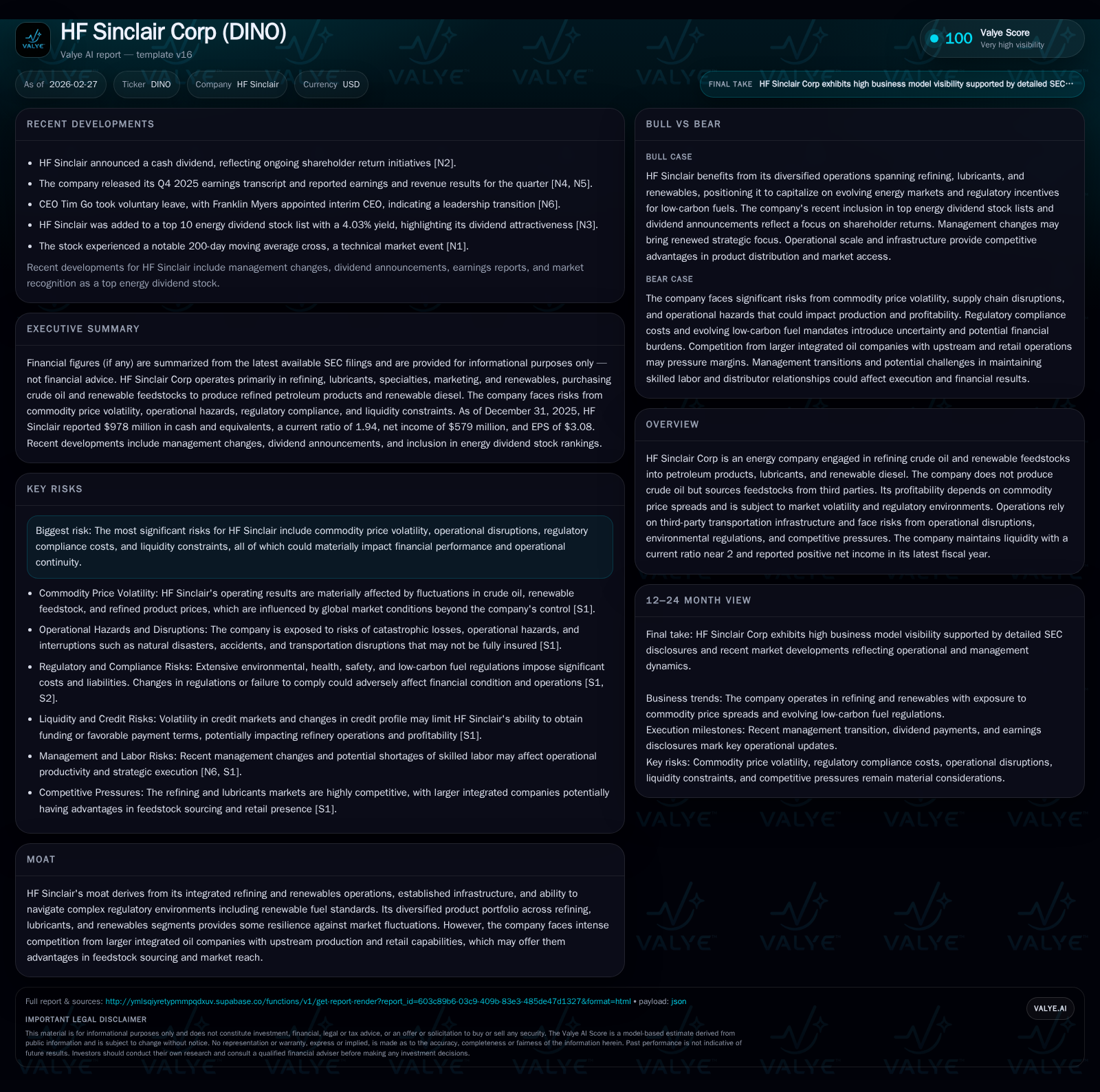

HF Sinclair's Transition to Renewable Diesel Amidst Market Volatility

The company’s refining turnaround and renewable diesel expansion unfold under volatile commodity prices and shifting regulatory demands.

HF Sinclair Corp demonstrated a sharp resurgence in earnings in fiscal year 2025 despite a notable revenue decline, driven by improved operational leverage and an evolving product mix emphasizing renewable diesel. The company's reliance on third-party feedstock sourcing and exposure to volatile RIN credit costs weigh on profitability amid tightening government regulations. Capital allocation has adapted with dividend initiations and scaled-back buybacks, supported by strong liquidity metrics. Leadership transitions add governance uncertainty as the firm navigates operational risks and emerging catalysts tied to climate policy and energy demand shifts.

Revenue and Earnings Evolution: The Turnaround Trajectory

HF Sinclair Corp posted a striking financial reversal in fiscal year 2025 anchored by a +255% jump in operating income to approximately $927 million from $261 million in 2024, according to the latest annual report [F1]. This significant upside took place despite the company experiencing a sharp revenue contraction of over 42%, declining to levels consistent with lower processing volumes or pricing pressures [F1]. Net income followed suit, climbing from $177 million to $579 million, reflecting a +227% improvement [F1].

This divergence suggests HF Sinclair achieved considerable operational leverage or margin expansion, possibly through refined product slate optimization or higher-margin renewables penetration [N3]. However, the revenue shrinkage underscores ongoing headwinds from market volatility in commodity prices impacting top-line throughput or realizations.

Historical performance (annual)

| FY | Net ($bn) | CFO ($bn) | OpInc ($bn) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0.6 | 1.3 | 0.9 | 449 | +227.1% |

| 2024 | 0.2 | 1.1 | 0.3 | 470 | -88.9% |

| 2023 | 1.6 | 2.3 | 2.2 | 353 | -45.6% |

| 2022 | 2.9 | 3.8 | 4.1 | 485 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($bn) |

|---|---|---|---|

| 2025 | 376 | 354 | 0.9 |

| 2024 | 386 | 672 | 0.6 |

| 2023 | 341 | 999 | 1.9 |

| 2022 | 256 | 1372 | 3.3 |

Source: SEC companyfacts cache [F1].

Table shows key financial metrics highlighting the strong income recovery in FY2025 despite revenue declines [F1]

Drivers Behind the Performance Swing: Feedstock Sourcing and Product Mix

HF Sinclair operates without upstream crude production, relying entirely on third-party sourcing for crude oil and renewable feedstocks [S1]. This exposes it acutely to commodity price spreads—the differential between input costs and refined product prices—which materially affect profitability [S1]. The extreme volatility in crude markets coupled with supply chain intermittence presents ongoing challenges.

Compounding this are fluctuations in Renewable Identification Numbers (RINs) prices, credits required under U.S. Renewable Fuel Standards (RFS) for blending biofuels into petroleum products [S2]. HF Sinclair must purchase RINs on open markets when unable to blend sufficient renewable content directly, subjecting it to cost uncertainty. Inability to pass these costs onto customers or limited RIN availability could compress margins substantially [S2].

Further complexity arises from HF Sinclair’s diversified portfolio spanning petrochemical refining, lubricants, and an expanding renewables segment [F1][S14]. This diversity offers some resilience against petroleum pricing shocks but requires dynamic feedstock management and marketing agility.

Renewable Diesel Expansion: Navigating Regulations and Market Demand

The Renewable Diesel segment represents both an opportunity and challenge for HF Sinclair’s growth trajectory [N3][S2]. Increasing renewable mandates under evolving EPA policies elevate demand for low-carbon fuels but concurrently raise compliance costs linked to volatile RIN credit markets [S8][S24].

Small refinery exemptions, which historically softened some RFS obligations for refineries like those operated by HF Sinclair, remain uncertain following EPA decisions vacated or revised through court actions [S2]. Recent EPA grants of partial or full exemptions introduce ambiguity regarding future compliance burdens.

Despite these regulatory headwinds, mandated increases in renewable diesel consumption create market pull favorable to HF Sinclair’s renewables operations—provided execution balances shifting policy landscapes and cost exposures effectively.

Operational Risks: Regulatory Compliance and Infrastructure Reliance

HF Sinclair's operational footprint is subject to multifaceted risks including health, safety, environmental regulations, and reliance on third-party distribution infrastructure [S1][S6][S23]. Compliance failures can induce penalties or force operational interruptions while necessitating significant capital outlays.

Recent leadership developments underscore governance risk as CEO Tim Go entered voluntary leave with Board Chair Franklin Myers appointed interim CEO; this transition creates potential momentum disruption at a critical juncture for the company [N9][S19].

Moreover, logistical dependencies on pipelines, trucking, railroads—and vulnerability to cyber-attacks targeting control systems—compound operational fragility amid growing complexity of environmental oversight regimes [S26][S29].

Capital Allocation Priorities: Dividends, Buybacks, and Liquidity Stance

Capital return strategy reflects HF Sinclair’s adaptation to its cyclical environment. It initiated quarterly dividends recently at $0.50 per share providing investors an approximately 4% yield based on market commentary [N1][N11], signaling confidence in sustained free cash flow generation.

Share buybacks have been moderated sharply relative to previous years—from nearly $1.37 billion repurchased in FY2022 down to about $354 million in FY2025—indicating prudence aligned with volatile cash flow scenarios [F1][N12].

Robust liquidity positions reinforce this discipline; the company’s current ratio stands near 1.94 supported by nearly $978 million in cash reserves as of FY-end 2025 [F1][S4]. These metrics afford flexibility to meet working capital needs despite exposure to commodity price swings.

Financial Health Snapshot: Liquidity Ratios and Credit Facilities

Alongside cash liquidity preservation, HF Sinclair manages borrowing constraints imposed by revolving credit facility covenants restricting liens, indebtedness levels, ownership changes, and M&A activities [S4][S22]. Meeting these covenants is critical in securing financing options amid rising cost of capital environments globally [S5].

Exposure to floating rate debt introduces interest rate volatility risk requiring active treasury measures; failure to comply or adverse credit profile shifts risk accelerated maturities or borrowing prohibitions which could impair operational funding capacity [S4][S5].

Governance and Management Transitions Impacting Outlook

Governance stability faces tests with the CEO's voluntary leave effective early 2026 and interim leadership by Board Chair Franklin Myers along with appointment of Acting CFO Vivek Garg who brings experience but must navigate transitional challenges rapidly [N9][S19].

Such executive shifts often presage strategic re-examination periods potentially affecting investor sentiment or operational execution speed during critical phases of business transformation.

Future Catalysts and Industry Indicators to Monitor

Upcoming quarters will be pivotal as HF Sinclair reports earnings against expectations of continued profitability gains supported by renewables segment growth narratives but challenged by commodity swings [N7][N3]. Monitoring EPA updates on Renewable Fuel Standards clarity—including small refinery exemption frameworks—is essential given their bearing on compliance cost structures [S2][N13].

Additionally, sector movements such as Valero’s share price rally suggest wider investor sentiment shifts toward integrated refiners innovating via low carbon fuel initiatives which might influence HF Sinclair’s competitive positioning over time [N13]. Geopolitical developments influencing crude supply chains also represent latent volatility drivers for margin sustainability.

This analysis is based solely on reported data from HF Sinclair Corp’s official filings and verified news sources as cited. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments