Krispy Kreme’s Strategic Challenges and Growth Prospects in the Indulgence Market

Krispy Kreme’s iconic brand faces steep financial losses and operational dependencies as it pursues omni-channel and international growth.

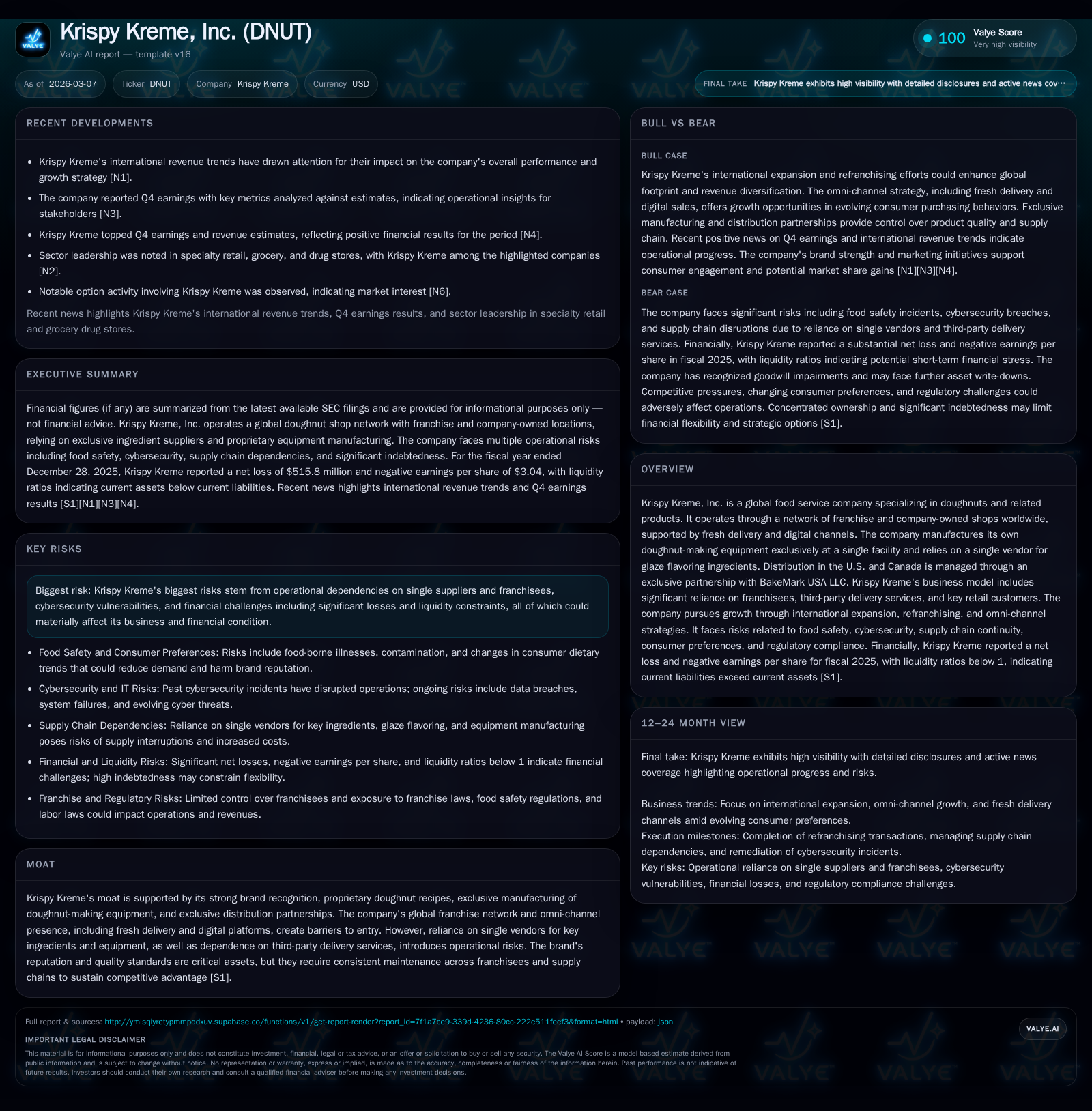

Krispy Kreme, a global leader in indulgence food service known for its signature doughnuts, has recently encountered significant financial headwinds marked by widening operating losses and a sharply negative net income trajectory. The company’s unique moat built on proprietary recipes, exclusive manufacturing, and franchise leverage is tempered by substantial supply chain risks and reliance on third-party delivery. Domestic growth appears mixed while international markets contribute a growing but challenged revenue stream. Financially strained with liquidity concerns and minimal capital returns, Krispy Kreme’s path forward hinges on successful refranchising, technological innovation in digital channels, and risk mitigation across its complex supply network.

Iconic Brand Built on Recipe Innovation and Exclusive Partnerships

Krispy Kreme boasts a distinctive competitive advantage anchored by its proprietary doughnut recipes that have cultivated strong brand recognition over decades. The company uniquely manufactures its doughnut-making equipment solely from a dedicated facility in Winston-Salem—an operational bottleneck that ensures quality control yet raises concentration risk [S1][S26]. Furthermore, Krispy Kreme holds exclusive ownership of its glaze recipe but sources essential glaze flavoring ingredients from a single vendor. This exclusivity underscores the firm's reliance on tightly controlled supply relationships rather than commodity sourcing flexibility.

The firm leases its distribution network in the U.S. and Canada exclusively to BakeMark USA LLC who handles ingredient packaging and supplies to both company-owned and franchised stores [S1][S10][S23]. These arrangements underpin franchise leverage by providing consistent product standards but impart operational vulnerability should BakeMark encounter disruptions. Krispy Kreme's omnichannel strategy extends beyond brick-and-mortar shops to include fresh delivery supported by digital platforms managed internally alongside partnerships with third-party delivery aggregators [S6]. While this hybrid distribution approach widens Points of Access for consumers, it embeds dependencies on external last-mile delivery operators whose performance can influence customer satisfaction negatively if service lapses.

Historical Performance Trends: From Profitability to Sharp Losses

The financial trajectory for Krispy Kreme from FY2022 through FY2025 reveals an alarming shift from moderate profitability into deep losses. Operating income swung from positive $29.0 million in 2022 to a loss of $8.7 million in 2024 before plummeting dramatically to -$469.3 million in 2025—a staggering deterioration amounting to a -5272% year-over-year decline last fiscal year [F1]. Net income trends echoed this pattern; while slightly positive at $3.1 million in 2024 after earlier losses (-$15.6 million in 2022), the bottom line collapsed to -$515.8 million by end-2025.

This steep operating margin compression aligns with the intense investments associated with refranchising efforts, international expansion costs, integration of fresh delivery channels, and digital platform development—typical dynamics for foodservice chains navigating transformation while managing inflationary pressures [F1]. Alongside these growth initiatives come higher fixed costs amid volatile commodity pricing (notably flour, sugar, shortening) exacerbated by ongoing inflation impacting cost structures [S23]. Such expense escalations alongside revenue-mix shifts conspire to deepen losses until operational scale efficiencies materialize.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -516 | 34 | -469 | 98 | -16764.5% |

| 2024 | 3 | 46 | -9 | 121 | +108.2% |

| 2023 | -38 | 46 | 13 | 121 | -142.8% |

| 2022 | -16 | 140 | 29 | 112 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 12 | 1 | -64 |

| 2024 | 24 | 5 | -75 |

| 2023 | 24 | 2 | -76 |

| 2022 | 23 | 4 | 28 |

Source: SEC companyfacts cache [F1].

Operating income swung from modest profits into sizable losses reflecting significant margin pressures over four years.

Supply Chain Dependencies and Operational Risk Factors

Krispy Kreme's manufacturing footprint is highly concentrated; it produces all its doughnut-making equipment at one facility which creates production continuity risk should disruptions emerge at this site [S26]. Replacing or relocating this manufacturing capability would be costly and time-consuming.

Additionally crucial is the company's dependence on a sole vendor for glaze flavoring ingredients derived exclusively from its recipes—an arrangement that creates single-source risk exposure that could imperil consistent product availability should supply interruptions occur [S1][S26]. Distribution within North America rides heavily on BakeMark USA LLC's exclusive contract; any operational or contractual failure here threatens ingredient supply chains affecting shop-level performance [S10][S23].

Franchisee variability represents another key risk vector: limited direct control over franchise operations may undermine quality or safety standards leading to reputational damage [S1][S16]. Cybersecurity events pose real threats; prior incidents during fiscal 2024 materially disrupted operations pointing to persistent IT system vulnerabilities inherent in managing complex omni-channel businesses reliant on technology platforms [S1][S19]. Legal exposures tied to food safety litigation or regulatory compliance further compound the company’s operational risks domain with FDA oversight intensifying around labeling and ingredient disclosures [S4][S7][S9].

Domestics vs International: Mixed Signals from Growth Drivers

While domestic same-store sales have shown softness due partly to saturated markets and evolving consumer preferences favoring health-conscious options thus challenging indulgence foods [N1], international revenue streams are increasingly pivotal [N1][S10][S12]. As of fiscal year-end 2025 data indicate approximately half or more of Krispy Kreme’s Points of Access are outside the U.S., signaling global franchising ambitions relying on joint ventures or strategic partners across multiple regions including Europe and Asia-Pacific [S19][S20].

However international expansion carries elevated geopolitical risks such as trade restrictions or currency volatility alongside logistical complexity [N1][S17][S20]. Success abroad necessitates scaling franchise recruitment while balancing local consumer taste adaptation without diluting core brand attributes—no small feat given cultural diversity across markets served.

Omni-Channel Expansion: Digital and Fresh Delivery Opportunities

Krispy Kreme’s omni-channel model rests heavily on blending brick-and-mortar experiences with digital engagement via mobile ordering apps backed by an internally managed platform supplemented by third-party delivery services handling last-mile logistics [S1][S6]. This hybrid approach aims at tapping convenience-driven consumption trends but also exposes the brand to marketplace fragmentation where aggregator fees compress margins.

Fresh delivery introduces additional regulatory compliance burdens around food safety controls given perishability as well as challenges maintaining quality through outsourced logistics providers whose workflows remain outside direct company command [S7][S20]. Rising competition within digital ecosystems necessitates continuous investment in technology upgrades utilizing artificial intelligence or machine learning capabilities to enhance personalized marketing effectiveness—a domain still nascent for the firm compared to larger rivals with deep pockets [S6][S24].

Financial Health Overview: Capital Structure, Cash Flows, and Capital Allocation

Key financial metrics portray liquidity strains and capital discipline reflective of transition-era challenges. As of late-2025 balance sheet figures reveal current assets totaling approximately $174 million contrasted against current liabilities exceeding $457 million yielding a distressed current ratio near 0.38 indicative of tight short-term liquidity coverage [F1][S22].

Operating cash flow declined roughly 26% year-on-year reaching nearly $34 million whereas capital expenditures contracted about 19% but remained elevated near $98 million evidencing ongoing investment requirements aligned with refranchising infrastructure deployment [F1]. Resultant free cash flow stood negative around $64 million signifying cash burn amid capex demands.

Equity declined substantially reflecting accumulated losses sliding below $650 million causing an approximate negative ROE near -79%, an unsustainable return figure underscoring underlying profitability challenges [F1]. Dividends paid were curtailed modestly alongside minimal share repurchase activity denoting cautious capital allocation aligned with debt deleveraging priorities outlined under credit covenant scrutiny [F1][S22][S27].

Strategic Outlook: What to Watch Next on Growth Milestones and Risk Mitigation

Upcoming investor milestones center on quarterly earnings releases expected to reveal progress in arresting operating losses via successful refranchising execution coupled with scaling omni-channel sales attributed primarily to enhanced mobile ordering adoption and fresh delivery penetration gains [N5][S6]. Technological investments aimed at fortifying cybersecurity defenses remain paramount given recent material weaknesses identified relating to IT internal controls potentially impacting timely accurate reporting capabilities [S1][S19].[N5]

Regulatory environment watch points include evolving food safety legislations imposing stricter ingredient disclosure norms as well as franchise law reforms potentially limiting enforcement powers over franchise agreements constituting revenue risks if fraternities mismanage compliance obligations or quality standards deteriorate [S4][S7][S9].[N5]

Supply continuity hinges critically on maintaining strong partnership terms with BakeMark USA LLC alongside developing contingency plans for glaze flavor intermediates sourcing ameliorating single-vendor dependencies flagged repeatedly as existential operational risks.[S23][S26]

Conclusion: Balancing Brand Legacy with Execution Risks

Krispy Kreme's illustrious heritage affords it substantial intangible assets encapsulated in brand loyalty secured through proprietary recipes and unique manufacturing prowess evidenced by specialized equipment production rights. However impressive this moat is superficially—the firm's viability relies on deftly navigating multifaceted execution risks stemming from acute supply chain concentration vulnerabilities compounded by deep operational losses stressing liquidity frameworks.

Expanding international footprint offers promise yet brings geopolitical volatility needing judicious franchise partner selection paired with refined consumer insights across heterogeneous markets. Simultaneously pursuing omni-channel innovation offers differentiated consumer engagement routes yet demands robust IT system resilience coupled with delivery logistics excellence under fierce competitive scrutiny.

Investor vigilance remains essential given significant financial headwinds reflected in large-scale quarterly losses undermining shareholder returns alongside systemic challenges regulating franchise ecosystems tightening operational oversight capacities amidst rising labor costs and evolving regulatory regimes.

In sum—a cautiously optimistic outlook predicated on sustained execution discipline applying rigorous capital allocation frameworks balancing reinvestment against deleveraging imperatives while safeguarding longstanding brand equity amidst exigent strategic tradeoffs confronting today’s indulgence sector disruptors.

This analysis is based solely on publicly available information provided through SEC filings ([F1],[S#]) and recent news releases ([N#]). It does not constitute investment advice or recommendations regarding Krispy Kreme securities or any other asset.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments