Doximity’s Strategic Growth Amid Healthcare Digitization and Legal Risks

Doximity leverages acquisitions, financial strength, and network effects to navigate evolving digital health challenges.

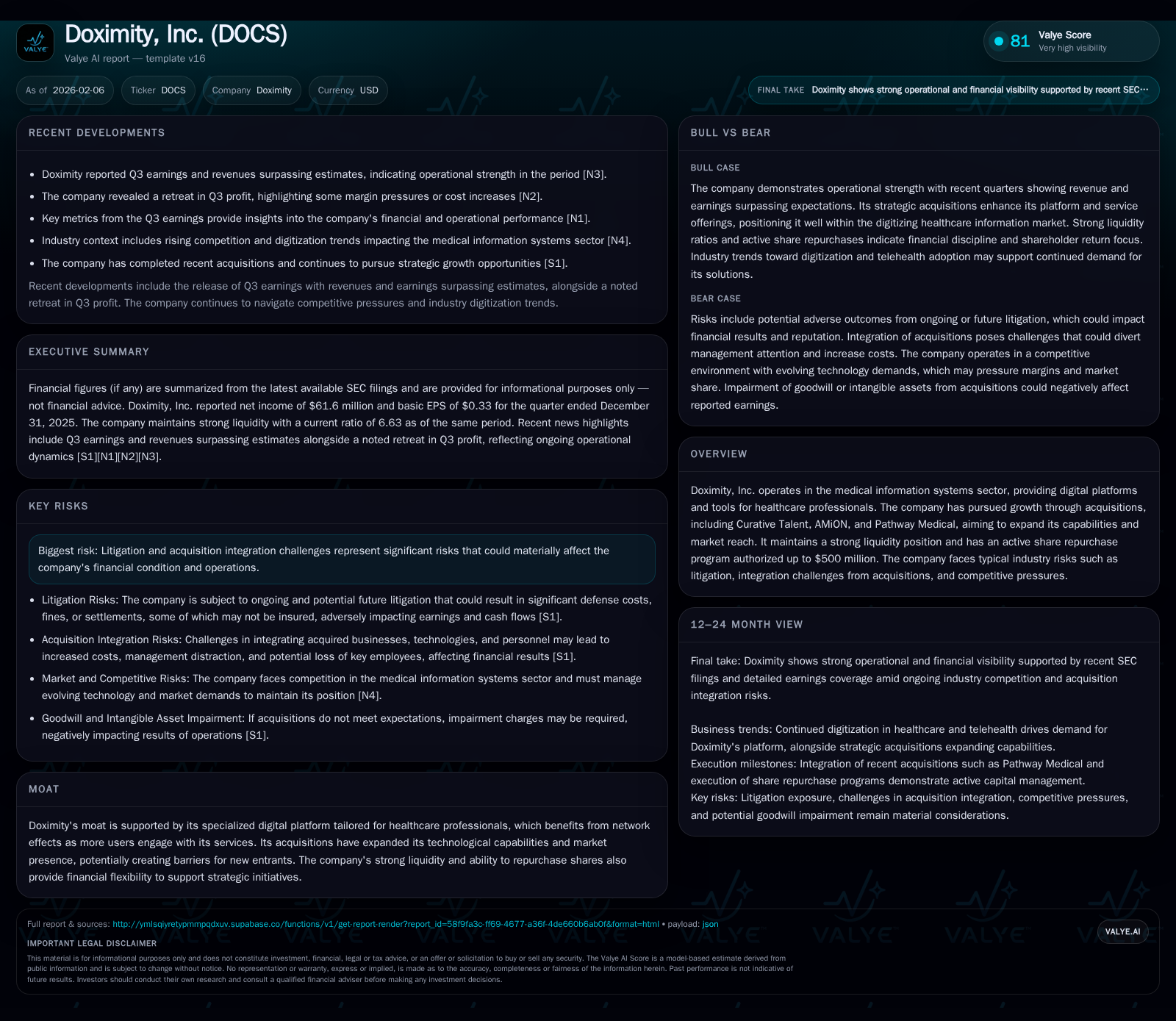

Doximity, Inc. has solidified its position in the medical information systems sector through a specialized healthcare professional platform that benefits from network effects and targeted acquisitions. Its robust liquidity, exemplified by a current ratio of approximately 6.63 and a substantial cash reserve, underpins ongoing strategic investments and a $500 million share repurchase program. However, the company faces significant risks from ongoing litigation and integration complexities from recent acquisitions such as Curative Talent, AMiON, and Pathway Medical. Meanwhile, rising industry competition and the accelerating AI-driven healthcare transformation create both headwinds and opportunities shaping its long-term outlook.

Doximity's Platform: Building a Digital Healthcare Network

At the heart of Doximity’s market presence lies its specialized medical information systems platform crafted exclusively for healthcare professionals. This tailored design fosters strong network effects—the utility of the platform increases as more clinicians engage with its services—effectively raising switching costs for users and erecting barriers to entry for potential competitors [valye_report_excerpt]. By intertwining communication tools, recruitment solutions, and medical data management in one ecosystem, Doximity cements its role as an indispensable resource for practitioners navigating increasingly complex healthcare environments.

The acquisitions of Curative Talent, AMiON, and Pathway Medical have bolstered this foundation by complementing core functionalities with expanded recruitment capabilities and improved clinical scheduling solutions. These integrations deepen user engagement by addressing key pain points along the healthcare professional workflow [valye_report_excerpt]. Such holistic coverage continues to differentiate Doximity within a crowded digital health space, suggesting sustained moat reinforcement grounded in user-centric innovation.

This foundational platform strength sets the stage for analyzing the company’s financial robustness that facilitates these strategic maneuvers.

Financial Fortitude: Liquidity and Profitability Trends

Examining Doximity’s recent financial disclosures reveals impressive short-term solvency. The company's current assets stood at approximately $993 million against just $150 million in current liabilities at fiscal year-end 2025, translating into a current ratio of about 6.63 [F1]. This ample liquidity cushion not only safeguards operational continuity amid unpredictable market conditions but also empowers strategic initiatives such as acquisitions and share repurchases.

Net income totaled roughly $61.6 million at year-end 2025 [F1], reflecting profitability despite pressures outlined in Q3 reports. The quarter notably surpassed analyst revenue estimates yet simultaneously disclosed a retreat in net profit margins [N2][N5]. This divergence underscores cost dynamics likely linked to acquisition integration expenses or investment in growth initiatives.

Cash reserves exceeding $64 million bolster capital deployment flexibility including an authorized $500 million share repurchase program [valye_report_excerpt], signaling management's confidence in returning value while maintaining financial strength.

Strong liquidity ensures that Doximity remains well-equipped to absorb shocks from operational setbacks or legal contingencies discussed later while pursuing long-term growth.

Growth by Acquisition: Strategic Expansion and Integration

Doximity’s expansion strategy hinges significantly on carefully selected acquisitions aimed at enhancing both platform capabilities and geographic reach. Curative Talent introduced advanced talent acquisition technologies to the portfolio in fiscal 2021; AMiON added clinical scheduling solutions in fiscal 2023; while Pathway Medical further broadened offerings after its mid-2025 purchase [valye_report_excerpt][S2]. Each deal ostensibly complements core competencies by filling gaps or extending addressable markets.

Nonetheless, integrating diverse systems and cultures remains complex. The risk disclosures highlight potential pitfalls such as difficulties maintaining uniform policies across acquired entities or disruptions caused by personnel amalgamations [S2]. Unsuccessful integrations could erode anticipated synergies or inflate costs materially impacting results.

Management publicly acknowledges these challenges but emphasizes robust processes to harmonize operations post-acquisition. Successful integration is foundational for sustaining the network effects critical to competitive advantage.

This dynamic interplay between expansion opportunity and integration risk is mirrored in external industry pressures threatening Doximity’s operating environment.

Industry Headwinds: Litigation and Competitive Dynamics

Doximity navigates a terrain marked by intensifying competition among digital health platforms alongside acute legal vulnerabilities. The company currently faces multiple litigations potentially exposing it to significant defense expenditures or settlements beyond insurance coverage limits [S2]. Such exposure may exert direct financial strain while diverting executive focus away from strategic priorities.

Legal battles also influence intangible factors—damaged reputation risks alienating customers or complicating talent retention [S2]. Concurrently, competitor activity escalates as rivals pursue innovations targeting segments overlapping with Doximity’s offerings [N6]. This heightened competition compresses pricing power and demands continuous product evolution.

In combination, these headwinds necessitate adaptive strategies balancing assertive innovation with cautious risk management—elements explored next under the lens of advancing AI adoption reshaping healthcare technology.

Evolving Market Position Amid the AI Boom

Artificial intelligence now commands center stage across healthcare digitization narratives with Doximity positioned as an influential participant among medical-tech stocks embracing AI-enhanced functionalities [N4][N10]. Analysts recognize DOCS as one of several top-tier names benefiting from AI-driven efficiencies despite sector volatility [N7].

The convergence of AI with medical information platforms offers promising dimensions—from boosting diagnostic decision support to streamlining administrative workflows—where incumbents like Doximity can leverage existing user bases to accelerate adoption curves [analysis]. Yet this opportunity entails constant innovation cycles lest rivals erode lead positions through novel technologies or data analytics capabilities.

Navigating this transformational wave will require disciplined investments fueled by financial resilience documented earlier alongside vigilance amid shifting regulatory landscapes governing AI use in healthcare products.

Breaking Down the Q3 Earnings Beat and Profit Retreat

Doximity’s latest quarterly report illustrated complex operational realities—revenues outpaced consensus forecasts signaling robust demand for core services [N2], however reported net profits diminished relative to prior periods [N5].

Disaggregating these results reveals that revenue growth was propelled by heightened product uptake across multiple segments including recruitment tools linked to recent acquisitions [N1]. Conversely, profitability contraction stemmed partly from elevated operating expenses related to integration efforts along with increased investments in R&D targeting AI capabilities and platform enhancements [N3].

This performance nuance highlights transitional phases where top-line momentum coexists with margin pressure typical for companies deepening platform sophistication while absorbing deal-related costs.

Understanding these earnings intricacies informs valuation judgments examined subsequently.

Valuation and Long-Term Growth Outlook

Market valuation of Doximity reflects a delicate balance between optimistic growth projections anchored by strong strategic assets versus caution warranted by sector turbulence. Notably, Wells Fargo upgraded DOCS citing sustained innovation pipelines despite recent profit softness, underscoring confidence in long-term trajectories [N12][N7].

Simultaneously, stock price declines exceeding broader market gains suggest underlying investor apprehension possibly linked to litigation risks or integration uncertainties [N8]. Share repurchase programs authorized up to $500 million function as mechanisms aligning shareholder interests with management confidence while potentially mitigating undervaluation pressures [valye_report_excerpt].

Ultimately, valuation considerations hinge on how effectively Doximity converts technological advantages into scalable earnings growth amid fiercely competitive environments.

Risks and Mitigation: Navigating Legal and Integration Challenges

Legal risk remains paramount; ongoing litigations entail material exposure capable of disrupting earnings consistency through unforeseen fines or settlement payouts unshielded by insurance coverage gaps [S2]. Such developments could inflate insurance premiums further constraining margins or impact board composition due to directors’ liability concerns.

Regarding acquisitions, challenges include blending disparate corporate cultures alongside harmonizing technical infrastructures without degrading service levels or brand equity—a multifaceted endeavor detailed extensively in risk disclosures [S2][valye_report_excerpt].

Management articulates proactive countermeasures encompassing robust compliance frameworks, dedicated legal defenses, rigorous due diligence ahead of deals, as well as comprehensive integration playbooks designed to preserve standards uniformly post-acquisition.

These mitigations are critical levers reducing downside probabilities while enabling growth strategies to proceed with calibrated oversight.

Investor Sentiment and Stock Performance Trends

Recent stock trends portray DOCS as experiencing disproportionate declines relative to general market rebounds despite fundamental progress [N14][N8]. Technical indicators such as RSI entering oversold territory reinforce perceptions of short-term undervaluation though accompanied by lingering uncertainty driven by litigation news cycles [N13].

Contrastingly, analyst sentiment exhibits constructive tones evidenced in upgrades emphasizing prospective AI-driven expansion balanced against acknowledgment of profit margin pressures [N12][N7]. This dual narrative conveys a nuanced investor psyche torn between opportunity recognition and caution amidst sector-wide telehealth volatility discussions [N9][N11].

The interplay between behavioral dynamics and underlying fundamentals will be pivotal shaping DOCS’s market trajectory moving forward.

This analysis synthesizes publicly available financial data, regulatory filings, and industry commentary up to early February 2026 without prescribing any investment decisions. Market conditions evolve rapidly; readers should consider multifaceted factors when interpreting this information.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments