Roman DBDR Acquisition Corp. II’s SPAC Model Hinges on Climate-Tech Merger Execution

Roman DBDR Acquisition Corp. II is navigating the transition from a capital-raising shell to an operating entity through a pivotal merger with ThomasLloyd Climate Solutions targeting AI data centers.

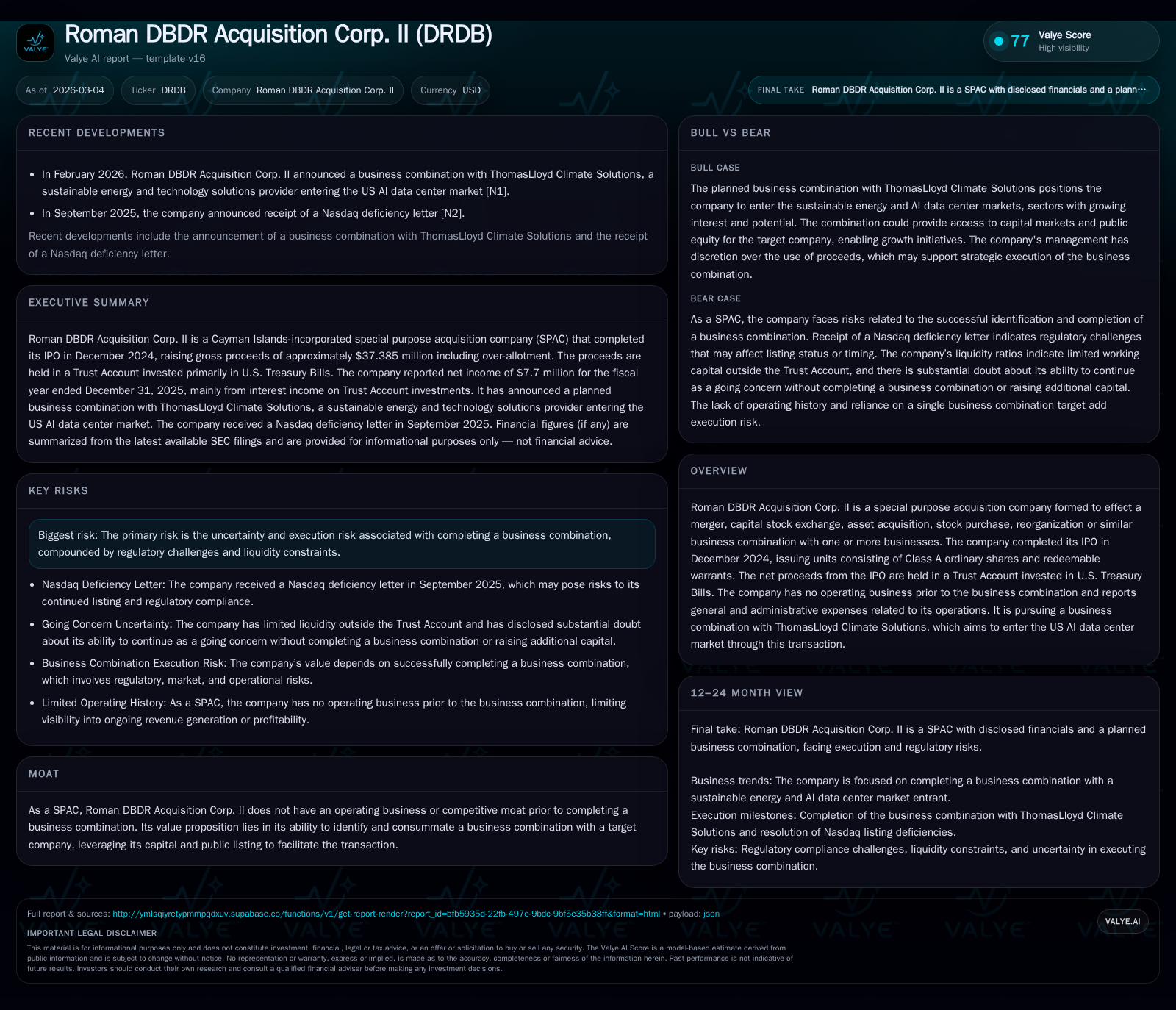

Roman DBDR Acquisition Corp. II, a special purpose acquisition company formed in late 2024, seeks growth by completing a business combination with ThomasLloyd Climate Solutions, aiming to enter the U.S. AI data center market. Historically, as a SPAC, the company has no operating business and generates losses related to administrative expenses while holding IPO proceeds in trust. Its future hinges squarely on successful deal closure amidst regulatory and execution risks. Financially, it operates with low liquidity outside its trust account and generates negative operating cash flows as it invests in the merger process, without paying dividends or repurchasing shares.

Company Background and Structure

Roman DBDR Acquisition Corp. II (ticker: DRDB) is a special purpose acquisition company (SPAC) formed in 2024 to facilitate mergers or similar business combinations that transform it from a capital pool vehicle into an operating public entity [S1][N1]. It completed an initial public offering (IPO) in December 2024, issuing units comprising Class A ordinary shares and redeemable warrants, raising gross proceeds exceeding $230 million after exercising over-allotment options [S5]. These proceeds are held primarily in an interest-bearing Trust Account invested in U.S. Treasury Bills intended to finance an eventual business combination.

Until consummation of its initial business combination, Roman DBDR holds no active operations or revenue-generating businesses but incurs general and administrative expenses related primarily to maintaining corporate functions and pursuing a target entity [S1][F1].

Historical Performance and Financial Overview

As a SPAC shell, traditional revenue metrics do not apply; financials reflect IPO-related accounting entries, administrative costs, and equity structural changes.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 8 | -1288906 | -2 | +3362.5% |

| 2024 | 0 | -411797 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -994.4 |

| 2024 | 18.7 |

Source: SEC companyfacts cache [F1].

Operating losses increased sharply in FY2025 compared to FY2024 reflecting higher administrative expenses likely linked to merger activities [F1]. Operating cash flows remain negative and deepened year-over-year as the company invests in pursuit of its business combination [F1]. The substantial net income increase is attributable to non-operating items such as mark-to-market adjustments on financial instruments typical for SPACs rather than recurring earnings [F1]. Liquidity outside the Trust Account is modest at approximately $183K at year-end 2025 with current liabilities exceeding current assets resulting in a current ratio of 0.35 [F1][S14]. Public shareholders retain redemption rights backed by Trust Account assets at about $10 per share.

Future Growth Prospects

Roman DBDR’s growth depends entirely on completing its announced merger with ThomasLloyd Climate Solutions [N1]. This target focuses on sustainable energy solutions for AI data centers within the U.S., responding to rising demand for green-powered infrastructure amid AI expansion [N1]. The transaction aims to transition Roman DBDR from a capital shell into an operating company exposed immediately to AI-driven climate-tech infrastructure markets.

Potential Growth Drivers:

- Entry into high-growth sustainable infrastructure markets tied to AI compute demand,

- Access to public equity capital markets post-merger for further funding,

- Leveraging ThomasLloyd’s vertical integration capabilities.

Key Risks and Constraints:

- Uncertainty around successful deal closing,

- Regulatory scrutiny typical for climate-tech transactions,

- Market volatility affecting valuation before closing,

- Operational challenges scaling capital-intensive infrastructure.

Forecasts and Milestones

The company has not provided explicit guidance or forecasts within filings or press releases [S3][N1]. Near-term milestones include:

- Signing definitive business combination agreements,

- Securing shareholder approval,

- Transitioning governance post-merger,

- Initiating operational rollout of U.S.-based AI data center projects. Investors should monitor forthcoming SEC filings such as proxy statements for detailed timing and terms [S3]. The deal must close within customary SPAC deadlines established at IPO.

Capital Allocation and Returns

As a pre-merger SPAC entity, Roman DBDR has not declared or paid dividends nor conducted share repurchases [S6][S13][F1]. Capital allocation focuses on preserving IPO proceeds within the Trust Account pending deployment toward qualifying targets meeting minimum valuation requirements (at least 80% of Trust Account balance upon signing) [S5].

Return on equity is not meaningful due to net income driven by non-recurring accounting effects combined with negative shareholders’ equity resulting from temporary equity classification of redeemable shares subject to redemption rights [F1]. Sponsor interests reside mainly in nominal-cost Class B shares with locked voting rights pre-closing while waiving redemption rights on founder shares aligning incentives during merger pursuit [S19][S27].

Industry Context Analysis

Roman DBDR’s planned transformation via ThomasLloyd Climate Solutions aligns with major trends: accelerating adoption of green energy infrastructure amid surging AI workloads driving data center demand globally. The target’s focus on sustainable energy solutions addresses environmental regulations and corporate ESG mandates gaining prominence across sectors.

SPACs targeting climate-tech remain popular yet execution-dependent vehicles; success hinges on timely deal-making absent underlying operations beforehand. Roman DBDR’s timing captures sector momentum though competitive positioning depends critically on execution precision.

Conclusion

Roman DBDR Acquisition Corp. II exemplifies a SPAC transitioning from capital vehicle to operating entity through a pending transformative merger with ThomasLloyd Climate Solutions focused on AI-driven climate tech infrastructure. Until deal closure, financials reflect pre-deal administrative expenses offset against trust-held IPO liquidity amidst execution risks common across SPACs.

Market participants should track official announcements regarding merger progress alongside evolving regulatory landscapes shaping climate-tech infrastructure financing post-completion.

This analysis is based solely on available public filings and news reports as of March 2026 and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments