Datavault AI’s Explosive Revenue Growth Overshadowed by Deepening Losses and Nasdaq Compliance Risks

Rapid top-line expansion fails to translate into profitability amid liquidity constraints and listing challenges.

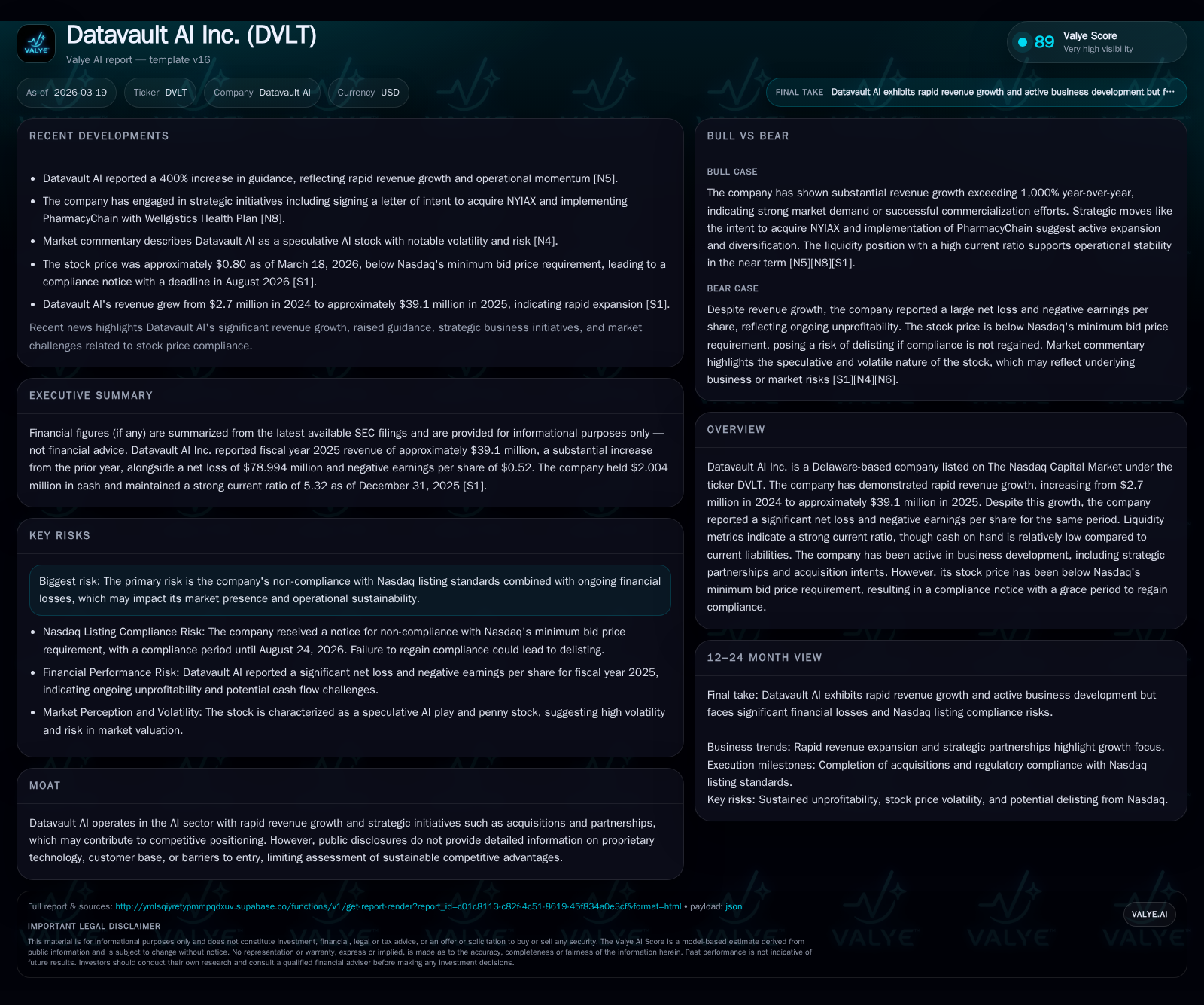

Datavault AI Inc. reported a remarkable surge in revenue from $2.7 million in 2024 to $39.1 million in 2025, reflecting over 13-fold growth. However, this growth coincided with escalating operating losses, pushing net losses to nearly $79 million last year. The company faces a precarious cash position relative to current liabilities despite a strong current ratio, while its stock trades below Nasdaq’s minimum bid price requirement, triggering a compliance notice. Strategic moves such as equity warrant dividends aim to stabilize the business, but financing pressures and legal risks continue to loom.

Corporate Overview and Industry Context

Datavault AI Inc., incorporated in Delaware and listed on the Nasdaq Capital Market under ticker DVLT, operates at the intersection of artificial intelligence and blockchain technologies. The company is positioned within sectors characterized by rapid innovation cycles and evolving regulatory frameworks.

Historical Performance and Growth Drivers

Datavault demonstrated extraordinary revenue growth, expanding from approximately $2.7 million in FY2024 to nearly $39.1 million in FY2025—a year-over-year increase of roughly 1362% [F1]. This rapid top-line expansion underscores aggressive scaling efforts through product development and market penetration initiatives.

However, this growth has been accompanied by substantial operating losses that deepened to approximately -$32.5 million in FY2025 from -$21.1 million the previous year. Net losses similarly expanded sharply, reaching nearly -$79.0 million compared to -$51.4 million in FY2024 [F1]. These results indicate that the company remains in an investment phase with significant expenditures outpacing revenues.

Operating cash flow was negative $23.6 million in FY2025, indicating continued cash consumption despite modest capital expenditures of $380 thousand—suggesting restrained investment in fixed assets or R&D capitalization [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 39 | -79 | -24 | -32 | +1361.8% | -53.7% |

| 2024 | 3 | -51 | -18 | -21 | +28.4% | -174.6% |

| 2023 | 2 | -19 | -15 | -21 | -38.1% | -15.9% |

| 2022 | 3 | -16 | -18 | -18 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -24 | -33.2 |

| 2024 | -18 | -60.0 |

| 2023 | -15 | 363.0 |

| 2022 | -18 | 809.2 |

Source: SEC companyfacts cache [F1].

Table: Datavault AI Inc.’s key financial metrics highlight rapid revenue growth alongside sustained losses (all figures USD) [F1]

Liquidity Position and Capital Structure

The balance sheet reflects a strong current ratio of approximately 5.32 with current assets near $143 million against current liabilities of roughly $26.9 million [F1]. Nonetheless, cash and cash equivalents stand at only about $2 million—raising concerns about immediate liquidity given the scale of near-term obligations.

Equity increased markedly to nearly $238 million by the end of FY2025 from approximately $85.7 million in FY2024 due primarily to capital raises supporting operational expansion [F1]. Despite this improvement in net assets, ongoing negative earnings result in an approximate return on equity of -33%, underscoring profitability challenges.

Regulatory and Listing Risks

Datavault’s common stock is trading below Nasdaq’s minimum bid price requirement which has resulted in formal non-compliance notifications from the exchange. The company has been granted extensions through August 24th, 2026 to regain compliance or face potential delisting [S21][S26]. Management is considering corporate actions such as reverse stock splits to address these issues.

Strategic Initiatives and Capital Allocation

The board has adopted an unconventional capital allocation approach by declaring dividends payable through warrants exercisable contingent upon holders possessing Dream Bowl Meme Coin II tokens—a novel integration of traditional equity instruments with blockchain-based assets [S4][S19][S22].

No traditional dividends or share repurchases have been reported; instead shareholder value distribution focuses on warrant issuances aligned with emerging tokenized asset frameworks.

Operational Risks and Outlook

Key risks highlighted include dependency on third-party semiconductor suppliers critical for product delivery; regulatory uncertainties surrounding AI and blockchain technologies; concentration of revenue among a few customers; and active legal proceedings alleging contractual breaches and securities violations filed in early March 2026 [S1].

Growth strategies emphasize acquisitions and strategic partnerships designed to scale offerings but carry inherent execution risks.

Analytical Summary

Datavault AI illustrates a profile of rapid revenue expansion offset by deepening losses and persistent cash burn amid liquidity constraints. The company’s innovative capital strategies involving token-linked warrants reflect attempts at creative financing solutions within complex regulatory environments.

Nasdaq listing compliance challenges add uncertainty alongside legal risks that require ongoing monitoring. Without clear near-term profitability or positive free cash flow trends—currently estimated at negative $23.99 million—continued financing will be essential for sustaining operations.

This analysis is based on publicly available SEC filings ([S1], [S3]-[S29]) complemented by detailed financial data from XBRL disclosures ([F1]). It does not constitute investment advice but aims to provide an informed perspective on Datavault AI’s financial condition and strategic positioning.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments