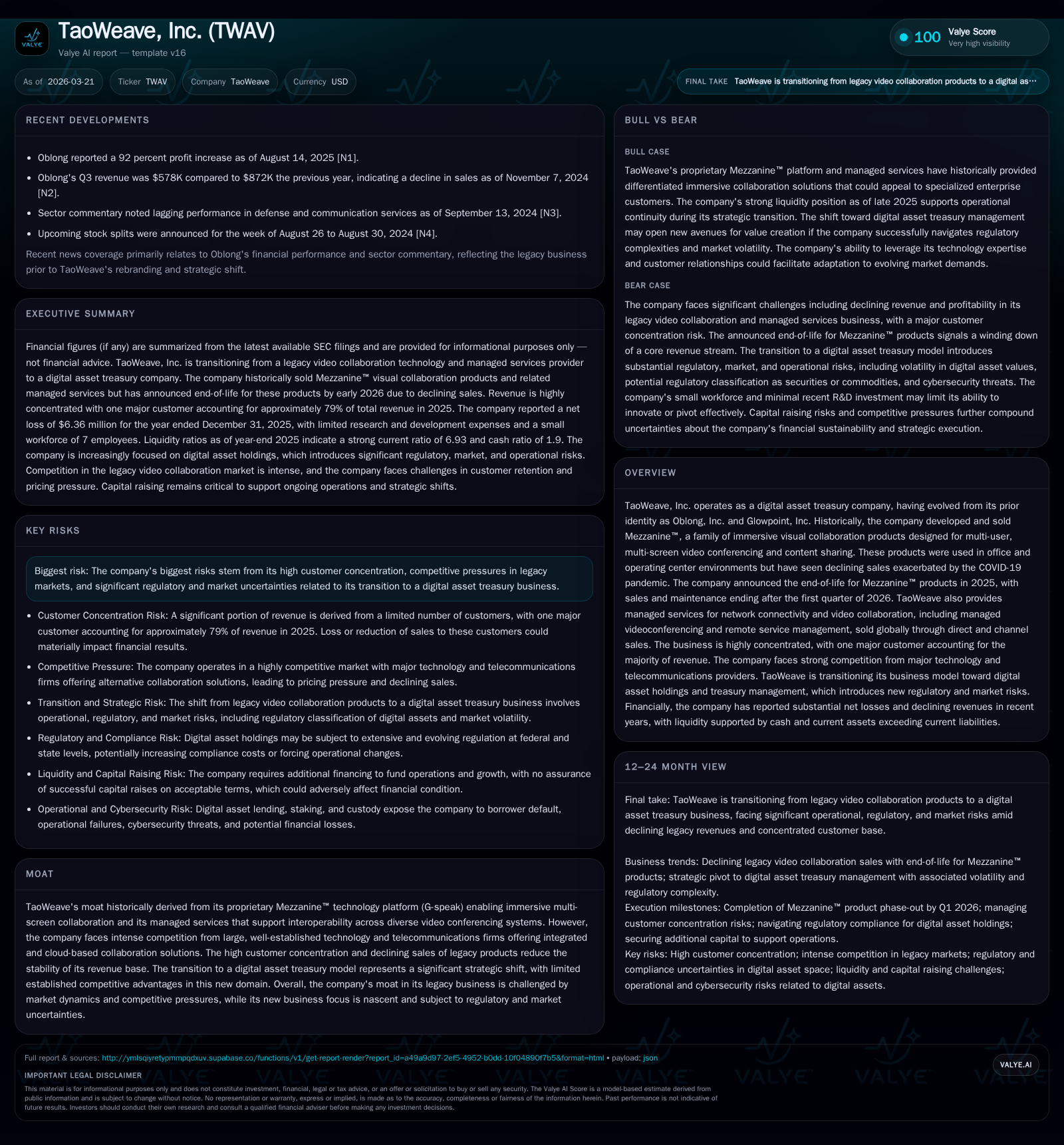

TaoWeave's Transition: From Immersive Visual Tech to Digital Asset Treasury

TaoWeave exits its legacy immersive collaboration business while venturing into digital asset treasury amid ongoing revenue concentration and financial challenges.

TaoWeave, Inc. has wound down its legacy Mezzanine™ immersive multi-screen collaboration platform, a product line severely impacted by the COVID-19 pandemic and broader industry shifts, culminating in its end-of-life announcement in 2025. The company faces elevated risks from extreme customer revenue concentration—one client accounted for nearly 80% of 2025 revenues—and intense competition in video collaboration and managed network services. TaoWeave is repositioning as a digital asset treasury firm, a substantial pivot marked by uncertain growth prospects and regulatory hurdles. Financially, the firm continues to report losses and negative cash flows, though liquidity remains supported by equity capital; capital raises will be critical to sustain operations during this transformation.

Legacy Roots and Revenue Trajectory: The Mezzanine™ Era’s Downturn

TaoWeave's heritage centers on its proprietary Mezzanine™ platform, a suite of immersive collaboration solutions enabling multi-user, multi-screen spatial interactions designed to enhance videoconferencing environments ranging from small teams to innovation centers. This platform leverages the G-speak technology underpinning dynamic content sharing across multiple displays via unique spatial input devices. Historically positioned within office and operating center settings, Mezzanine™ offered turnkey configurations (200-, 300-, and 600-Series) that sought to disrupt traditional video conferencing paradigms.

However, the commercial outlook deteriorated over recent years, significantly exacerbated by the COVID-19 pandemic which disincentivized centralized office use and larger physical collaboration spaces. TaoWeave progressively curtailed investments in both sales/marketing (which dropped dramatically from $181K in 2024 to $21K in 2025) and research/development (only $10K R&D spend in 2025), signaling strategic abandonment of this legacy product line [S1][S3][F1].

Consequently, the Company announced in 2025 the formal end-of-life for Mezzanine™, scheduling cessation of all sales and maintenance contracts after Q1 2026 [S1]. Financially this shift aligns with an ongoing decline in revenues driven by dwindling orders and related service contracts.

Financial Performance Overview

The following table summarizes TaoWeave’s annual key financials reflecting this trajectory through FY2025:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -6 | -3 | -3 | -57.2% | |

| 2024 | -4 | -3 | -4 | +7.8% | |

| 2023 | -4 | -3 | -4 | 0 | +80.0% |

| 2022 | -22 | -6 | -22 | 11000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -90.4 | |

| 2024 | -101.0 | |

| 2023 | -3 | -79.7 |

| 2022 | -6 | -606.6 |

Source: SEC companyfacts cache [F1].

*Partial computed where data allows; revenue figures are not explicitly provided [F1]. Capex trends reflect near-zero reinvestment supporting shutdown of legacy operations [F1].

Despite narrowings in operational losses since the peak detriments experienced in FY2022 amid pandemic disruptions and intensifying competition [S1], TaoWeave remains significantly loss-making with negative cash flow indicating ongoing structural challenges exacerbated by legacy product decline.

Concentration Risks Amid Legacy Sales Decline

The severity of TaoWeave’s customer reliance risk is underscored by its extraordinarily high revenue concentration: one major client contributed approximately 79% of total consolidated revenues for FY2025 (down slightly from ~85% in FY2024) [S4][S6][S7][F1]. Such dependence creates material vulnerability through single-customer funding variability — any contract non-renewal or renegotiation could swiftly destabilize financial results.

This risk converges with heightened cyclical volatility where dominant customers’ operational or strategic shifts bear disproportionate effects on revenue timing and volume. Coupled with longer sales cycles typical in channel partner engagements plagued by sporadic purchase behavior further compounds predictability challenges.

The collaboration market landscape also stacks significant headwinds: TaoWeave contends against entrenched cloud-based incumbents like Cisco WebEx and Zoom offering integrated platforms with broader ecosystems alongside Google Suite and Microsoft Teams encroaching into virtual co-working environments [S4]. These competitors leverage cloud scalability over localized spatial computing solutions — despite the latter’s unique immersive interaction attributes — eroding pricing power amidst commoditized offerings.

Managed services revenues suffer similarly from competition with telecom giants such as British Telecom and AT&T as well as managed service providers who integrate videoconferencing infrastructure into bundled solutions [S4]. The combination of limited pricing leverage plus dependency on underlying carrier networks accentuates margin pressure.

Shifting Gears: The Digital Asset Treasury Model Emerges

Faced with persistent declines in its core offerings and intensifying competition coupled with diminishing market relevance for hardware-centric collaboration solutions post-pandemic era usage patterns [S1], TaoWeave undertook a pronounced strategic pivot: it now operates primarily as a digital asset treasury company [S8][S9][S14]. This repositioning marks a substantial departure from development and sale of physical/video collaboration hardware/software to managing cryptocurrency or blockchain-based assets aimed at public investors.

However this transition is nascent with many uncertainties:

- There is limited evidence so far of established competitive moats analogous to G-speak’s historic spatial computing innovations.

- Regulatory scrutiny remains high for entities holding or trading digital assets given potential liabilities under U.S. laws such as the Investment Company Act; classification could materially inhibit business scope if deemed an investment company [S8][S9].

- Market adoption curves remain unclear alongside technological risks inherent in digital treasury management.

This reorientation illustrates a classic case of corporate reinvention triggered by obsolescence pressures but carries non-trivial execution risk alongside unclear revenue visibility.

Competitive Pressures Across Collaborations and Managed Services

Legacy Mezzanine™ solutions historically excelled at delivering multi-display experiences addressing interoperability gaps that conventional videoconferencing struggled with due to protocol fragmentation across vendors (Cisco vs Polycom vs Microsoft ecosystems) [S17]. G-speak technology supported spatial input allowing users effective control across distributed screens enhancing decision speed.

However recent years witnessed accelerated migration towards cloud-hosted conferencing platforms that do not require specialized hardware nor complex spatial interactions but leverage browser/mobile ubiquity instead [S4]. Consequently:

- TaoWeave faced declining managed services revenues primarily due to churn as customers moved towards integrated cloud offerings like Zoom Rooms or Microsoft Teams Rooms.[S17]

- Telecommunications carrier reliance implicit in network managed services limits operational control; carriers can constrain access or pricing arbitrarily impacting TaoWeave service delivery capability and profitability.[S7][S10]

This situational context highlights waning differentiation benefits from physical immersion technologies vis-à-vis highly scalable software-defined communication paradigms dominating enterprise budgets.

Capital Structure, Cash Flows, and ROE Trends: A Financial Health Checkup

TaoWeave’s latest financial snapshot reveals continuing distress albeit with some signs of operational cost discipline:

- Operating income improved year-over-year decreasing losses by nearly $1.24 million (YOY change +29.5%) down to negative $2.96 million in FY2025 from negative $4.20 million prior year [F1].

- Net losses remain deep at $6.36 million highlighting continued unprofitability [F1].

- Operating cash flows remain negative at $3 million but have slightly improved (+11.5%) consistent with reduced working capital needs or better collections.[F1]

- Capital expenditures have ceased completely indicating no new investments aligned with wind-down strategy.[F1]

- Equity base grew notably to $7 million supporting adequate liquidity; current ratio near seven times (6.93x) underscores short-term solvency strength boosted likely by recent financing rounds.[F1][S8][S11][S12][S13][S21]

- Return on equity stands deeply negative (~-90%), reflecting prolonged unprofitability [F1].

- No dividends or share buybacks have been recorded recently pointing toward capital conservation posture rather than shareholder returns [F1][S21].

The company acknowledges the need for further capital raises through warrant exercises or new securities issuances to fund ongoing operations or growth initiatives especially focused on the digital asset treasury business [S8][S19][S20][S21].

What Lies Ahead: Growth Prospects, Milestones, and Critical Unknowns

Absent explicit management guidance or publicly stated forecasts for future revenue or earnings growth related to the new digital treasury focus per available filings, key performance triggers will include:

- Successful completion of Mezzanine™ product/support sunset after Q1 2026 without residual liabilities impacting financials.[S1]

- Securing diversified clients beyond the dominant single customer currently generating ~79% revenue—without broadening customer base volatility will persist.[S4]

- Execution milestones around fundraising efforts including exercise of outstanding warrants raising fresh capital required for digital asset expansions.[S8][S21]

- Navigating initial regulatory approvals/licenses relevant to holding/managing crypto assets within U.S jurisdictional constraints given exposure under Investment Company Act provisions.[S8]

- Demonstrating scalable operations capability within emerging crypto treasury markets against sharper regulatory oversight complexity compared with prior technology product markets.

Market observers should scrutinize quarterly updates on capital raise status plus any commentary relating to regulatory developments affecting dTAO positioning as harbingers for valuation recalibrations.

Potential Hurdles: Customer Dependence and Regulatory Complexities

Customer concentration risk exposes TaoWeave profoundly not only financially but operationally since contract renewals are often unpredictable subject to counterparty creditworthiness changes possibly intensified by macroeconomic downturn dynamics or insolvency events affecting major clients [S6][S7].

Telecommunications carrier dependencies impose vendor risk inherent when critical network infrastructure providers alter terms or restrict access adversely affecting managed services quality/reliability or cost structure resulting potentially in lost contracts or increased expenses [S7][S10].

Regulatory uncertainty is acute particularly around being designated an "investment company" under U.S federal statutes which imposes stringent restrictions on financing structures transactions with affiliates capital frameworks severely constraining business model viability if triggered inadvertently [S8][S14].

Cybersecurity vulnerabilities within TaoWeave’s operational environment plus those prevailing among customer networks represent latent risks that could lead to data breaches latency claims reputational damage materially affecting business continuity restrictions under insurance policies causing unforeseen expenses [S14].

These factors collectively elevate execution risks intrinsic during this metamorphosis phase demanding adept regulatory navigation robust vendor relationship management plus enhanced governance capabilities.

This analysis synthesizes publicly filed SEC disclosures including recent form 10-K/10-Q documents alongside structured financial data points but does not provide investment advice nor price forecasts. Readers should consider detailed official filings directly for compliance purposes before forming conclusions regarding TaoWeave's future prospects.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments