Enbridge Inc: Strategic Infrastructure Investments and Regulatory Navigation Amid Market Uncertainties

An in-depth examination of Enbridge's asset investments, regulatory landscape, and resilience in navigating trade and market challenges.

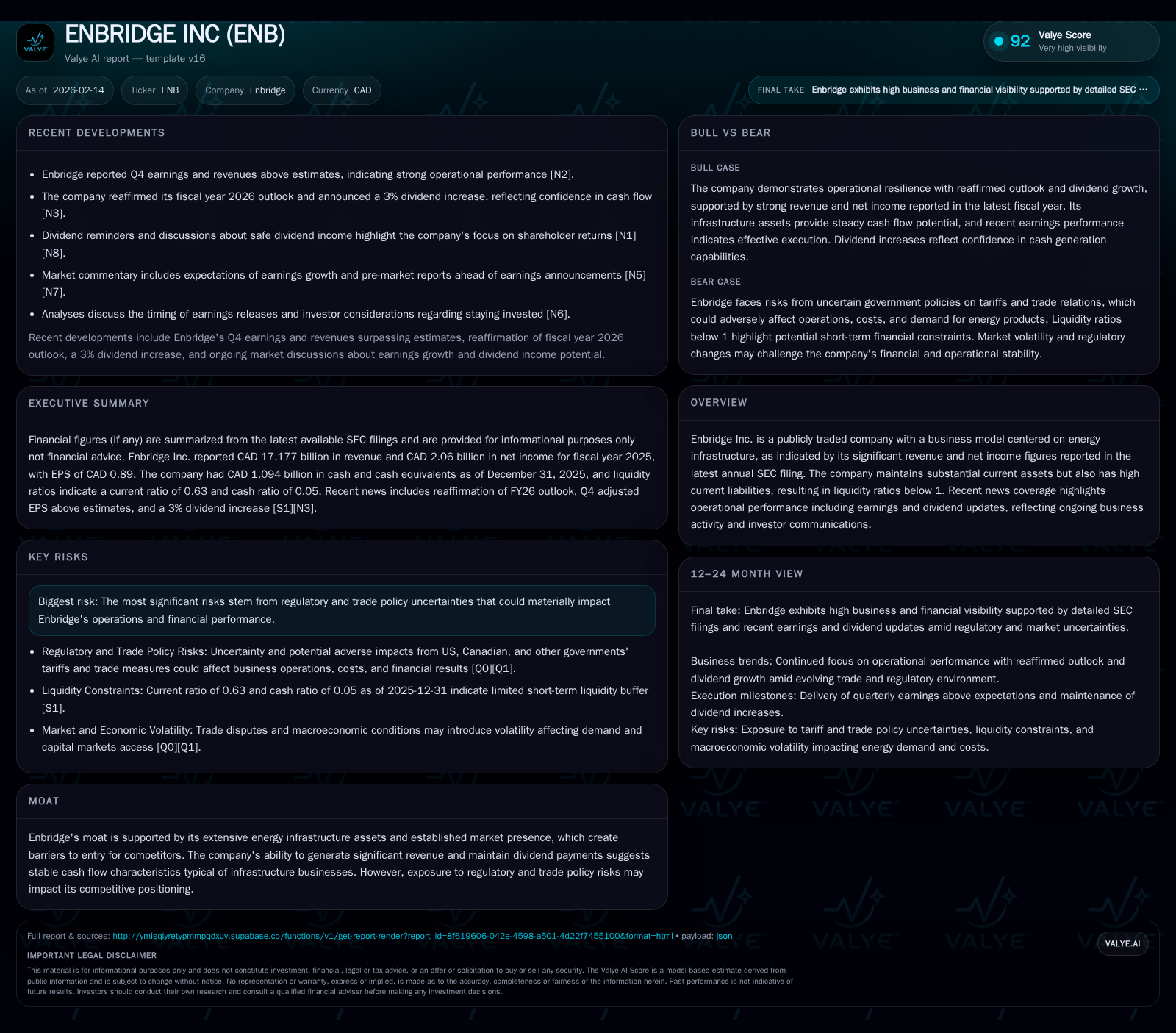

Enbridge Inc. remains a pivotal player in North American energy infrastructure, underscored by robust capital commitments targeting longevity and efficiency improvements. Recent financial disclosures reveal strong revenue and earnings performance despite liquidity pressures from a sub-1 current ratio. The company’s proactive engagement with multiple regulatory rate cases and adaptive dividend policy highlight its efforts to sustain cash flows amid evolving energy market dynamics. Simultaneously, Enbridge contends with increasingly complex trade policy crosswinds and cybersecurity threats, while leveraging Indigenous partnerships to bolster stakeholder relations and long-term access.

Enbridge’s Capital Blueprint: Investing in Longevity and Efficiency

Enbridge’s strategic investments underpin its commanding presence in North America’s energy landscape. Central to this blueprint is the announced US$1.3 billion capital commitment for the Mainline System through 2028, aimed at extending the physical life of key pipeline assets while enhancing reliability and operational efficiency [S1]. This approach aligns with Enbridge’s tolling settlement framework, which allows the utility to earn returns on invested capital, effectively locking in value over the long term.

Moreover, the July 2025 equity infusion of approximately $736 million by Stonlasec8 Indigenous Investments Limited Partnership—representing 38 First Nations groups—into the BC natural gas pipeline system signals a strategic partnership extending beyond capital gains [S1]. This equity participation not only supplies crucial funding but also consolidates social license, reducing operational friction that can accompany infrastructure projects crossing Indigenous lands.

Through these focused investments, Enbridge reinforces its moat by maintaining and upgrading an extensive energy infrastructure network critical to North American markets. The emphasis on asset longevity supports rising demand scenarios while managing cost efficiencies critical for competitive toll setting under regulated frameworks.

Financial Pulse Check: Healthy Earnings Against Liquidity Constraints

Recent financials highlight a dual narrative: robust profitability juxtaposed with working capital tightness. Enbridge reported CAD 17.2 billion in revenue alongside a net income of CAD 2.06 billion for fiscal year 2025 [F1], reflecting continued operational strength amid an evolving energy environment. Earnings consistently beat expectations per recent quarterly updates, reinforcing confidence in core business segments [N1][N7].

However, liquidity metrics merit close attention. The current ratio stands at approximately 0.63 (current assets CAD 13.2 billion vs current liabilities CAD 21 billion) [F1], signaling potential short-term funding pressures—a common feature within capital-intensive infrastructure companies that often carry high levels of payable obligations tied to ongoing project expenditures.

This imbalance underscores the importance of efficient cash management strategies during periods marked by elevated capital deployment and regulatory scrutiny. While dividend increases confirmed by management demonstrate available free cash flow [N7], maintaining liquidity without compromising operational flexibility will be essential as Enbridge pursues its expansive investment agenda.

Regulatory Hurdles: Navigating Rate Cases and Energy Board Interactions

Enbridge faces a complex mosaic of regulatory proceedings influencing revenue recovery and return expectations across multiple pipeline systems. The Algonquin Gas Transmission and Maritimes & Northeast U.S. rate cases both reached settle-in-principle agreements approved by FERC in April 2025, providing effective rates as early as December 2024 or January 2025 [S1]. These agreements illustrate how negotiation dynamics can reduce uncertainty, balancing stakeholder interests.

Nonetheless, some proceedings remain volatile. For example, East Tennessee Natural Gas filed a rate case in April 2025 with subsequent FERC suspension orders subject to refund mechanisms; settlement talks continue [S1]. Similarly, Vector Pipeline's consolidated rate case reached a settlement principle expected for FERC approval within early 2026 [S1].

In Canada, M&N Canada finalized toll settlements from January 2026 to December 2027 awaiting regulatory approval from the Canada Energy Regulator; decisions here will significantly influence cash flow visibility over the medium term [S1].

The Gas Distribution segment also encounters layered regulatory challenges — notably Enbridge Gas Ontario’s multi-phase incentive regulation framework where appeals concerning depreciation methods continue alongside approved price cap mechanisms incorporating earnings sharing clauses [S1]. Meanwhile, Enbridge Gas Ohio saw recent rulings adjusting revenue targets downward but maintaining support for continued infrastructure investment through capital expenditure programs [S1].

Navigating these diverse regulatory landscapes requires dexterity; outcomes directly affect allowed returns on equity (ROEs), capital recovery timelines, and thus long-term financial stability.

Dividend Fortitude: Rewarding Investors Amid Uncertainty

Despite external pressures ranging from regulatory complexities to market volatility linked to trade tensions, Enbridge continues to prioritize shareholder returns via its dividend policy. Following Q4 earnings exceedance announcements, the company declared a dividend increase of approximately 3% — reinforcing confidence in persistent cash flow generation even amid tightening conditions [N6][N7][N8].

This move aligns with Enbridge’s historically stable income-focused investor positioning, supported further by consistent free cash flow from durable pipeline toll frameworks [N10][N11]. In a volatile energy sector backdrop compounded by geopolitical shifts, such dividend fortification offers investors a reliable income stream.

The sustainability of this cash return hinges on timely rate case approvals coupled with prudent capital deployment – areas where the company’s track record suggests balanced risk management.

Trade Policy Crosswinds: Evaluating Tariff Risks and Market Volatility

Trade disputes cast an uneven shadow over Enbridge’s operational landscape primarily via US-imposed tariffs on steel and aluminum imports which feed into construction costs for pipelines and maintenance activities [S2]. Though some relief surfaced as limited exemptions or delays ensued, the specter of retaliatory tariffs from Canada introduces additional uncertainty regarding cost inflation.

Further compounding risk are announcements related to potential renegotiations of the United States-Mexico-Canada Agreement (USMCA). Modifications here could unsettle established energy market rules impacting cross-border flows of crude oil, natural gas, and liquids.

Collectively these tariff uncertainties have contributed to notable market volatility during much of 2025 – reverberating through supply chains, access to materials necessary for infrastructure upkeep/expansion, as well as possibly restricting capital market conditions essential for funding large-scale projects [S2].

While direct commodity export tariffs exclude certain energy products like crude oil currently, any escalation or extension of trade conflicts could quickly degrade economic fundamentals supporting demand for Canadian energy exports.

Cybersecurity Vigilance: Safeguarding Critical Energy Infrastructure

Recognizing their centrality to regional energy security, Enbridge has intensified focus on cybersecurity defenses amidst an increasing threat landscape [S1]. The company employs layered risk mitigation strategies including continuous third-party vendor assessments focusing on critical suppliers whose vulnerabilities could cascade into widespread disruption.

Internally, cybersecurity governance is anchored under the Chief Information Security Officer who oversees a dedicated Security Operations Center running around the clock year-round—complemented by automated alerting systems designed for rapid threat detection and response [S1]. Employee cyber hygiene is aggressively pursued via mandatory awareness campaigns alongside phishing simulation exercises tailored especially for higher risk cohorts within operations technology sectors.

Although no material breaches have compromised operations or financial integrity so far, this proactive posture diminishes risk exposure that regulators increasingly scrutinize in essential service providers — potentially preserving reputational standing vital for customer trust and regulatory goodwill.

Stakeholder Synergies: Indigenous Partnerships and Market Positioning

The participation of Indigenous groups as equity partners in key pipeline assets exemplifies Enbridge’s broader strategy toward inclusive stakeholder engagement—a critical factor given evolving social licensing demands across infrastructure sectors [S1]. The BC Pipeline System holds particular prominence where Stonlasec8 Indigenous Investments owns roughly one-eighth interest—providing not only capital inflows but also aligning interests toward sustainable regional development.

Such arrangements help mitigate construction delays or legal conflicts more common historically in resource-based projects traversing Indigenous territories. By embedding meaningful partnerships into ownership structures, Enbridge enhances its competitive advantages via smoother project execution pathways alongside improved community relations.

This model also positions Enbridge favorably against peers less advanced in indigenous inclusion initiatives—improving resilience against shifts in political or regulatory attitudes affecting project viability.

Looking Ahead: Growth Prospects Versus Emerging Risks

Looking forward into FY26 and beyond, growth trajectories hinge critically on successful navigation through pending regulatory reviews including anticipated decisions from CER regarding Maritimes & Northeast Canada toll settlements expected within Q1 2026 as well as finalization of consolidated Vector Pipeline rates awaiting FERC approval [S1][N3][N4]. These rulings will materially influence allowed returns underpinning investment economics.

Parallel macro factors like lingering trade policy ambiguities remain wildcards capable of injecting cost inflation or demand shocks disrupting long-term forecasts [S2]. Inflationary pressures driven by tariff-related input costs may necessitate recalibration in contracting strategy or investment cadence.

Nevertheless, with reaffirmed guidance accompanied by steady dividend growth signals [N7], Enbridge projects cautious optimism in sustaining core business momentum supported by robust infrastructure assets complemented with proactive risk controls including cybersecurity oversight and stakeholder inclusivity.

Overall prospects must consider nuanced dynamics—where solid fundamentals meet increasingly complex externalities requiring vigilant execution capabilities across finance, regulation, operations, and public affairs domains.

Disclaimer: This analysis is based solely on publicly available information as of February 14, 2026; it does not constitute investment advice or recommendations. Readers should conduct further due diligence before forming views or making decisions related to Enbridge Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments