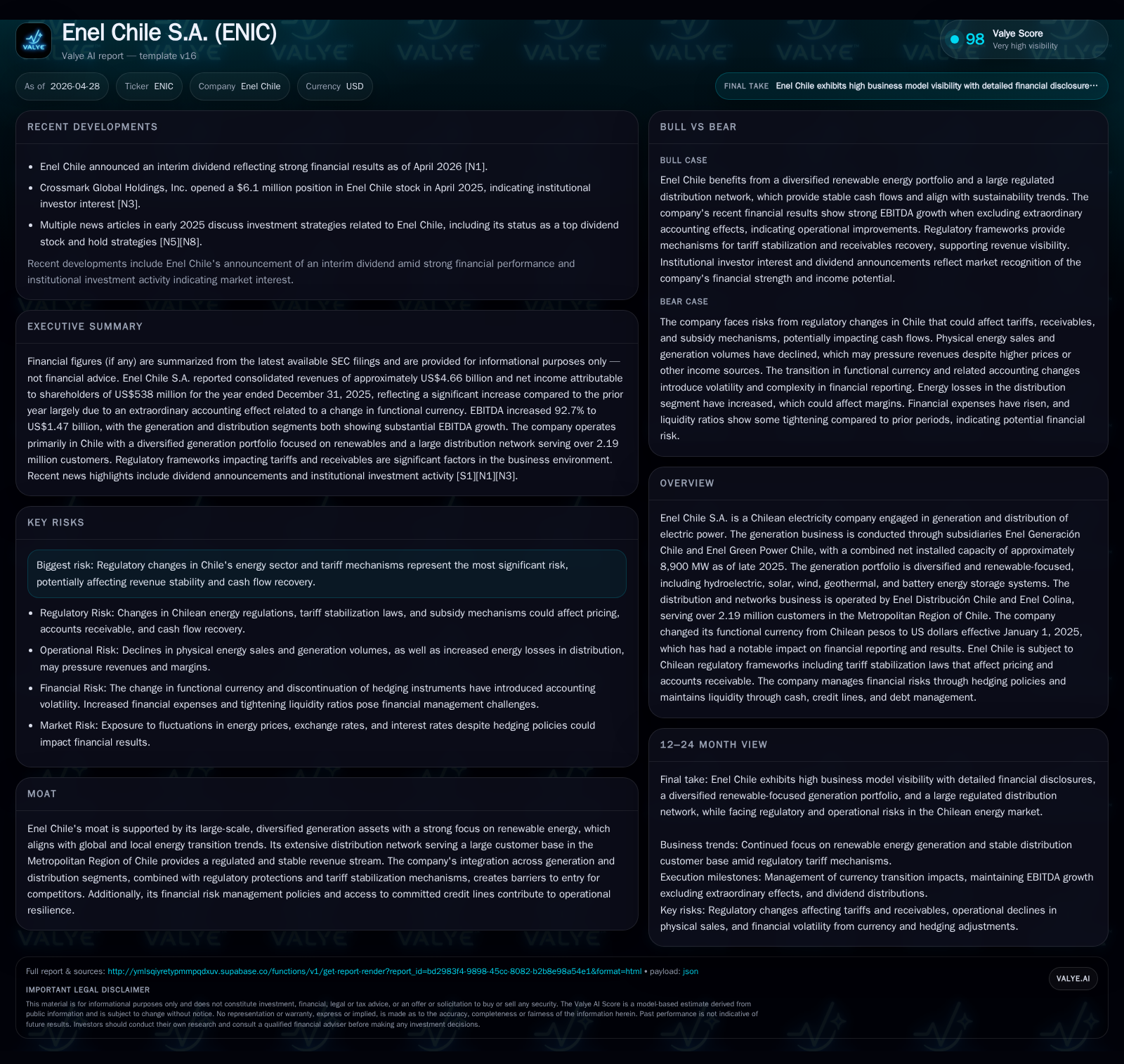

Enel Chile Advances Dividend Strategy and Currency Transition in 2025 Results

Enel Chile’s latest quarterly filings underscore a strategic dividend proposal amid operational shifts from its US dollar functional currency adoption and evolving tariff frameworks.

In its most recent quarterly disclosure, Enel Chile reported a net income surge driven largely by the cessation of USD revenue hedging following its functional currency transition to the US dollar effective January 2025. The company proposes a final dividend representing 50% of 2025 net income, aligning with prior payout policies and signaling confidence in its earnings stability. Enel Chile’s dual business model integrates a renewable-heavy power generation portfolio with a regulated distribution network serving over two million customers, creating a solid moat reinforced by Chilean regulatory protections and tariff stabilization mechanisms. Despite growth headwinds from lower hydroelectric output, the firm’s strategic focus on renewables capacity expansion and prudent financial management provide measured growth visibility.

Latest Quarterly Highlights and Strategic Dividend Proposal

Enel Chile’s operating updates for the year ended December 31, 2025, reveal several notable developments that set the company’s near-term trajectory. The Board of Directors has decided to propose a final dividend distribution of approximately US$269 million—equivalent to 50% of net income for 2025—to be submitted for shareholder approval at the Ordinary Shareholders’ Meeting on April 28, 2026 [S3]. This follows an interim dividend paid earlier in January and aligns with Enel Chile’s consistent capital return framework.

Operationally, the company posted a net income attributable to shareholders of US$538 million for full-year 2025, which includes an extraordinary positive impact from discontinuing revenue hedging instruments tied to foreign exchange following the switch of Enel Generación Chile's functional currency from Chilean pesos to US dollars as of January 1, 2025 [S2]. Isolating this effect reveals a slight net income decline versus adjusted 2024 figures; however, Q4 alone saw earnings rebound strongly to US$186 million compared to a negative US$292 million in Q4 of the prior year. This swing was driven predominantly by accounting adjustments related to foreign currency exposure cessation.

Simultaneously, operating revenues surged by over 10% year-on-year to US$4.66 billion supported by higher energy sales volumes and gas commercialization within generation operations [S2]. Cost controls contributed too: procurement and services expenses declined nearly 10%, although Q4 saw some increases mostly due to energy purchase costs in both generation and distribution segments.

The nuanced pricing evolution under new tariff decrees issued by Chile’s National Energy Commission (CNE) represents an ongoing headwind but one balanced by regulatory mechanisms designed to protect cash flow [S2]. Customers consuming less than or equal to 350 kWh/month pay prices adjusted semiannually with an added MPC charge facilitating debt amortization in energy pricing schemes. For higher consumption brackets above this threshold, prices reflect real-time energy and capacity costs plus similar MPC adjustments scheduled via average node price decrees for upcoming semesters. Such tiered price transparency signals evolving regulatory sophistication impacting Enel Chile’s revenue recognition dynamics.

Enel Chile’s Dual Business Model: Integrated Generation and Distribution Dynamics

The foundation of Enel Chile’s earnings lies in its integrated approach combining large-scale power generation assets with regulated distribution networks servicing over two million customers concentrated primarily in Santiago's Metropolitan Region [S1]. Its generation platform comprises subsidiaries Enel Generación Chile and Enel Green Power Chile, which together hold about 8.9 GW of net installed capacity as of late 2025 [S1]. This portfolio is noteworthy for its significant renewable orientation — encompassing hydroelectric plants, extensive solar arrays, modern wind farms, geothermal facilities employing indigenous resources, and cutting-edge battery energy storage systems that enhance grid flexibility.

The embedded flexibility of this diversified fleet cushions against single-technology volatility typical in emerging markets while positioning growth prospects in sync with global decarbonization mandates. Complementing generation is the distribution arm through Enel Distribución Chile and Enel Colina that manage more than two million customers under regulated tariff regimes with associated service quality delivery requirements [S1]. This segment provides stable recurring cash flows backed by a customer base exhibiting high switching costs arising from binding tariff frameworks enforced by the Comisión Nacional de Energía (CNE).

This vertical integration supports operational synergies where generation mix influences distribution network efficiency and mitigates volume risk on both sides via long-term contracts aligned with regulatory guidelines.

Regulatory Environment and Its Influence on Pricing and Revenue Stability

Chilean energy market regulation plays a pivotal role at defining Enel Chile’s revenue trajectory. The CNE governs tariff design including mechanisms such as tariff stabilization laws that aim to smooth consumer bill fluctuations linked to wholesale market prices. The recently approved Exempt Resolution No.633 modifies average node price setting methodologies by adjusting inflation application methods coupled with interest rate standards for non-adjustable peso transactions [S2].

Such adjustments bear material consequences for operating revenues as consumption bands are differentiated — lower-use consumers absorb price revisions semiannually with an incremental MPC charge added progressively while higher-consumption segments settle charges reflecting current nodal prices plus MPC components aimed at repaying accumulated system debts.

While these frameworks introduce regulatory constraints curbing full pricing power freedom for utilities like Enel Chile, they simultaneously protect cash flow recovery allowing predictable investment planning horizons despite external commodity price or currency volatility—an outcome critical in countries like Chile faced periodically with drought-induced hydropower supply shocks.

Competitive Positioning within Chile’s Energy Sector

Within Chile’s energy value chain, Enel Chile occupies a commanding position fueled by scale advantages and breadth of asset types absent among smaller or fossil fuel-dependent competitors [S1]. Its renewable-dominant portfolio dovetails neatly with government climate mandates supporting accelerated clean energy deployment leading up to legislated carbon neutrality targets.

Regulatory protection through established tariff stabilization laws alongside entrenched regulatory approvals for network expansions create formidable entry barriers that preserve incumbency benefits especially in tightly contested urban centers like Santiago metropolitan area served exclusively by Enel’s distribution subsidiaries. Furthermore, stringent financial risk management practices including defined currency exposure limitations bolster its resilience amid volatile commodity price environments prevalent across Latin America.

Growth Prospects Anchored in Renewables and Customer Base Expansion

Looking ahead, incremental growth opportunities exist principally through selective renewable capacity additions beyond the core base of ~8.9 GW along with augmentations in battery storage enabling enhanced dispatchability supportive of grid modernization efforts [S1]. Project development pipelines targeting solar-wind hybrid projects as well as geothermal enhancement signal intent to capture rising demand segments empowered by government incentive programs encouraging clean infrastructure investments.

Expansion potential also revolves around deepening penetration within existing distribution footprint where population growth trends combined with electrification drives elevate future load curves sustainably under regulated tariff remuneration formulae [F1]. However, natural constraints such as hydrological variability pose cyclical volume limitations tempered somewhat by contract indexing strategies that mitigate direct profit erosion during drought cycles. This balance highlights a predominantly structural rather than purely cyclical demand story.

Key Operational Risks and Regulatory Challenges Ahead

The primary operational risks encompass shifts in regulatory tariffs or policy reforms that could alter price realization paradigms adversely impacting cash flow stability [S1][S2]. Chilean authorities occasionally recalibrate compensation formulas influencing effective utility margins which could require recalibration of corporate strategies including capital allocation priorities.

Moreover, commodity price volatilities remain relevant given fuel dependencies albeit mitigated substantially via hedges indexed primarily against natural gas volumes at Henry Hub prices and coal contracts—extending hedging coverage into coal sales contracts further exemplify active risk management initiatives deployed by management [S1]. These efforts partially offset exposure though residual risks persist given international commodity market gyrations.

Financial Overview: Liquidity, Capital Structure, and Cash Flow Analysis

As per the most recent disclosures ending December 31, 2025, Enel Chile maintains a current liquidity ratio marginally below unity at approximately 0.91 times driven by internal liquidity reallocations including upward reclassification into other current financial liabilities totaling US$238 million—a reflection primarily attributed to reclassified short-term portions of longer-term debt obligations including bonds and loans [S2][F1].

Cash flow from financing activities generated negative net cash flow totaling roughly US$771 million during fiscal year 2025 which incorporates dividend payouts aggregating US$351 million alongside interest payments nearing US$174 million plus principal loan repayments aggregating various sums toward affiliated entities [S2]. Despite these outflows exerting pressure on liquidity metrics near-term profitability improvements anchored in functional currency transition gains help sustain credit metrics within acceptable utility sector thresholds.

These financial discipline aspects underline confidence supporting ongoing capital investments targeted at sustaining renewable growth trajectories while honoring shareholder return commitments consistent with stated dividend policies.

Upcoming Milestones and Market Signals to Monitor

Key forthcoming events include the April 28, 2026 Ordinary Shareholders’ Meeting expected to ratify the Board-proposed final dividend payout totaling roughly US$269 million subject to adjustment deducting interim dividends already disbursed early this year [S3]. Market participants will also watch closely newly implemented tariff decree effects commencing first semester of 2026 impacting billing cycles across segmented customer classes influenced by MPC charges delineated previously.

Operationally relevant indicators such as quarterly generation volumes broken down by technology type post-Q4 signal execution continuity while regulatory announcements regarding potential further price-setting methodology refinements may materially influence future top-line momentum trajectories [S2]. These markers should serve as bellwethers for validating strategic execution amidst evolving sector dynamics.

This analysis reflects insights derived exclusively from current SEC filings dated March-April 2026 combined with corroborative company data sources without incorporating speculative forecasts or investment advice. The assessment emphasizes operational realities grounded in disclosed facts contextualized within recognized industry norms pertinent to Chile's regulated electricity market structure.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments