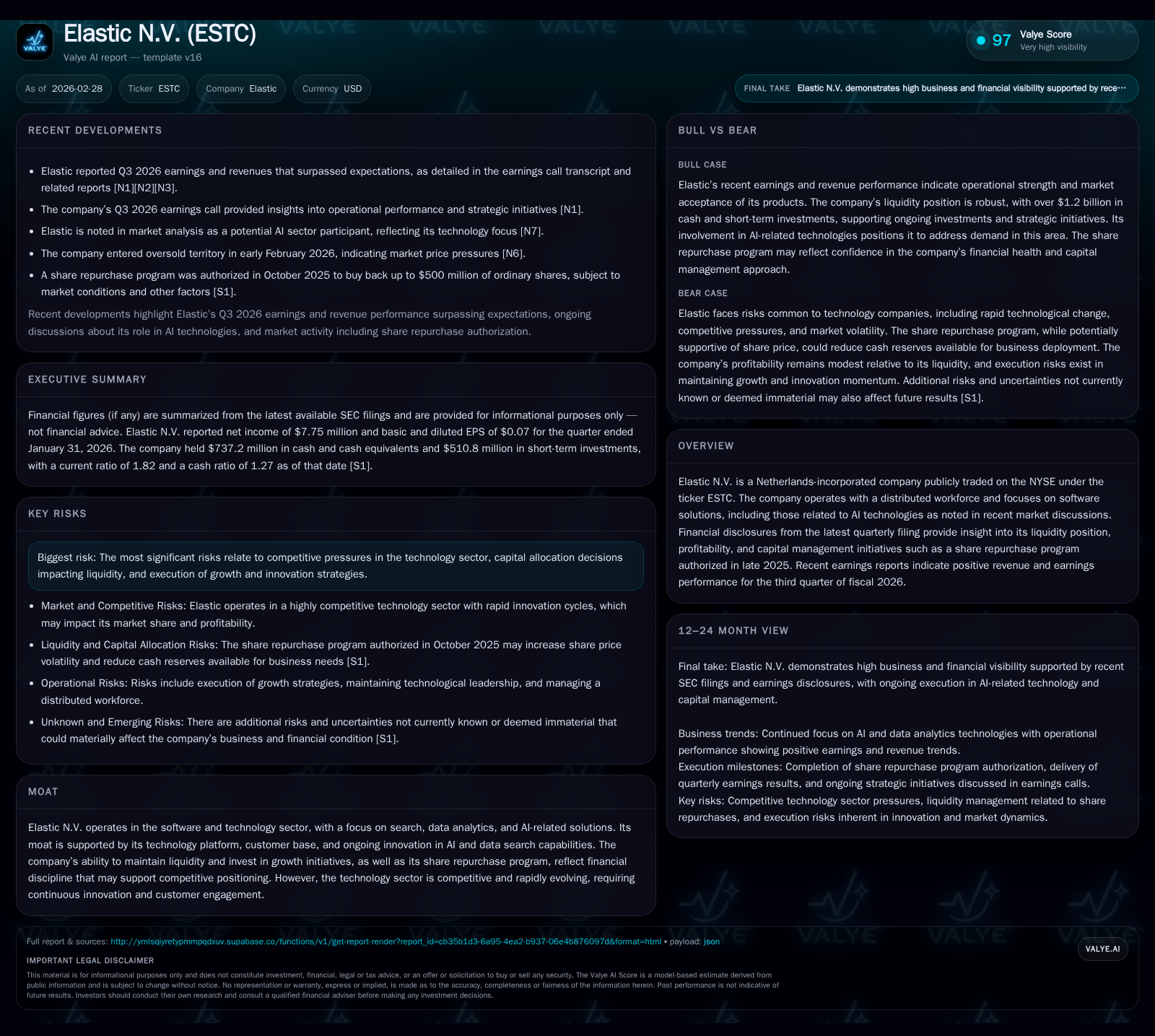

Elastic N.V.: Financial Resilience and AI Innovation Powering Up

Elastic’s operational turnaround and capital discipline underpin its strategic focus on AI-enhanced search and analytics solutions.

After years of operating losses, Elastic N.V. has shown marked improvement in cash flow generation and operational metrics, signaling a financial stabilization. The company is actively leveraging AI-driven innovations within its search and data analytics platforms to sustain growth momentum. Notably, recent quarterly results have surpassed market expectations, supported by disciplined liquidity management and a substantial share buyback authorization. However, competitive pressures and execution risks remain pivotal factors shaping Elastic’s future trajectory.

From Operating Losses to Positive Cash Flows: Tracing Elastic’s Financial Turnaround

Elastic N.V.’s recent fiscal history depicts a company transitioning from persistent operating losses toward healthier cash flow dynamics. In FY2025, Elastic narrowed its operating loss by 57.7% compared to prior years but continued reporting an operating income deficit of approximately -$54.9 million [F1]. Despite this, the quality of earnings improved notably—operating cash flow ballooned by 78.9% YoY to $266 million, evidencing stronger underlying fundamentals and operational resilience amid ongoing investments and expenses that kept net income negative at -$108.1 million during the same period [F1]. This divergence suggests investment cycles or one-time charges offsetting bottom-line profitability even as core operations stabilized.

The trend reflects both strategic cost controls and revenue growth initiatives taking root. Capital expenditures rose modestly by 25.9%, signaling continued spending on technology infrastructure essential for AI and platform development without aggressive expansion that might imperil liquidity [F1]. Equity growth of 25.6% underscores balance sheet strengthening through retained earnings and capital management.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -108 | 266 | -55 | 4 | -275.2% |

| 2024 | 62 | 149 | -130 | 3 | +126.1% |

| 2023 | -236 | 36 | -219 | 3 | -15.9% |

| 2022 | -204 | 6 | -174 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 262 | -11.7 |

| 2024 | 145 | 8.4 |

| 2023 | 33 | -59.2 |

| 2022 | 3 | -49.1 |

Source: SEC companyfacts cache [F1].

'Operating income' and other data from [F1]; %YoY calculated based on stated annual values.

Evolving Business Model with AI-Enabled Search and Data Analytics Platforms

Elastic continues advancing its core technology portfolio with an intensified focus on artificial intelligence embedded into its search platform offerings. Industry practitioners recognize the critical importance of machine learning-powered search algorithms that dynamically adapt to data patterns for superior relevance—a domain where Elastic positions itself strongly [N7]. Moreover, Elastic's expansion into data observability solutions enhances usage metrics that promote higher platform stickiness by delivering real-time analytics with actionable insights for clients at scale.

This innovation thrust not only supports customer retention but aligns closely with escalating market demand for integrated AI capabilities within enterprise search environments, positioning Elastic as a strategic partner amid accelerating digital transformation trends noted in recent sector commentaries .

Recent Quarter Outperformance: Surpassing Market Expectations

Q3 fiscal year 2026 results demonstrated Elastic’s accelerating operational momentum by surpassing Wall Street’s revenue and earnings estimates—a notable positive inflection after prior fluctuating periods [N1], [N2], [N3]. According to management commentary during the Nasdaq earnings call on February 26, 2026, the company’s continued adoption of its AI-enhanced platform offerings contributed materially to top-line beat and margin improvements accessible through improved sales execution strategies combined with a controlled cost structure [S3].

Investors responded favorably as these results affirm Elastic's capacity to navigate competitive headwinds while scaling innovative software suites driving recurring revenues.

Capital Allocation Focus: Record Share Buyback Program and Liquidity Management

In October 2025, Elastic secured board approval for an open-ended share repurchase program authorizing up to $500 million of outstanding ordinary shares to be repurchased over time at management discretion based on market conditions, liquidity considerations, and other corporate factors such as trading volumes or share price fluctuations [S4], [S8]. This initiative marks a transition toward returning value to shareholders while maintaining flexibility.

The repurchased shares will be held as treasury stock, signaling confidence from leadership about the company’s valuation levels without compromising immediate cash reserve needs critical for ongoing tech investments.

Liquidity remains robust as evidenced by the current ratio of approximately 1.82 at the January 31, 2026 quarter-end ($1.79 billion in current assets vs $983 million current liabilities), indicating ample working capital buffer supporting day-to-day operations alongside strategic capital deployment plans also reflected in modest capex spending increases year-over-year $4.35M vs prior periods [F1], [S10].

Risks Underpinning Profitability Improvements: Competitive Intensity and Execution Challenges

Elastic candidly outlines significant risks inherent within fast-evolving technology sectors encompassing search, data analytics, and AI innovation domains where rapid obsolescence cycles can threaten market share without sustained R&D efforts and go-to-market effectiveness [S2], [S5], [S7]. Competition from entrenched incumbents as well as emerging cloud-native startups heightens pressure on pricing power and requires relentless innovation pipelines alongside successful execution of sales strategies.

Additionally, capital allocation decisions tied to share repurchases must balance against preserving sufficient liquidity for aggressive product development investments—missteps here could limit financial agility especially given wider macroeconomic uncertainties impacting software demand dynamics.

Key Metrics Recap: Profitability Gains, Cash Flows, and Return on Equity Analysis

Elastic’s approximate return on equity (ROE) for the latest full fiscal year stands near -11.7%, reflecting ongoing negative net income pressures despite improving profit contributions from operations [F1]. However, the positive free cash flow estimated at roughly $262 million (operating cash flow minus capex) indicates substantial internal resource generation capability fueling both organic growth initiatives and shareholder returns through buybacks.

This duality highlights a transitional stage wherein cash-generative operations gain footing but net income remains sensitive to investment cycles or one-time items affecting GAAP results.

What Investors Should Monitor Next: Growth Catalysts and Capital Deployments

Looking ahead, key indicators warrant close observation including escalations in AI solution adoption rates across client verticals which may be detailed in forthcoming quarterly disclosures—as suggested by industry analysts identifying Elastic among leading generative AI platform beneficiaries early into 2026 adoption waves [N7]. Monitoring actual share repurchase pace against authorized limits will reveal management’s confidence level amidst prevailing market conditions affecting free cash flow availability.

Moreover, executive incentives—particularly CEO Ashutosh Kulkarni's performance-based equity award structured around rigorous share price appreciation targets aligned with relative total shareholder return against Russell 3000 benchmarks—underscore strong leadership motivation for sustainable value creation over multi-year horizons extending to October 2030 under specified vesting scenarios incorporating service continuity and performance hurdles designed to trigger meaningful increment vesting only upon achieving substantial TSR milestones [S15], [S18], [S19].

These factors collectively frame Elastic’s trajectory where financial discipline converges with transformative AI innovation fronts under seasoned management stewardship.

This report reflects analysis solely based on provided company disclosures including SEC filings and recent news releases aggregated up to February 28, 2026. It contains no investment recommendations or price projections but aims to elucidate key operational trends, capital strategies, risks, and monitoring guidance relevant for institutional readers evaluating Elastic N.V.'s evolving business landscape.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments