GMTech’s Rapid Scale in Asian Smartphone Sales and Transition to Profitability Amid Limited Moat

GMTech pivoted sharply from IT consulting to smartphone distribution in Asia, achieving sizable revenue growth and net income in its second full year.

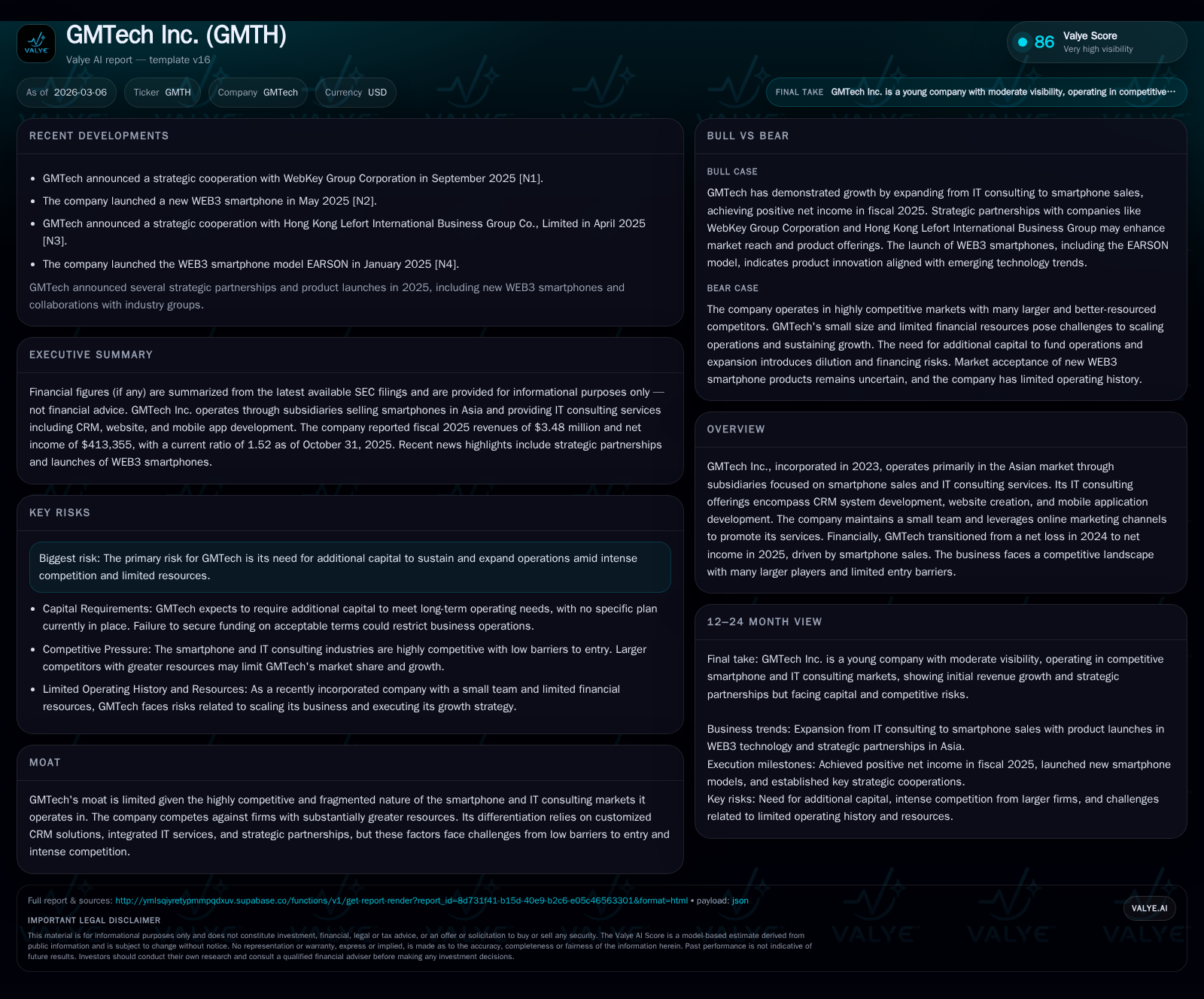

Founded in late 2023, GMTech Inc. swiftly shifted its business model from modest IT consulting services to wholesale and retail smartphone sales across Asia. This strategic realignment fueled explosive revenue growth from $52,800 in FY2024 to $3.48 million in FY2025 and pushed the company into net profitability with a $413,000 income in FY2025. Despite this progress, GMTech operates in highly fragmented markets with intense competition and minimal entry barriers, relying on customized CRM solutions and integrated IT offerings for differentiation. The company’s liquidity profile is modest with a current ratio of 1.52 and positive operating cash flow, but ongoing expansion necessitates further capital raises amid heightened operational expenses related to AI development and marketing investments.

Historical Performance: Explosive Growth From Niche Beginnings

GMTech Inc., incorporated at the tail end of 2023, initially operated as an IT consulting provider focused on CRM systems development, website construction, and mobile application solutions primarily serving clients within the Asian market [S1][S8]. In its inaugural fiscal year ending October 31, 2024, GMTech’s revenues were minimal at $52,800—derived solely from IT consulting services—with a net loss of approximately $32,557 reflecting early-stage expenses typical for a start-up entity [F1][S1].

The transformative pivot towards wholesale and retail smartphone sales via its subsidiary Shenggang Excellence Limited began in earnest during FY2025. This strategic shift drove a meteoric rise in revenues to approximately $3.48 million—a roughly 6,487% year-over-year spike—with smartphone trade constituting all the reported sales for that year [F1]. Importantly, this surge translated into positive net income totaling just over $413,000. The swing from loss to profit underscores enhanced operational efficacy enabled by scale increases and a more market-aligned business model [F1][S1].

Operating cash flow mirrored this trajectory: turning positive at about $142,617 after a negative flow the prior year. This reflects not only profitable operations but also active working capital management during rapid inventory build-up linked to smartphone distribution [F1][S1]. However, investing activities absorbed significant cash—$240,508—primarily due to issuance of notes receivable (non-trade) to non-related parties and purchase of property and equipment [F1][S1]. Financing activity trends indicate modest net outflows associated with promissory note repayments suggesting a cautious capital structure approach without reliance on large borrowings [F1][S3].

Historical performance (annual)

| FY | Rev ($mm) | Net ($) | CFO ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 3 | 413355 | 142617 | +6487.2% | +1369.6% |

| 2024 | 0 | -32557 | -54565 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 78.8 |

| 2024 | -29.8 |

Source: SEC companyfacts cache [F1].

Table: GMTech Annual Financial Summary showing rapid revenue scaling alongside return to profitability.

Business Model Dynamics and Market Context

GMTech’s dual-pronged operations combine smartphone sales through Shenggang Excellence Limited and bespoke IT consulting via Anptech Inc., both wholly owned subsidiaries focused geographically on the Asian markets [S8]. While the smartphone segment catalyzed the company’s top-line explosion in FY2025 through wholesale/retail distribution channels targeting diverse customer bases including resellers and end users [S8], the IT consulting segment remains relatively nascent.

Consulting services emphasize customized CRM deployments tailored to client-specific workflows alongside website and mobile app development featuring security enhancements and UI/UX design considerations [S24]. These offerings seek to complement smartphone sales by fostering integrated digital ecosystems for customers but operate in an intensely competitive landscape marked by fragmentation and numerous players ranging from global tech giants to SMEs [S20].

Barriers to entry are notably low across both sectors; thus differentiation hinges on the company’s ability to provide tailored CRM solutions coupled with comprehensive technical support—a value proposition that management believes can partially offset resource disadvantages against larger competitors [S20]. Yet emerging competitive threats remain palpable given market attractiveness.

Future Growth Prospects: Opportunities Tempered by Constraints

Management plans indicate continued emphasis on expanding smartphone trading volumes within Asian markets alongside bolstering IT consulting depth through innovative services such as AI development tools currently under pilot [S6][S13]. Marketing efforts are slated for escalation utilizing social media channels including Facebook and Instagram with targeted campaigns aiming to leverage executives’ personal networks supplemented by digital advertising strategies [S24].

Further revenue streams could materialize from enterprise mobility solutions tied to their mobile app offerings if successful penetration ensues. However, growth ceilings persist due to:

- Commoditized nature of smartphones limiting margin improvement;

- Intense price competition constraining gross profit expansion;

- Hiring challenges for skilled personnel amid localized tech talent shortages;

- Need for substantial capital infusion to fund marketing push and R&D initiatives including AI tool development;

- Regulatory compliance requirements currently assessed as low impact [S18][S20].

No explicit quantitative guidance has been disclosed beyond acknowledgments that additional funding rounds will be necessary within the next year or so — expected primarily through equity issuances which will dilute shareholders but provide essential runway [S6][S7][S10]. The absence of committed financing arrangements presently highlights operational risks related to sustaining growth momentum.

Capital Allocation and Financial Returns

GMTech’s approximate Return on Equity stood near an impressive ~78.8% at fiscal year-end October 31, 2025 — reflective largely of nascent equity base combined with early profitability rather than mature capital deployment effectiveness [F1]. Free cash flow generation appears positive albeit modest with operating cash flows exceeding capital expenditures though detailed capex was not extensively itemized beyond notes receivable issuance and minor property investments [F1][S13].

There are no records or announcements indicating dividends or share buybacks; financial strategy centers around reinvesting internally generated funds complemented by external capital raises for scaling operations as required [S25][S27][S28]. This approach aligns with typical profiles of rapidly growing startups trading off immediate returns for future expansion capacity.

Liquidity Profile and Financing Risks

At October 31st, 2025 GMTech held approximately $16K cash combined with merchant receivables above $164K and inventories nearing $802K—consistent with inventory builds supporting fast turnover smartphone sales [F1][S1][S10]. Current liabilities approximated $841K driven largely by deferred revenues ($615K), taxation payables ($91K), lease obligations ($73K), accrued liabilities ($14K), notes payable ($5K), and related party payables ($51K) [F1][S15]. This yields a healthy current ratio of about 1.52 suggestive of adequate short-term liquidity though working capital needs remain elevated.

Debt levels are low overall but the firm has historically relied on equity issuances (notably raising $140K common stock proceeds early on) supplemented by director loans without formal agreements for short-term financing buffer; no bank credit lines exist [S14][S21]. Forward-looking commentary warns about significant capital requirements looming within twelve months tied to expanding operating expenses arising from new technology investments like AI tools plus scaled marketing efforts needed for market penetration—necessitating external funding through equity/debt markets or loans which are inherently uncertain given competitive environment [S6][S17][S23].

Industry Insight: Competitive Intensity Shapes Strategic Reality (Analysis)

As observed widely across Asian tech distribution channels and IT service providers catering SMEs/wholesale customers alike, companies face relentless pricing pressure fueled by numerous suppliers capable of rapid entry without substantial investment hurdles. Unlike sectors driven by patented technology or strong brand loyalty where moats solidify over time via network effects or switching costs, the lack of proprietary products along with commoditized smartphone lines means margins compress rapidly unless unique value-added services accompany core product offerings.

This dynamic dictates that GMTech’s advancement hinges less on dominating supply chains than establishing sticky client relationships via flexible CRM customization coupled with consultative support—a labor-intensive strategy unlikely easily replicated but challenging to scale efficiently given small staff size mentioned ([N/A]). It is common here for firms adopting adjacent service bundles to eke incremental profits but sustained differentiation requires continuous innovation investment underpinned by stable funding.

Summary Takeaways

GMTech stands at an inflection point having demonstrated capability to exponentially expand revenues while transitioning into profitability within roughly two years following inception. The company harnessed the higher-volume smartphone distribution business as financial engine supported modestly by complementary IT consulting services emphasizing CRM system customizations intended to entrench client dependencies.

Yet strategic fragility arises from deeply fragmented market structures characterized by cutthroat competition among better-resourced incumbents plus customer sensitivity about switching costs outside specialized software realms. Liquidity constraints represent a key vulnerability since upcoming phases necessitate significant cash outlays aimed at marketing expansion alongside R&D ventures around artificial intelligence applications—the latter signaling ambition but also added execution risks.

Investors observing GMTech should prioritize monitoring quarterly disclosures for any announced equity or debt raises critical for preserving going concern status alongside evolving revenue mix shifts potentially enhancing profitability sustainably beyond initial gains accomplished predominantly through volume growth alone.

Disclaimer: This report is prepared solely for informational purposes referencing publicly available SEC filings dated up through March 6th, 2026. It does not constitute investment advice or recommendations regarding securities nor solicit any transaction related thereto.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments