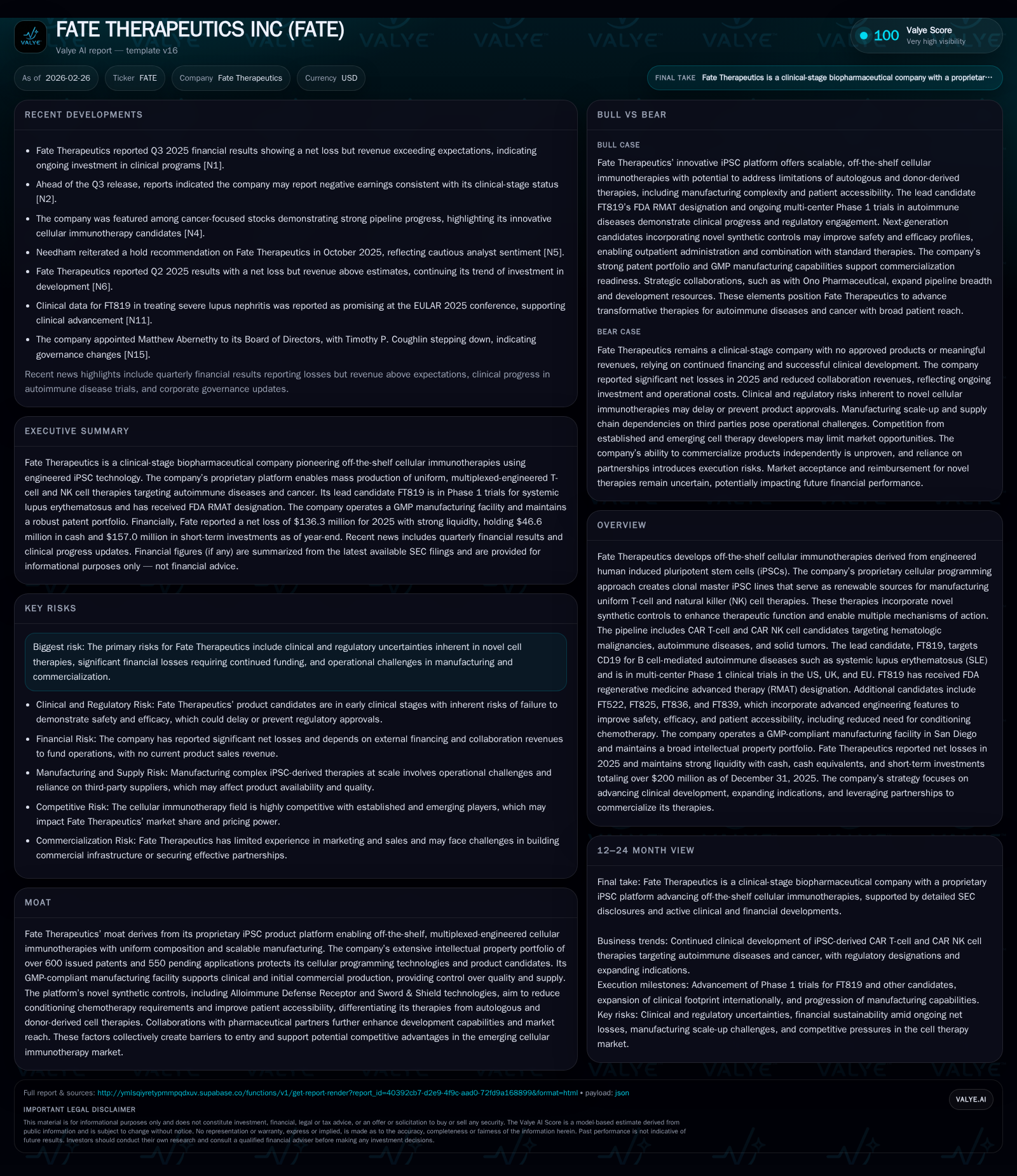

Fate Therapeutics Advances Off-the-Shelf iPSC Cell Therapies While Managing Clinical and Financial Challenges

Fate Therapeutics leverages proprietary iPSC technology to produce uniform, scalable cellular immunotherapies but continues to face clinical development uncertainty and sustained operating losses.

Fate Therapeutics has pioneered an off-the-shelf cellular programming platform based on engineered human induced pluripotent stem cells (iPSCs), enabling scalable production of uniform CAR T-cell and NK cell therapies targeting diverse indications including hematologic malignancies, autoimmune diseases, and solid tumors. Despite a robust intellectual property base and ongoing multi-center Phase 1 trials for lead programs like FT819, the company remains in the clinical-stage with no product revenues, sustaining large net losses annually. Cash reserves sufficed for at least a year post-2025 year-end, but ongoing R&D and manufacturing scale-up costs, combined with regulatory and litigation risks, underpin operational challenges that will shape near-term prospects.

Company Overview and Technology Platform

Fate Therapeutics is a clinical-stage biopharmaceutical company headquartered in San Diego, pioneering an innovative approach termed "cellular programming." This involves engineering human induced pluripotent stem cells (iPSCs) to incorporate synthetic controls of cell function. These engineered iPSCs serve as renewable clonal master lines, enabling the company's ability to mass-produce uniform off-the-shelf T-cell and natural killer (NK) cell therapies. Analogous to master cell lines used in monoclonal antibody manufacturing, Fate’s platform aims to address logistical complexities of autologous cell therapies by delivering consistent product batches with scalable manufacturing capabilities [S1].

The cells produced can be multiplexed-engineered for multiple therapeutic mechanisms of action and programmed for on-demand availability. The pipeline covers hematologic malignancies, autoimmune disorders including systemic lupus erythematosus (SLE), idiopathic inflammatory myositis, systemic sclerosis, myasthenia gravis, and solid tumors through collaboration arrangements [S1]. For example, the lead candidate FT819 targets CD19 expressing B cells relevant for autoimmune disease indications; it is designated under FDA’s RMAT program and is being evaluated in Phase 1 clinical trials across multiple regions including the US, UK, and EU [N/A]. Further candidates involve CAR NK therapies developed for cancer indications [S1].

Historical Financial Performance

Despite scientific progress, Fate Therapeutics has not commercialized products yet. Revenues remain largely derived from research collaborations and government grants rather than product sales. Notably, top-line figures have shown stability rather than growth over the last available historical window with revenue around $1 million noted as of 2017 [F1]. Losses have been extensive due to heavy investment in R&D and manufacturing scale-up.

The table below summarizes key financial metrics for recent years:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -136 | -106 | -148 | 6 | +26.8% |

| 2024 | -186 | -123 | -210 | 1 | -15.7% |

| 2023 | -161 | -132 | -191 | 6 | +42.9% |

| 2022 | -282 | -248 | -308 | 36 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -112 | -65.8 |

| 2024 | -124 | -58.4 |

| 2023 | -138 | -43.7 |

| 2022 | -284 | -58.2 |

Source: SEC companyfacts cache [F1].

(FY = Fiscal Year; Rev = Revenue; OpInc = Operating Income; Net = Net Income; CFO = Cash Flow From Operations; Capex = Capital Expenditures; Equity = Shareholders' Equity); revenues reported only through FY2017 at approx. $1M [F1].

Operating losses shrank meaningfully between 2024 and 2025 (approximate improvement of ~30%), coinciding with corporate restructuring aimed at cost control [S7]. However, cash flow from operations remains strongly negative reflecting ongoing investment in clinical programs and manufacturing infrastructure.

Growth Drivers

Fate’s future growth potential is closely tied to progressing its iPSC-derived cell therapy candidates through clinical milestones toward regulatory approvals. Its multiplexed off-the-shelf platform seeks to overcome limitations of patient-specific autologous products by enhancing scalability while maintaining safety via synthetic cellular controls such as Alloimmune Defense Receptor constructs.

The progression of FT819 into later stage clinical development with successful trial outcomes would be a considerable catalyst given its RMAT designation—designed specifically for serious conditions lacking adequate treatment options [N#]. Expanding geographic enrollment also widens regulatory visibility.

Collaborations such as the partnership with Ono Pharmaceuticals further diversify fate's pipeline into solid tumor indications beyond hematological uses [S1]. Additionally, proprietary intellectual property—totaling over 600 issued patents—and GMP-compliant manufacturing facilities provide barriers against competition while enabling controlled supply scalability [S1].

Capitalizing on relatively novel applications of CAR NK cells may unlock new therapeutic modalities if safety/efficacy profiles materialize favorably.

Constraints on Growth

However, significant factors could cap growth prospects:

- Clinical trial outcomes remain uncertain given pioneering nature of these therapies.

- Regulatory landscape for genetically engineered cell products involves complex requirements that may delay approvals or require costly post-market studies.

- Manufacturing complexity associated with scaling iPSC-based products demands continual process optimization.

- Dependence on external funding remains critical since the company lacks meaningful commercial revenues [S1].

- Litigation concerning prior collaborations (notably the Janssen Agreement) imposes legal risk that may divert company resources despite motions to dismiss currently pending [S8][S26].

- Pricing pressures from evolving healthcare reimbursement policies present commercialization challenges especially within U.S. payor frameworks [S19][S12].

Financial Outlook & Expectations

While explicit forward guidance remains unavailable from disclosed documents [N#], operational expenditures will likely continue substantially due to ongoing clinical trials plus maintenance of internal manufacturing capabilities.

The company expects to incur sustained losses “for at least the foreseeable future” during advancement of its product candidates through regulatory approval pathways [S1]. Investors should monitor clinical data readouts for FT819 and other pipeline products as key near-term value inflection points. Progress in strategic partnerships or licensing may also influence developmental trajectory.

Capital Structure & Liquidity Position

As of December 31, 2025 Fate had approximately $46.6 million in cash & cash equivalents plus restricted cash totaling about $10.2 million—forming a total liquid position near $57 million [F1][S18]. Marketable debt securities investments were also disclosed supporting short term liquidity buffers [S14]. The company implemented a restructuring during mid-2025 which included workforce reduction measures aimed at cost savings extending operational runway without immediate financing needs [S7].

Total equity stands at roughly $207 million declining from prior years mainly due to accumulated deficits from net losses [F1]. No dividend payments or share repurchase programs were noted.

Returns & Capital Allocation

Reflecting typical early-stage biopharma dynamics without approved product sales yet, the firm’s return on equity is profoundly negative (approximate ROE: -66%) given sustained net losses totaling over $136 million for fiscal year ended December 31st, 2025 relative to equity base [F1]. Free cash flow continues negative after capital expenditure investment mainly directed toward manufacturing scale-up.

Capital allocation presently prioritizes R&D efforts (~$24 million spent on clinical programs alone in 2025), intellectual property protection activities alongside maintaining regulated production infrastructure under GMP conditions [S11][S13].

Industry Context & Competitive Positioning

Within cellular immunotherapy space generally dominated by autologous CAR-T products requiring individualized manufacturing cycles—companies like Fate developing allogeneic off-the-shelf platforms aim for disruptive scalability advantages. Utilizing iPSC-derived lines offers potential batch consistency absent variability intrinsic to patient-sourced cells. Competitors working with primary donor cells or gene editing methods may still face supply chain constraints or immune compatibility challenges that Fate’s proprietary clonal lines look to mitigate via synthetic controls like Sword & Shield technology. Nonetheless, the field is marked by high regulatory scrutiny plus rapidly evolving science requiring continuous innovation. Strategic alliances represent critical pathways for commercialization acceleration – Fate’s collaborations signal recognition of platform value though successful commercialization milestones remain a prerequisite.

Risks Summary

Key risks identified include:

- Clinical trial failures or delays could stall pipeline advancement significantly.

- Regulatory setbacks could impose additional cost burdens or restrict product labeling/indications.

- Persistent operating losses require continued capital raises exposing dilution potential.

- Manufacturing challenges scaling sophisticated iPSC-derived therapies safely add operational risk layers.

- Ongoing lawsuits related to prior disclosure practices pose financial/legal uncertainties.

- Healthcare policy dynamics affecting drug pricing/reimbursement may impact revenue potential after commercialization.

The company actively manages these risks but their inherent nature underscores investor caution regarding timeline predictability and capital intensity inherent in next-generation cell therapy development.[S4][S8][S15][S16]

This analysis consolidates currently available regulatory filings and company disclosures without issuing investment recommendations. Readers should consider updated public filings for further insight into Fate Therapeutics’ evolving business prospects.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments