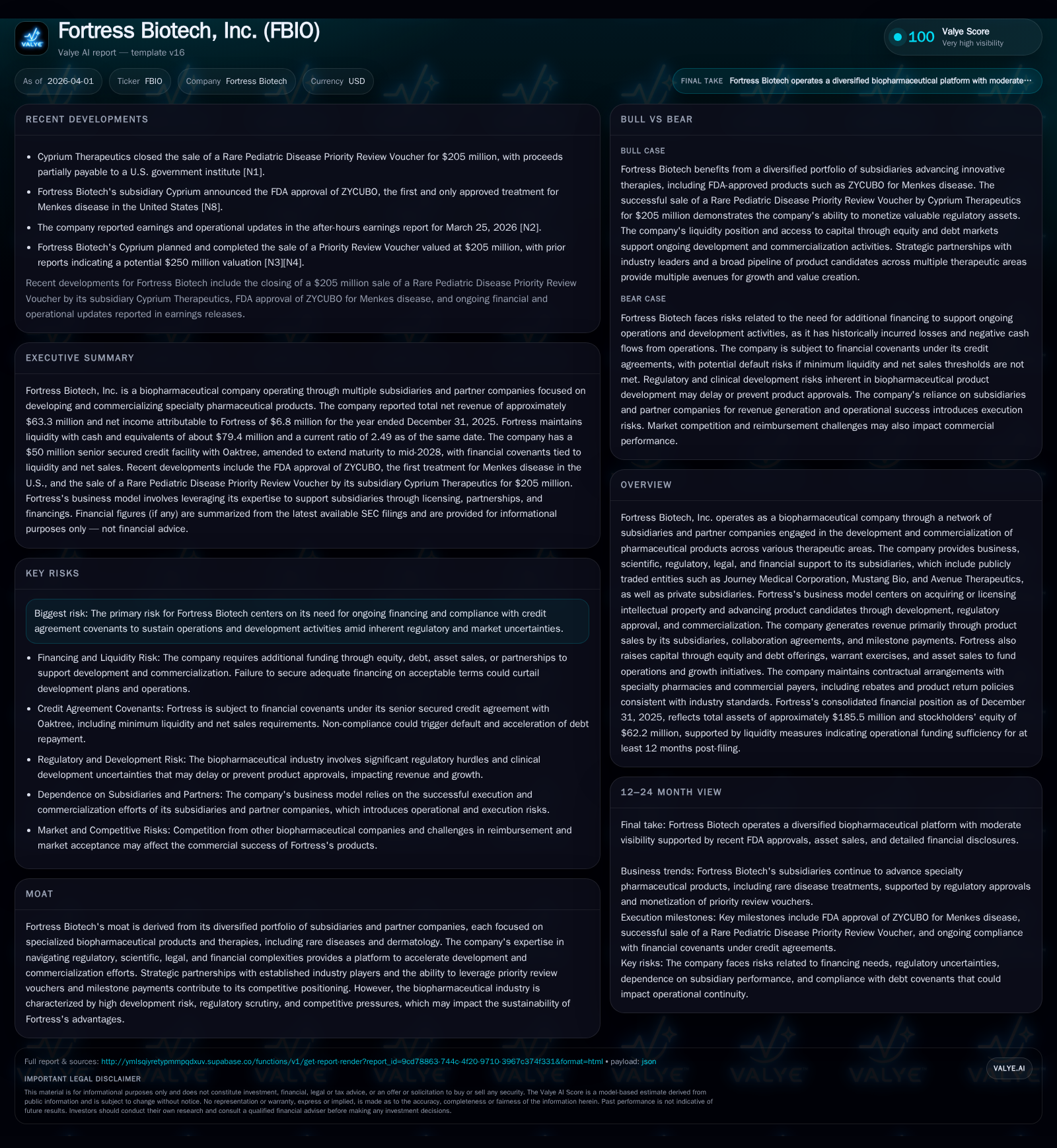

Fortress Biotech Leverages Diversified Subsidiaries Amid Financial and Regulatory Headwinds

Fortress Biotech maintains growth through strategic asset sales and subsidiary expansion while managing significant operating losses and debt covenants.

Fortress Biotech operates a network of subsidiaries focusing on specialized pharmaceutical products, generating revenue through product sales, collaborations, and milestone payments. In 2025, revenue increased 9.7% to $63.3 million, while operating losses narrowed but remained substantial at $70.2 million. Net income turned positive to $6.8 million, driven largely by non-operating gains including the monetization of assets. The sale of a $205 million priority review voucher (PRV) by its subsidiary Cyprium marked a key liquidity event affecting debt covenant relief under an amended loan facility. Fortress’s growth outlook depends on advancing clinical candidates within its portfolio and sustaining capital access amid stringent loan covenants and regulatory risks.

Company Overview and Business Model

Fortress Biotech operates as a holding company supporting a network of subsidiaries that focus on diverse therapeutic areas including dermatology, rare diseases, gene therapies, and neurology. The parent company provides business infrastructure and capital support while subsidiaries independently develop and commercialize pharmaceutical assets. Fortress employs a strategy of acquiring or licensing intellectual property rights with development funded through equity or debt financing alongside milestone payments tied to regulatory progress [S1][N1].

Historical Financial Performance

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 63 | 7 | -66 | -70 | +9.7% | +114.8% |

| 2024 | 58 | -46 | -80 | -110 | -31.8% | +24.1% |

| 2023 | 85 | -61 | -128 | -142 | +11.6% | +30.0% |

| 2022 | 76 | -87 | -179 | -204 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 664000 | 13.7 | |

| 2024 | 694000 | -80 | -202.3 |

| 2023 | 736000 | -128 | -269.0 |

| 2022 | 749000 | -182 | -207.5 |

Source: SEC companyfacts cache [F1].

Revenue increased by approximately 9.7% in FY2025 compared to FY2024, driven by growth in subsidiary product sales and milestone payments particularly from Journey Medical's dermatology portfolio [F1]. Operating losses improved by roughly one-third year-over-year but remain substantial reflecting ongoing investment in pipeline development [F1]. Net income turned positive in FY2025 primarily due to non-operating gains including proceeds from monetizing assets such as priority review vouchers (PRVs) [F1][N3].

Operating cash flow remains negative consistent with heavy R&D spending but improved about 18% versus the prior year [F1]. Dividend payments on preferred stock were suspended mid-2024 as part of cash conservation efforts [S1].

Capital Structure and Key Financial Developments

A major liquidity event occurred early in 2026 when Cyprium Therapeutics, a Fortress subsidiary, sold a rare pediatric disease Priority Review Voucher for gross proceeds of $205 million [N2][N3]. Approximately 20% of these proceeds are payable to the NIH institute [S14]. This transaction significantly enhanced Fortress’s financial flexibility.

Fortress has refinanced its debt with Oaktree Fund Administration under an amended "New Oaktree Agreement" for a $35 million loan facility maturing June 30, 2028 [S8][S9]. Key terms include:

- A roughly 41-month interest-only period at an effective rate near 11.6% as of December 31, 2025.

- Quarterly interest payments with staged principal repayments beginning in late 2027.

- Collateralization of substantially all company assets.

- Financial covenants requiring minimum liquidity levels starting at $7 million, reduced to $2 million post-PRV monetization.

- Progressive minimum net sales tests based on Journey Medical's consolidated sales.

- Annual capital raise targets through equity or monetization events totaling at least $20 million before maturity.

- Maintenance of minimum ownership stakes in public subsidiaries.

Following the Cyprium PRV sale and reductions in outstanding loan balances below $10–$15 million thresholds, several covenants including net sales tests and capital raise requirements are suspended or relaxed easing near-term pressures [S13][S16].

Journey Medical also maintains a separate credit agreement with SWK Credit Agreement extended into mid-2028 with principal repayments linked to revenue milestones [S14]. Total consolidated liabilities were approximately $123 million with long-term notes payable exceeding $52 million as of year-end [F1][S17].

Operational Highlights and Pipeline Prospects

The company's diversified portfolio approach mitigates risks inherent in single-product biotech firms by supporting multiple specialty biopharma companies focused on rare conditions, dermatology treatments, gene therapies, etc., enabling shared services and strategic capital allocation [S16].

Recent developments include Avenue Therapeutics securing an exclusive license from Duke University for ATX-04 targeting lysosomal storage diseases leveraging existing safety data — signaling late-stage pipeline expansion [N1][S25]. Other subsidiaries continue active clinical programs requiring sustained capital investment expected to generate future milestone revenues.

Regulatory approval outcomes across subsidiaries remain key catalysts for revenue generation given Fortress's dependence on milestone-based cash flows.

Risks and Challenges

The company's primary risk remains its dependence on continuous capital raises due to cumulative operating losses exceeding hundreds of millions since inception [F1], necessitating ongoing financings coupled with asset monetizations to maintain operations [S20]. Failure to meet loan covenant requirements could trigger defaults subject to cure periods but pose operational disruption risks.

High failure rates typical of biopharmaceutical development combined with regulatory uncertainties add volatility to revenue forecasts [S7]. Legal contingencies related to prior divestitures impose potential indemnification costs though recent settlements have limited direct impact on Fortress’s finances [S7][S28].

Dividend suspension on preferred shares reflects conservative cash management limiting shareholder returns presently [S1].

Returns and Capital Allocation Summary

Based on FY2025 results, Fortress’s approximate return on equity stands near 13.7%, influenced by one-time gains amid persistent operational losses [F1]. Negative operating cash flow primarily reflects continued R&D investment focused on clinical development rather than fixed asset expansion — capex was minimal in recent years [F1][S22].

Share repurchases have been negligible historically reflecting preservation strategies typical for development-stage biotechs [F1]. Dividend payouts ceased for preferred stock partly due to eligibility constraints impacting streamlined SEC registration filings [S1].

Capital allocation prioritizes funding clinical progressions mainly through external equity raises at both parent and subsidiary levels alongside strategic monetizations such as PRV sales [N3][S20].

Forward-Looking Considerations

While no explicit forward guidance has been issued post-FY25 reporting cycle [N1], investors should monitor:

- Clinical trial readouts across subsidiaries that could unlock milestone revenues.

- Achievement of Journey Medical’s net sales milestones critical for debt covenant compliance.

- Progression of strategic partnerships or licensing deals similar to Avenue’s Duke collaboration.

- Deployment plans for proceeds from the Cyprium PRV sale affecting debt reduction or new investments.

- Timing of regulatory filings that could accelerate commercial launches.

- Restoration of S-3 shelf eligibility contingent upon accrued dividend settlements enabling future equity offerings [S1].

The balance between positive pipeline developments unlocking milestone revenues versus ongoing capital needs amid stringent credit conditions will shape Fortress’s growth trajectory beyond near-term liquidity events.

This report is prepared solely for informational purposes without investment recommendation or advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments