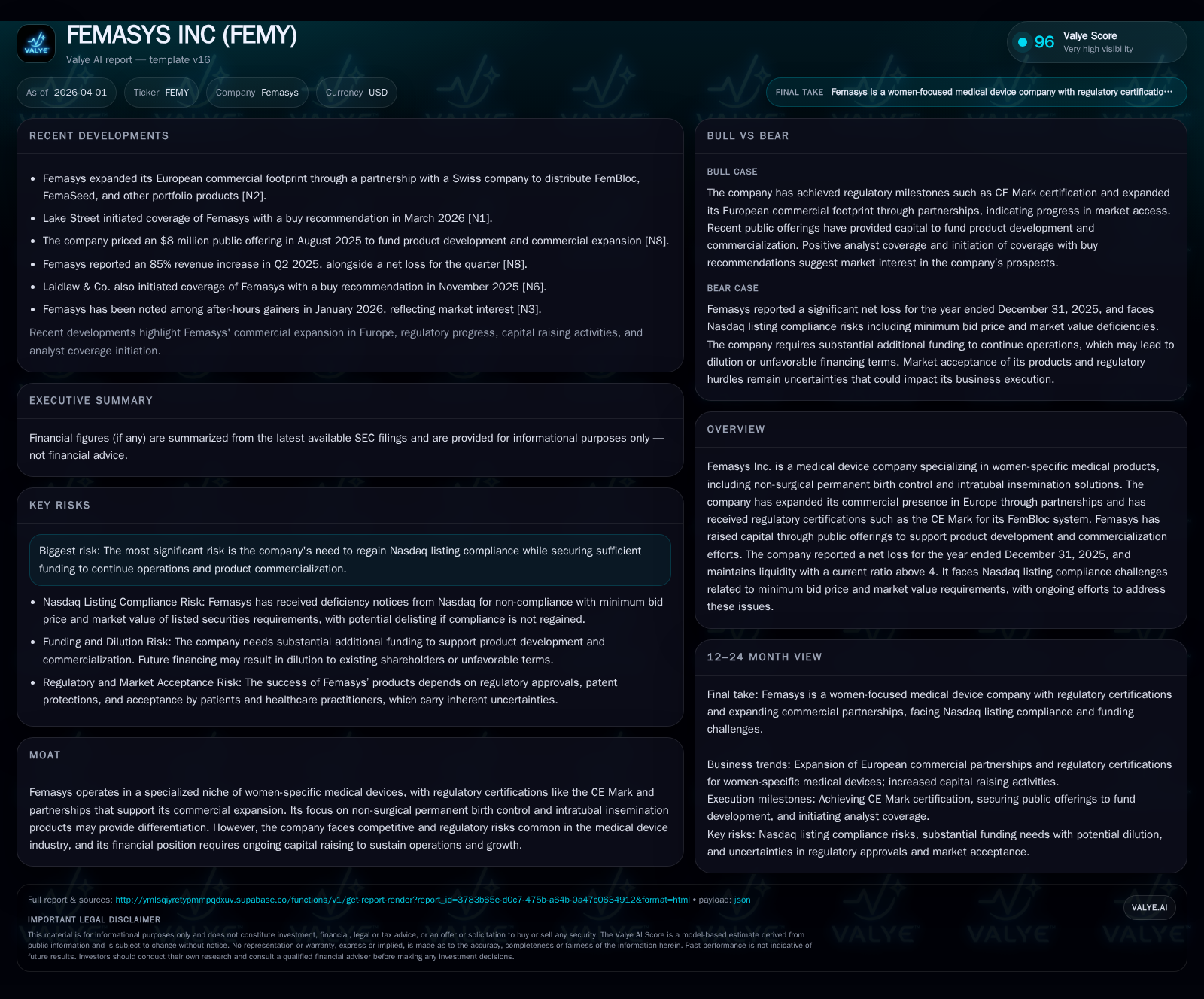

Femasys Inc Advances Women’s Health Devices Amid Financial and Regulatory Challenges

Femasys balances innovative product development in women’s health with persistent net losses and Nasdaq compliance risks.

Femasys Inc focuses on women-specific medical devices such as non-surgical permanent birth control and intratubal insemination. Despite regulatory progress including CE Mark certifications and AMA CPT code approvals, the company continues to report significant operating losses and faces Nasdaq listing compliance challenges. Capital raises remain essential to fund pivotal FDA trials and commercial expansion, particularly in Europe through partnerships. Key risks include financial sustainability amid competitive and regulatory pressures, underscoring a complex path to profitability.

Financial Performance: Sustained Losses Despite Revenue Growth Initiatives

Femasys Inc has operated at a loss as it invests heavily in women-specific medical devices. The fiscal year ending December 31, 2025 concluded with an operating loss of approximately -$17.6 million and a net loss near -$18.6 million [F1]. These reflect marginal improvements compared to the prior year's operating loss of -$17.8 million and net loss of -$18.8 million [F1].

Operating cash flow was deeply negative at about -$18.7 million in FY2025, slightly improved from -$19.4 million in FY2024 [F1]. Capital expenditures declined from roughly $762k to $525k [F1], indicating adjustments in development spending.

This ongoing unprofitability underscores Femasys' capital-intensive growth phase typical of medtech innovators addressing niche unmet needs.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -19 | -19 | -18 | 525007 | +1.0% |

| 2024 | -19 | -19 | -18 | 761706 | -32.1% |

| 2023 | -14 | -11 | -15 | 143917 | -25.0% |

| 2022 | -11 | -11 | -12 | 407475 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -19 | -317.4 | |

| 2024 | 60753 | -20 | -816.5 |

| 2023 | 229953 | -11 | -77.6 |

| 2022 | -11 | -74.8 |

Source: SEC companyfacts cache [F1].

Table notes: Consistent operating losses with slight year-over-year improvements; highly negative cash flows reflect ongoing investments.

Product Development and Regulatory Milestones in 2025

Key offerings include FemBloc®, a non-surgical permanent birth control system delivering synthetic tissue adhesive into fallopian tubes; and FemaSeed®, an intratubal insemination (ITI) device facilitating infertility treatment.

FemBloc secured CE Mark certification under the EU Medical Device Regulation in early-mid 2025 — the first global regulatory approval for such a non-surgical female sterilization device [S1].

Additionally,FemaSeed received approval from the American Medical Association's CPT Editorial Panel for a Category III CPT code [N2], facilitating reimbursement pathways critical for U.S. clinical adoption.

Peer-reviewed data support FemBloc's effectiveness and five-year safety profile [S1], positioning it as a safer alternative to surgical sterilization methods. Similarly,FemaSeed's clinical trials demonstrate positive patient and practitioner satisfaction [S1].

These milestones reflect focused R&D efforts advancing proprietary technologies within women's health.

Capital Structure and Nasdaq Compliance Challenges

As of December 31, 2025,Femasys reported current assets of approximately $16.5 million against current liabilities near $3.6 million yielding a current ratio around 4.53 [F1]. Cash and cash equivalents were about $9.3 million [F1], indicating solid short-term liquidity.

However,the company carries an accumulated deficit exceeding $145 million reflecting sustained historical losses [S1]. Financing has primarily come from public offerings including ATM equity sales private placements convertible preferred stock,and convertible notes issuance [S1].

Nasdaq has issued notices citing non-compliance due to sub-$1 minimum bid price persisting over extended periods and market capitalization below required thresholds [S2]. An initial cure period expired January 12th 2026 with Nasdaq granting an extension through July 13th 2026 contingent on measures such as potential reverse stock splits to restore compliance [S6][S18].

Pro forma equity after late-2025 financings improved to about $5.2 million surpassing the required minimum for continued listing [S2]. Nevertheless,the risk remains until sustained compliance is demonstrated.

Current cash forecasts estimate operational runway into late 2026 absent unforeseen expenses or revenue shortfalls [S1][S6][S4]. Additional capital raises will be necessary to complete pivotal FDA trials particularly the PMA filing for FemBloc [S1].

Commercial Strategy: Expanding European Market Presence

Femasys leverages strategic partnerships in Europe to commercialize FemBloc's minimally invasive benefits against traditional surgical sterilization approaches [S1]. These collaborations provide local marketing infrastructure and sales channels critical across diverse healthcare reimbursement systems.

The company also markets complementary diagnostics like FemVue ultrasound devices enhancing patient assessment capabilities alongside fertility treatments.

Clinical Pipeline Outlook: FemBloc Pivotal Trial Progression

The key pipeline milestone is the pivotal FINALE trial evaluating FemBloc's safety and contraceptive efficacy necessary for FDA PMA submission [S1][N1]. Patient enrollment pace presents execution risk given clinical study competition.

FDA advisory feedback timing adds uncertainty affecting approval timelines beyond established European CE-marked markets.

Successful trial completion combined with robust regulatory submissions remains essential for U.S.market entry.

Capital Allocation: No Dividends; Limited Share Repurchases Amid Fundraising Needs

Consistent with its developmental stage,Femasys does not pay dividends allocating capital towards R&D and commercialization efforts [F1]. Share repurchases have been minimal — around $60k in recent years — reflecting limited capacity amid recurring equity raises [F1][S7][S18][S24].

Notably,the November 2025 financing proceeds were mainly used to retire legacy convertible notes improving financial flexibility but highlighting reliance on external funding sources [S4].

Further fundraising will likely be required before achieving sustainable profitability.[S1][S6]

Risks and Opportunities Summary

Risks:

- Continued operating losses require capital raises risking shareholder dilution[S1]

- Nasdaq listing compliance challenges could impact market access[S2]

- Regulatory or clinical trial delays may affect approval timelines[S1]

- Potential intellectual property disputes exist though no material litigation currently reported[S1]

- Competition from established surgical sterilization methods necessitates strong clinical evidence[S1]

Opportunities:

- First-in-class CE-marked non-surgical permanent birth control platform[S1]

- Growing infertility treatment portfolio including validated ITI technology[S1][N2]

- Expanding European presence through partnerships[S1]

- FDA pivotal trial outcomes could unlock broader U.S.market access[N1]

- Complementary diagnostic offerings foster integrated care solutions[S23]

Disclaimer:

This report is based on publicly available data through March-April 2026 filings and news releases. It is not investment advice regarding FEMASYS INC or its securities.

Comments