FIGS Inc. Advances Healthcare Apparel Innovation with Robust Profitability Amid Growth and Operational Scaling Challenges

Founder-led FIGS leverages technical fabric innovation, digital community engagement, and an integrated merchandising model to disrupt a traditional healthcare apparel market.

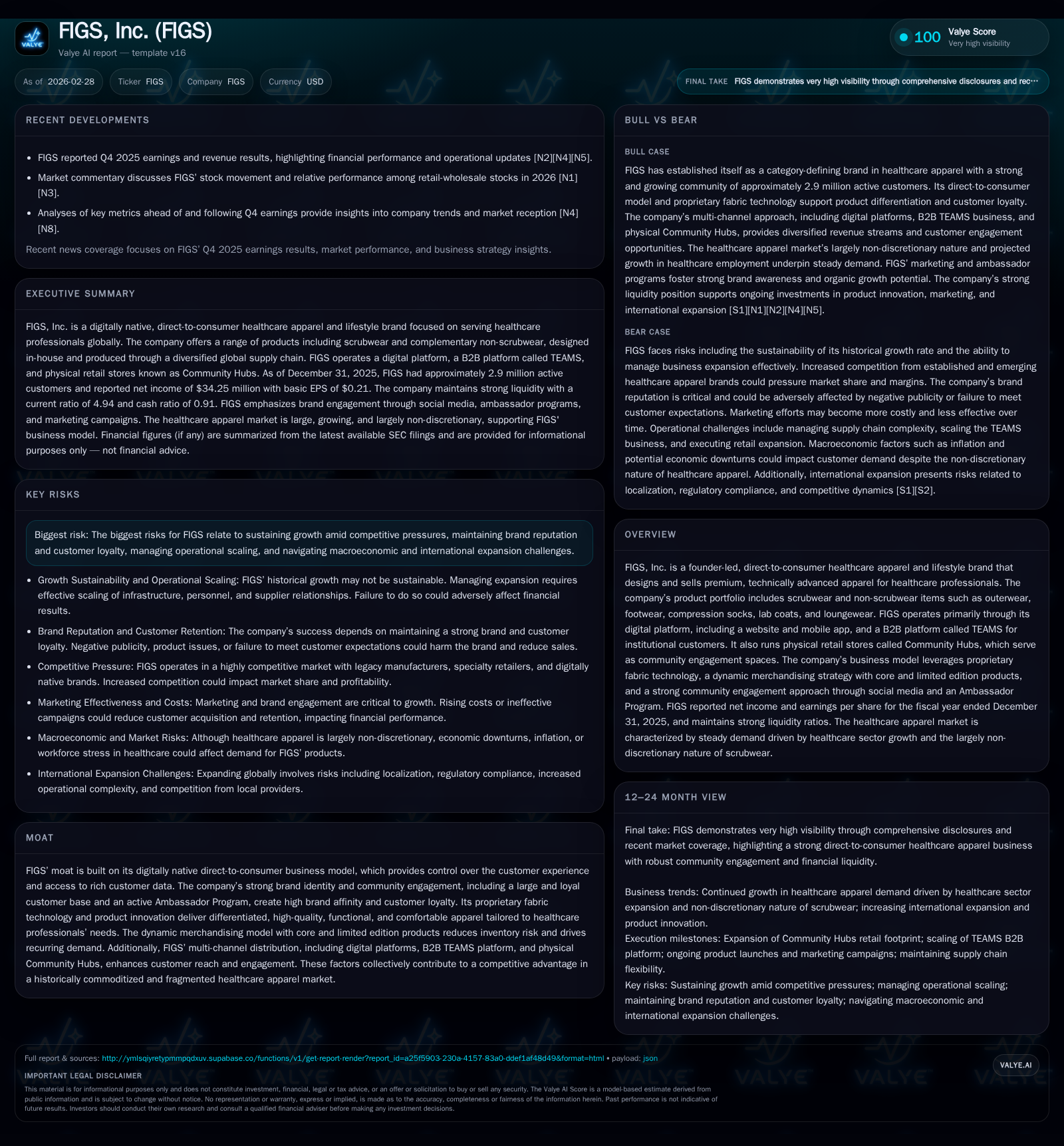

FIGS, Inc. has established itself as a digitally native, direct-to-consumer leader in premium healthcare apparel with nearly 2.9 million active customers as of end-2025. The company’s historical growth was driven by product innovation, brand loyalty, and community engagement through its digital platform and unique B2B TEAMS channel. In fiscal 2025, FIGS delivered a substantial profit rebound with $38.1 million operating income and $34.3 million net income on strong revenue growth, supported by effective inventory management and expanding physical retail hubs. Going forward, FIGS aims to sustain growth via international expansion, new product launches, and TEAMS adoption but faces risks including intensifying competition, scaling operational infrastructure, and supply chain complexity.

Company Overview

FIGS, Inc., founded and led by co-founders Heather Hasson (Executive Chairman) and Trina Spear (CEO), is a pioneering healthcare apparel and lifestyle brand focused on serving medical professionals globally through a direct-to-consumer (DTC) business model [S1][S4][S6][S9]. The company has redefined scrubs—previously commoditized products—through innovative design emphasizing comfort, durability, function, style, and affordability under its proprietary FIONx fabric technology featuring four-way stretch, anti-odor, anti-wrinkle, and moisture-wicking properties [S17]. Beyond scrubwear—which includes 17 core styles in ten colors accounting for over 60% of net revenues—FIGS offers a layered apparel system incorporating non-scrubwear such as outerwear, footwear (developed in partnership with New Balance), compression socks, lab coats, underscrubs, and loungewear [S6][S21].

Historical Performance

FIGS’ financial trajectory reflects the challenges of scaling an innovative brand within an entrenched industry disrupted through digital native methods. Revenue figures from companyfacts show a progression from earlier years culminating in reported revenues at least through calendar year-end 2021 [$419.6M], while explicit recent revenue benchmarks are not provided in submissions [F1]. Nonetheless, the company’s profitability improved markedly in the fiscal year ending December 31, 2025: operating income soared to approximately $38.1 million from just $2.3 million the prior year—a more than fifteenfold increase—and net income rose to about $34.3 million from $2.7 million in FY2024 [F1].

Operating cash flow manifested strength at $61.2 million despite a decline from prior-year levels ($81.2 million), reflecting investments in growth initiatives balanced against improving earnings quality [F1]. Concurrently, capital expenditures halved year over year to roughly $8.2 million owing partly to strategic moderation after prior expansion endeavors [F1]. FIGS maintains a strong liquidity position with cash & equivalents exceeding $81 million at year-end 2025 alongside a current ratio near five times—signaling robust short-term financial flexibility [F1]. Equity increased to approximately $437.5 million reflecting reinvested earnings and balance sheet accretion.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 34 | 61 | 38 | 8 | +1159.2% |

| 2024 | 3 | 81 | 2 | 17 | -88.0% |

| 2023 | 23 | 101 | 34 | 16 | +6.8% |

| 2022 | 21 | -35 | 38 | 5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 3 | 53 | 7.8 |

| 2024 | 45 | 64 | 0.7 |

| 2023 | 85 | 6.0 | |

| 2022 | -41 | 6.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures beyond FY2021 are not explicitly disclosed.

Business Model Drivers

FIGS’ moat stems from its digitally native DTC strategy that governs customer experience end-to-end via website and mobile apps, supported by proprietary data analytics optimizing assortment planning and replenishment [S9][S17]. The company’s multi-channel distribution further includes the B2B TEAMS platform that streamlines institutional uniform procurement—a fragmented segment historically underserved—and physical Community Hubs that create immersive brand spaces fostering loyalty and peer interaction among healthcare professionals [S6][S7].

Dynamic merchandising balances steady core scrub offerings with limited edition colors/styles launched based on consumer feedback—a model reducing inventory risk while stimulating repeat visits [S11]. This approach helped achieve an industry-leading return rate near 10%, significantly beneath typical online apparel returns of up to four times that rate [S11].

Community engagement remains pivotal: nearly three million active customers form a passionate cohort primarily composed of nurses but inclusive of diverse allied health roles worldwide [S13], energized through social media storytelling campaigns and extensive Ambassador Programs embedding FIGS deeply within hospital cultures.

Growth Prospects

Looking ahead, FIGS targets sustained expansion fueled by several vectors:

- Global Market Penetration: Continued international rollout supported by localized website experiences and regionalized marketing campaigns aims to capitalize on worldwide healthcare workforce growth [S6][N1].

- Product Innovation: Building upon core fabric technology to introduce new functional apparel categories designed for medical professionals’ shifting preferences both on- and off-shift enhances wallet share per customer [S21].

- TEAMS Platform Expansion: Increasing institutional adoption promises higher-volume contracts although success depends on navigating traditionally slow institutional purchase cycles [S6].

- Physical Footprint Growth: Opening more Community Hubs could strengthen brand connection though requires upfront investment with variable ROI profiles [S7].

However, growth is not without constraints:

- Rising competition from legacy uniform suppliers adapting digital strategies might dilute pricing power.

- Macroeconomic pressures impacting healthcare employment or discretionary spend may suppress demand.

- Operational scaling challenges include talent acquisition competition concentrated near headquarters (Southern California) and logistics hubs (Goodyear AZ), which may impact fulfillment speed or costs [S1][S2].

Forecasts & Milestones

No explicit company guidance was found for upcoming fiscal periods; however, key indicators to monitor are metrics related to:

- Active customer count trajectory especially outside North America.

- TEAMS platform penetration rates within institutions.

- Average order values across scrubwear vs non-scrubwear categories.

- Gross margin trends impacted by supply chain costs or currency fluctuations. Analysts closely watching quarterly updates should note these variables as signals of operational effectiveness post recent expansions [N1][N3].

Capital Allocation & Returns

The company's capital return activity remains modest relative to cash flows generated: FY2025 saw buybacks totaling roughly $2.7 million compared to a robust free cash flow estimated at approximately $53 million after capital spending [F1]. There are no dividend payouts currently disclosed.

ROE was moderate at about 7.8% in FY2025 reflecting net income against reported shareholder equity levels—commendable for a growth-stage apparel business investing heavily in product innovation and physical footprint builds yet below mature consumer staples benchmarks where double-digit ROEs prevail [F1].

FIGS’ operational cash flow generation underscores efficient conversion of sales into liquid resources supporting ongoing investments without heavy reliance on external financing.

Industry Context & Competitive Insight

Healthcare apparel has been traditionally fragmented with low innovation due to dependence on third-party licensed manufacturers selling undifferentiated scrubs predominantly via discount medical supply stores . FIGS upended this static landscape integrating technical fabrics seen in performance wear sectors into medical uniforms—a historically overlooked niche—with direct consumer connectivity enabling tailored design cycles uncommon among incumbents.

This blend of digitally native methods merged with mission-driven branding targeting “Awesome Humans”—healthcare workers who value purpose alongside function—provides substantive psychological differentiation difficult for legacy players weighted toward B2B distributor relationships to replicate quickly . However, emerging players focusing on sustainability claims or diversified wellness apparel could encroach on some lifestyle adjunct categories demanding vigilant competitive intelligence.

Supply chain remains crucial: reliance on key fabric suppliers mainly based in China poses geopolitical risks including tariffs or labor disruptions while attempts to diversify production geographies could increase cost structures temporarily but improve overall resilience [S22].

Risks & Legal Considerations

Recent SEC filings emphasize risk themes relevant for investors parsing operational durability:

- Legal proceedings detail ongoing securities litigation dating from IPO communications around demand forecasting accuracy now largely dismissed but costly management distraction persists [S10][S24].

- Compliance with varied international regulations governing privacy (e.g., CCPA), product safety standards across multiple jurisdictions adds complexity requiring continuous expenditure on controls with potential for penalties or reputational damage if breached unexpectedly [S15][S18].

- Dependence on foreign suppliers collides with anti-bribery laws including FCPA leading to reputational vulnerability beyond traditional supply chain risks if third parties contravene statutes unintentionally or otherwise [S8][S12][S20].

- Workforce stress in healthcare impacts replenishment-driven demand unpredictably—a subtle macro factor relevant given FIGS’ reliance on consistent purchase patterns by professionals juggling demanding schedules often exacerbated during health crises or economic downturns [S22].

Conclusion

FIGS stands out as an innovator transforming healthcare apparel through technology-driven design married with digital-first consumer engagement strategies centered on community empowerment rather than pure commoditization. Its FY2025 financial results signal solid profit recovery accompanied by effective capital discipline amid ongoing expansion efforts globally.

Nonetheless, sustaining momentum will require navigating increasingly complex operational terrain marked by talent market tightness near key facilities plus international regulatory compliance burdens amid evolving geopolitical headwinds affecting supply chains. Investors tracking FIGS should focus on how effectively management executes global scalability plans without compromising product quality or brand authenticity while maintaining tight inventory controls underpinned by deep analytics capabilities intrinsic to its DTC operating model.

This report is for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments