Flagstar Bank's Strategic Transformation Revives Profitability Amid Legacy Loan Challenges

Flagstar Bank improved net losses sharply by recalibrating its loan portfolio, optimizing funding costs, and enhancing operational efficiency, while managing concentrated credit risks.

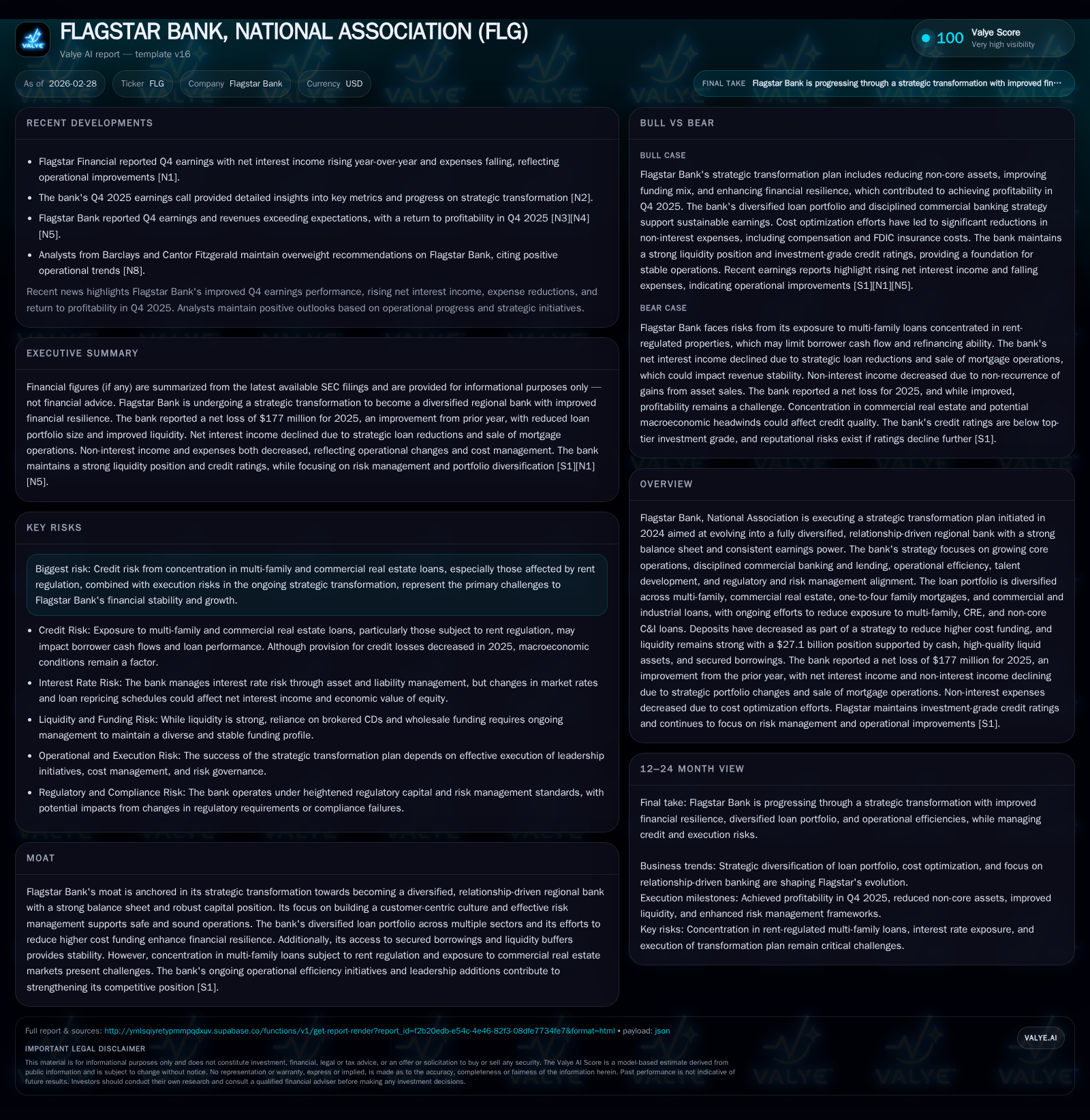

Flagstar Bank, N.A. has progressed from a net loss of $1.1 billion in 2024 to a significantly reduced net loss of $177 million in 2025 through its strategic transformation plan initiated in 2024. This plan centers on diversification away from multi-family and commercial real estate exposures, disciplined liability management including deposit base contraction and debt repricing, and operational enhancements that have lowered expenses. Despite continued credit concentration risks particularly in rent-regulated multi-family loans concentrated mostly in New York, Flagstar’s strengthened liquidity position at $27.1 billion and maintained capital ratios well above regulatory minimums underpin financial resilience. Going forward, monitoring loan quality trends in legacy portfolios and deposit growth will be critical milestones for potential earnings stabilization and sustainable growth.

From Heavy Losses to Scalability: Recent Financial Snapshots

Flagstar Bank's financial journey from a deep net loss of $1.1 billion in fiscal year 2024 to a narrower loss of $177 million in 2025 outlines a pronounced performance inflection tied directly to its ongoing strategic pivot [F1][S1]. Net income attributable to common shareholders similarly improved materially—reducing losses per share from -$3.49 to -$0.50—offering early evidence that the firm’s transformation efforts are gaining traction.

Net interest income (NII), Flagstar’s mainstay revenue component, fell from approximately $2.15 billion in 2024 to about $1.72 billion in 2025 [S1]. This decline reflected a combination of a reduced asset base—loans shrank nearly $7.5 billion—and compression in net interest margin owing to narrower spread dynamics influenced by both market rates and the asset-liability mix shift. The weighted average yield on total loans softened modestly from about 5.54% to 5.09%, while bond securities yields stabilized around mid-4% levels as reinvestment activities accelerated [S1]. Although the bank managed prudent cost containment leading to lower operating expenses driven partly by workforce adjustments post mortgage operation divestiture [N1][S27], cash flow metrics remain challenged with an operating cash flow deficit of approximately $181 million in the latest full year versus positive figures previously [F1]. Such negative operating cash flow suggests ongoing working capital requirements aligned with balance sheet restructuring.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | -177 | -181 | +84.2% |

| 2024 | -1118 | 86 | -1315.2% |

| 2023 | -79 | 263 | -112.2% |

| 2022 | 650 | 1026 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 15 | -2.2 | |

| 2024 | 53 | 0 | -13.7 |

| 2023 | 486 | 0 | -0.9 |

| 2022 | 317 | 7 | 7.4 |

Source: SEC companyfacts cache [F1].

Table Note: Revenue figures relate to earlier years ending before divestitures; recent years reflect strategic portfolio recalibration [F1].

Diversified Loan Portfolio Reshaping and Credit Risk Management

Central to Flagstar's strategy is reshaping its lending mix away from concentration hotspots notably multi-family residential properties subject to rent regulation laws—largely centered in New York State—and reducing exposure to volatile commercial real estate (CRE) segments [S1][S26][S17]. The multi-family portfolio contracted by approximately $5.9 billion during 2025 primarily via par payoffs including a significant single-borrower loan sale portion [S13][S26]. Over half the outstanding multi-family loans are fixed-rate convertible option loans which reset at repricing dates typically tied to intermediate-term market rates, impacting future cash flow predictability [S14][S25]. Approximately half of these interest-only loans will enter amortization by end-2026 heightening repayment pressure on borrowers amid inflationary cost environments.

Geographically concentrated multi-family loans remain predominantly located in NYC boroughs accounting for about two-thirds of total exposure—with Manhattan, Brooklyn, Bronx, Queens forming the core where rent laws curb landlords’ ability to increase rents upon vacancy thus restraining property cash flow upside [S26][S17]. Commercial real estate loans also shrank by roughly $2.5 billion (21%) through payoffs consistent with portfolio de-risking focus; office and industrial properties comprise significant collateral types here [S18][S23].

Credit risk monitoring includes mandated annual or more frequent appraisals of collateral securing substandard/non-accrual CRE and multifamily assets as well as detailed debt service coverage ratio (DSCR) assessments reflecting borrower capacity under forecast scenarios [S8][S16]. Charge-offs declined relative to prior years but remain elevated for the hardest-hit sub-portfolios totaling about $326 million in multi-family/CRE charge-offs during fiscal year ended December 2025 against an allowance for credit losses nearing $1 billion—indicating cautious provisioning amidst uncertain macroeconomic conditions [S10][S19].

Depository and Borrowing Strategy: Navigating Cost and Liquidity

In funding its asset base, Flagstar deliberately lowered its deposit footprint by nearly $9.9 billion or close to 13% since late-2024—a reflection of exiting higher-cost brokered certificates of deposit which fell precipitously from approximately $9.5 billion to just over $2.3 billion within one year [S12][S16]. This contraction aimed at lowering overall cost of funds pressed management to rely more on secured borrowing sources like Federal Home Loan Bank (FHLB) advances which increased short-term borrowings by about $1.25 billion but decreased long-term debt substantially through prepayments exceeding $2.5 billion during the year—efforts that cut weighted average borrowing rates from near 4.9% down toward mid-4% levels [S6][S17].

Liquidity remains a key strength amidst tightening deposit bases: Flagstar maintains an ample liquidity buffer at roughly $27.1 billion composed of cash reserves ($5.3B), high-quality liquid assets (HQLA) including agency mortgage-backed securities totaling over $13B unencumbered and available secured borrowing capacity at the Federal Reserve Discount Window ($1.8B) complemented by FHLB accessible capacity ($6.5B) ensuring flexibility under stress scenarios [S4][S5][S16]. The bank's liquidity policy incorporates robust early warning indicators overseen daily along with contingency funding plans tested against severe yet plausible stress frameworks aligned with regulator expectations [S4][S7].

Operational Efficiency Enhancements Supporting Profit Turnaround

Alongside portfolio rebalancing, operating expense containment played a pivotal role in Flagstar’s turnaround trajectory with overall general administrative expenses falling as branch rationalization efforts continued following disposal of mortgage operations completed late-2024 [N1][N2][S27]. This included recalibrations in compensation structures contributing to reduced personnel costs alongside lower FDIC insurance premiums reflecting reduced asset base size—both crucial given persistent margin pressure emanating largely from competitive deposit pricing needs and compressed net interest margins [N1][N2][S27].

Talent development initiatives also form part of enterprise transformation driving cultural shifts toward relationship banking embedding cross-sell opportunities and closer credit underwriting oversight aiming for sustained earnings stability beyond balance sheet adjustments [S1][N2].

Capital Position, Returns, and Shareholder Distributions

Flagstar’s capital ratios comfortably exceed regulatory minima after absorbing losses associated with transformation efforts. As of December end-2025, common equity tier 1 capital stood at about $7.8 billion yielding a CET1 ratio near 12.8%, well above the OCC’s threshold for “well capitalized” categorization [S14]. Risk-weighted assets reductions driven by loan portfolio shrinkage supported this robust buffer providing headroom for absorbing potential future credit shocks.

Return metrics remain negative consistent with ongoing restructuring losses although improving vs deep prior year deficits; implied ROE approximates -2.2% based on available data integrating annual losses against shareholder equity base circa $8.14B at year-end [F1]. Dividends paid were materially curtailed—to only $15 million compared with over $50 million the prior year—and no share repurchases have occurred since early stage post-pandemic buybacks ceased in late-2022 signaling prudent capital retention stance focused on balance sheet repair rather than distributions expansion [F1][S25].

Leadership Initiatives and Risk Governance in Transformation

Transformation progress owes much to newly appointed senior leadership enhancing both operational discipline and risk governance frameworks instituted since plan inception in early-2024 [S1]. The bank advanced formalized risk appetite statements articulating tolerance levels aligned tightly with budgeting, strategic planning and capital allocation processes integrating qualitative controls plus quantitative risk limits vetted regularly by board committees.

Credit risk management leverages comprehensive subportfolio reviews featuring scheduled collateral appraisals annually or more frequently for impaired assets alongside borrower financial updates facilitating refined internal ratings; liquidity stress testing protocols incorporate early warning indicators triggering contingency actions ensuring timely intervention capabilities under volatile conditions [S7][S16]. Senior risk officers maintain continuous oversight reflecting heightened supervisory expectations post previous losses facilitating adaptive credit risk practices tailored for rent-regulated loan nuances inherent within multi-family exposures.

Outlook: Milestones Ahead and Potential Growth Barriers

Looking forward into fiscal year 2026 and beyond, critical milestones flagged by management include monitoring loan repricing events where two-thirds of adjusted multi-family variable rate loans mature through repricing across next three years placing pressure on borrowers adjusting payment burdens amid rent regulations potentially constraining DSCR improvements required for sustaining standards underwriting new business [N2][S10][S17]. Deposit growth trajectory will serve as another barometer assessing success stabilizing low-cost funding sources after strategic contraction.

Risk factors loom mainly around execution risks associated with transformation pace completion alongside macroeconomic uncertainty impacting borrower demand for new lending products especially within commercial sectors targeted for expansion such as private banking-originated one-to-four family mortgages which warmed modestly (+8%) during latest fiscal period offering selective growth avenues despite core challenges remaining entrenched credit provisions tied primarily to legacy portfolios constraining earnings inflection timing [N10][N3][S26]. Staying compliant amid evolving prudential regulations without eroding capital buffers will further test institutional agility.

In sum, Flagstar Bank exemplifies measured but tangible progress from historic operating losses towards scalable profitability foundation underpinned by diversified lending repositioning backed by stable liquidity reserves reinforced through disciplined liability management alongside cautious but deliberate operational streamlining coupled with sharpened governance rigor safeguarding franchise value amidst sectoral headwinds.

Disclaimer: This analysis is provided solely for informational purposes based on publicly available data up to February 28, 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments