Spirit Aviation’s Bankruptcy Path and Operational Wind-Down: What Investors Should Know

Spirit Aviation Holdings continues its Chapter 11 restructuring with an orderly operational wind-down amid significant financial pressures.

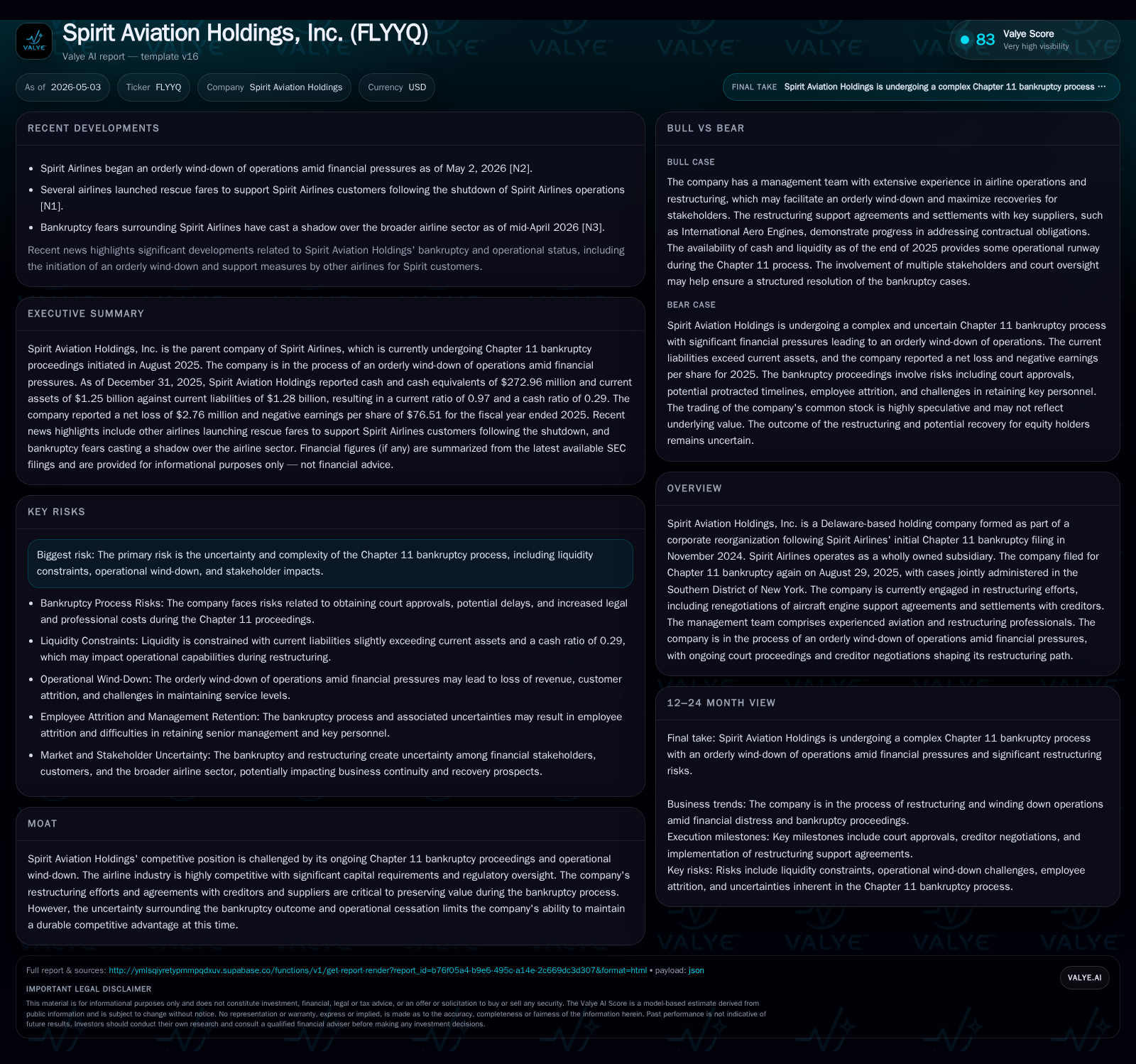

The March 2026 8-K filing for Spirit Aviation Holdings, Inc. reiterates ongoing Chapter 11 bankruptcy proceedings and highlights continuing restructuring efforts including creditor negotiations and operational wind-down. As a holding entity principally owning Spirit Airlines, the company confronts steep financial distress characterized by heavy leverage and sustained operating losses. The highly competitive low-cost carrier industry, combined with regulatory oversight and high capital intensity, constrains recovery prospects absent successful reorganization milestones. Key risks include liquidity strain, protracted bankruptcy duration, and uncertain outcomes ranging from liquidation to potential emergence.

Latest Corporate Developments and Restructuring Status

In its most recent filing on March 27, 2026 ([S3]), Spirit Aviation Holdings provided updates on its Chapter 11 bankruptcy case initiated on August 29, 2025. The filing underscores that Spirit and its subsidiaries continue as debtors-in-possession within the Southern District of New York Bankruptcy Court. These filings include monthly operating reports covering periods ending December 31, 2025, through January 31, 2026. The focus remains on dialogue with creditors, negotiations over key contracts such as aircraft engine support agreements, and the careful management of the airline's wind-down operations. This orderly cessation reflects the company’s recognition of strained finances and strategic imperative to maintain compliance with court mandates while seeking resolution.

This staging matters because it defines the near-term operational viability of Spirit Airlines as a subsidiary under Spirit Aviation Holdings. It signals that no turnaround via new growth initiatives is currently planned; rather efforts center on maximizing creditor recoveries and mitigating losses through structured reductions in operations amid ongoing financial pressures ([N2]).

Business Model Overview and Service Offering Quality

Spirit Airlines functions as a low-cost carrier within the holding company framework described in the April 2026 amended annual report ([S1]). The revenue model predominantly derives from passenger ticket sales complemented by ancillary revenue streams such as baggage fees, seat assignments, and onboard services—a standard approach among ultra-low-cost carriers. However, bankruptcy proceedings have compromised pricing power and customer confidence during this period.

The quality of service—typically value-oriented with limited frills—appeals to price-sensitive travelers but suffers from reputational damage resulting from operational disruptions linked to financial distress. The business model's reliance on high utilization of relatively homogenous aircraft fleets limits differentiation outside cost competitiveness, an advantage diminished as restructuring curtails network capacity.

As reported in the Valye analysis excerpt (), Spirit’s competitive positioning deteriorates due to bankruptcy-related uncertainties disrupting both supplier relationships (notably engine maintenance contracts) and customer retention. These factors undermine any durable economic moat amidst intense competition among U.S. low-cost carriers.

Competitive Environment and Industry Structural Challenges

Spirit operates in the fiercely contested U.S. domestic market for low-cost air travel. Competitors include better-capitalized carriers such as Southwest Airlines and Frontier Air, which enjoy stronger liquidity profiles to sustain pricing strategies during downturns. This dynamic places Spirit at a strategic disadvantage exacerbated by its current Chapter 11 status ().

Key industry structural characteristics impacting Spirit include aircraft leasing arrangements that impose fixed costs regardless of utilization levels. Engine maintenance support is another critical expense line item; ongoing renegotiations here are essential to unlocking cost relief but also pose risks if suppliers resist concessions ([S3]). Regulatory oversight by FAA and DOT imposes operational hauling capacity restrictions that limit flexibility in adjusting fleet usage during the wind-down phase.

Pricing power is impaired due to overcapacity conditions stemming from reduced flight schedules and competitor responses. Ancillary revenue streams may also contract given diminished passenger volumes and trust.

Key Growth Drivers and Potential Value Catalysts

Traditional growth drivers such as route expansion or increased seat capacity are effectively sidelined while Spirit navigates bankruptcy. Instead, growth-related upside materializes primarily through restructuring milestones: court approvals of reorganization plans; successful renegotiation of onerous contracts including aircraft leasing terms; deleveraging outcomes that reduce net debt burdens; or asset sales potentially injecting temporary liquidity ([S3], ).

The management’s demonstrated experience in complex restructurings—highlighted by CEO Eugene I. Davis’s background managing diverse distressed situations across industries ([S1])—offers some measure of discipline in preserving residual value where feasible.

Should these steps succeed without prolonged court disputes or hostile creditor actions, incremental recoveries might emerge post-bankruptcy emergence; however, no explicit timeline or quantifiable KPIs are currently disclosed.

Risks, Constraints, and Uncertainties in the Current Environment

The foremost risk remains extended bankruptcy duration compounded by liquidity pressures illustrated by a current ratio below unity (0.97) indicating current liabilities slightly exceed current assets as of year-end 2025 ([F1]). Total debt stands at approximately $1.26 billion with net debt near $986 million after accounting for cash holdings (~$273 million) ([F1]). Operating income was deeply negative (-$481 million), underscoring persistent cash burn amid reduced operations ([F1]).

These financial stresses constrain runway absent additional financing or rapid resolution via court-approved transformation plans. Employee attrition risk threatens operational continuity during this distracting period ( years).

Outcomes range from reorganization with some equity or debt stakeholder recovery to forced liquidation resulting in likely full loss for common stockholders (, [S16]). Market speculation is high as common stock trading transitions to OTC markets post-delisting ([S21]).

Upcoming Milestones and What Investors Should Monitor

Crucial near-term markers disclosed chiefly reside within bankruptcy procedural events: scheduled court hearings addressing debtor motions; deadlines for creditor consent solicitations regarding proposed amendments or plans; updates on key agreement renegotiations notably aircraft engine support contracts whose terms significantly affect cost structure ([S3]).

Market-level demand indicators such as rescue fares launched by other carriers to accommodate stranded Spirit passengers demonstrate tangible customer impact from operational shutdowns ([N1]). Watching these external market responses alongside formal court developments will help signal progress or further deterioration.

Current Financial Profile: Liquidity, Leverage, and Operating Metrics

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $273mm | |

| 2025-12-31 | ||

| Total debt | $1259mm | |

| 2025-12-31 | ||

| Net debt | $986mm | |

| 2025-12-31 | ||

| Current assets | $1246mm | |

| 2025-12-31 | ||

| Current liabilities | $1284mm | |

| 2025-12-31 | ||

| Current ratio | 0.97x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Amount (USD) |

|---|---|

| Cash & Equivalents | 272,959,000 |

| Total Debt | 1,258,700,000 |

| Net Debt | 985,741,000 |

| Current Assets | 1,245,824,000 |

| Current Liabilities | 1,283,725,000 |

| Current Ratio | 0.97 |

| Operating Income | -481,511,000 |

| Net Income | -2,760,453 |

As reflected above based on year-end December 31, 2025 data ([F1]), Spirit faces a challenging balance sheet profile dominated by significant leverage relative to modest cash reserves. Negative operating income illustrates ongoing losses consistent with wind-down activity rather than normal airline flight operations.

This analysis integrates recent event filings with contextual insights into Spirit Aviation Holdings’ strategic position amid its Chapter 11 restructuring journey. While management strives for an orderly transition leveraging its experience in distressed situations ([S1]), considerable uncertainty persists around timing and eventual recovery values for stakeholders.

Investors should therefore approach any exposure cautiously given the speculative nature of recovery prospects highlighted repeatedly across company disclosures ([S16]) and the active progression toward cessation of traditional operations ([N2]).

Disclaimer: This report is for informational purposes only within an analytical framework developed by Valye News. It does not constitute investment advice or recommendations to buy or sell securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments