Marqeta's Strategic Progress Elevates Embedded Finance Growth Trajectory

Marqeta posts sequential profitability improvement in Q1 2026, underscoring operational scale gains and enhanced embedded finance offerings.

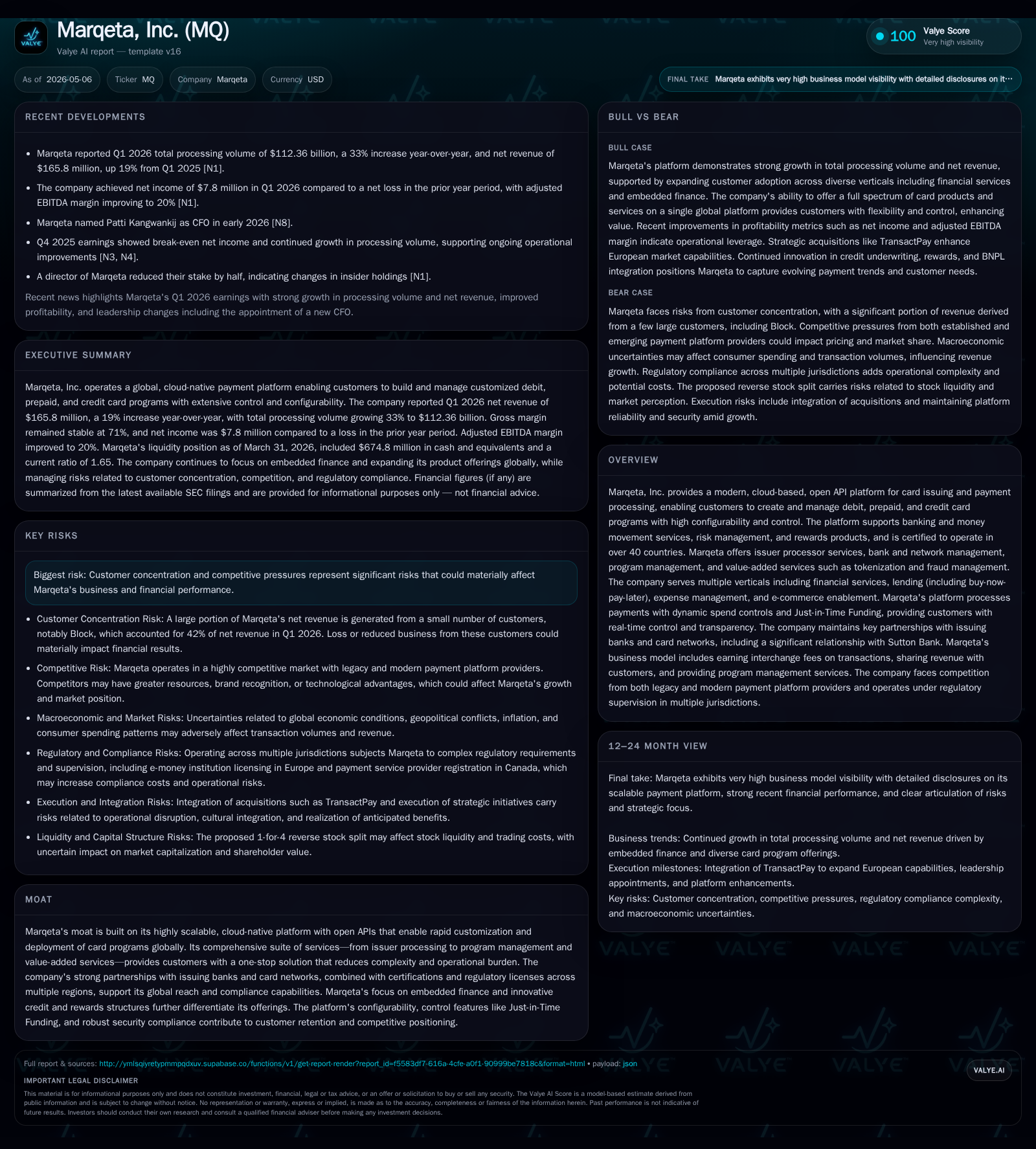

In Q1 2026, Marqeta achieved $165.8 million in net revenue alongside a positive net income of $7.8 million, marking a material turnaround from prior losses and signaling improved operational leverage. The company's cloud-native payment platform continues to capitalize on robust transaction volume growth driven by embedded finance adoption across multiple verticals including BNPL and digital banking. Strategic differentiation arises from its open API architecture, Just-in-Time Funding, and broad issuer processor services integrated with bank and network management. However, exposure to customer concentration—most notably Block—and complex network incentive accounting could constrain margin stability. Near-term watchers should focus on volume milestone incentives, customer renewal dynamics, and the outcome of an upcoming reverse stock split vote.

Latest Quarterly Operational Results: Turnaround Signs

Marqeta’s Q1 2026 performance marked a clear inflection point in its operating trajectory. Net revenue advanced to approximately $165.8 million, up nearly 19% year-over-year from $139.1 million in Q1 2025, propelled by sustained transaction volume increases on the platform [S2]. More notably, the company reported positive net income of $7.8 million compared to an $8.3 million loss a year earlier, reflecting improved operational discipline alongside stable total operating expenses around $115.5 million [S2]. Share-based compensation expense declined materially to just over $20 million from nearly $26 million in the prior year period—contributory to the margin improvement—while depreciation charges rose consistent with investments in platform infrastructure [S2].

Management highlighted that certain network incentive arrangements are contingent upon crossing cumulative annual volume thresholds which do not align perfectly with fiscal quarters; thus expense recognition is based on forecasted incentives derived from historical trends plus forward-looking event analysis [S2]. This dynamic creates some timing variability but indicates upside once volumes surpass critical breakpoints.

The combination of significant volume-driven revenue growth and disciplined expense control underpins positive adjusted EBITDA margins expanding to approximately 20%, up from 14% a year ago—a signal of scalable economics kicking in despite macroeconomic uncertainty impacting consumer spending patterns [S2][N2].

Business Model Overview: Modern Card Issuing Ecosystem

Marqeta operates as an issuer processor delivering a cloud-native, open API platform enabling clients to design sophisticated payment card programs encompassing debit, prepaid, and credit cards seamlessly integrated within their applications or websites [S1]. Customers span diverse verticals including financial services firms specializing in buy-now-pay-later (BNPL), expense management platforms, lending services, and e-commerce accelerators.

Revenue primarily derives from fees linked to Total Processing Volume (TPV)—the dollar value of transactions routed through its system net of returns—and various service fees associated with issuing bank sponsorships and network connections [S1]. Marqeta offers modular service levels ranging from core payment processing with Just-in-Time Funding (JIT) capabilities to comprehensive bank and network management where it facilitates regulatory compliance alongside card program administration such as chargebacks handling and reconciliation [S1].

This comprehensive suite reduces complexity and distribution friction for clients who prefer innovation speed without direct investment into complicated backend compliance or infrastructure layers managed by Marqeta’s platform.

Platform Differentiators and Product Quality

Marqeta’s platform differentiation lies in its flexibility and control features tailored for embedded finance scenarios where rapid deployment with granular spending rules is vital [S1]. JIT Funding enables real-time authorization with dynamic disbursement control minimizing float capital requirements while optimizing fraud risk exposure—a feature critical for fintechs offering instant credit or rewards linked transactions.

Tokenization combined with real-time decisioning engines embedded in the platform bolsters security postures across multiple certified jurisdictions (over 40 countries), facilitating global scalability while maintaining compliance integrity [S1]. The synergy between issuer processor services, bank partner integration as BIN sponsors, card network rule enforcement, and program management consolidates multiple fragmented value chain activities into one cohesive offering.

From a switching cost perspective, customers benefit from deeply embedded compliance workflows and customized API configurations making migration costly once programs are launched at scale.

Industry Context and Competitive Positioning

In the broader payment ecosystem Marqeta sits prominently as an issuer processor bridging issuing banks that sponsor BINs (Bank Identification Numbers), card networks like Visa/Mastercard facilitating settlement infrastructure, acquiring processors working downstream with merchants, and the fintech clients building user-facing payment propositions [S1].

Competitive pressures emanate largely from both legacy incumbent processors modernizing their platforms towards API accessibility as well as emerging fintech pure plays attempting disruptive models [S1]. However, Marqeta’s comprehensive compliance certifications across regions coupled with robust banking partnerships create tangible moat elements [N2][S1].

Notwithstanding these strengths risks remain concentrated around customer concentration—Block accounts for roughly 45% of revenues—with renewal pricing dynamics posing margin risk if such relationships weaken or shift unfavorably during contract renegotiations [S16][S18]. Regulatory environments require continual adaptation which can increase operational costs or delay product rollout timelines.

Key Drivers Fueling Growth Prospects

Structural growth drivers underpinning Marqeta’s expansion include accelerated adoption of embedded finance solutions where companies embed card issuing natively into apps catering to consumers’ seamless spending journeys. Total Processing Volume scaled to $382.5 billion in 2025 growing at an impressive 31% CAGR over two consecutive years evidences persistent strong demand for programmable payment rails [S1].

Product innovation such as enhancements in rewards integration and dynamic spend controls augments stickiness among existing clients while opening new avenues for monetization through ancillary services like tokenization and fraud management upsells [N2][S2]. The successful integration of recent acquisitions such as TransactPay also broadens Marqeta’s exposure into supplementary digital wallet ecosystems globally enhancing addressable market size.

Operational leverage continues to emerge as fixed cost absorption improves alongside volume-driven revenue; adjusted EBITDA margins expanding quarter-over-quarter reflect maturing economies of scale within technology infrastructure and sales efficiency gains arising from increasing client wallet share.

Risks and Constraints to Monitor

Noteworthy risks detailed in filings underscore client concentration vulnerabilities—with largest client Block contributing near half the net revenue base—such dependency could cause sharp top-line fluctuations if client engagement diminishes or contract terms deteriorate [S16][S18]. Timing nuances surrounding network incentive recognition add earnings volatility while ongoing macroeconomic challenges influencing discretionary consumer spending could slow TPV expansion rates adversely affecting profitability projections.

Additional watchpoints involve complex regulatory landscapes inherent to financial services including evolving card network rules along with heightened scrutiny on cybersecurity practices requiring continual product investment plus possible litigation outcomes given ongoing securities class action lawsuits against the company which could impose reputational or financial constraints if unresolved favorably [S16][N3].

Finally, the impending June 2026 shareholder vote on a reverse stock split raises liquidity considerations—all else equal reduced share count can increase per-share price but potentially impair trading volumes affecting investor base composition [S16][S3].

Near-Term Catalysts and Watchpoints

Investors and stakeholders should closely monitor several upcoming junctures: primarily the impact of achieving proposed volume incentives thresholds governing sizable network rebates influencing future margin profiles per quarterly disclosures — realization beyond forecasted levels would bode well for earnings sustainability [S2][N2]. Renewals or re-pricing negotiations with marquee clients such as Block will provide directional signals on customer stickiness amidst competitive advances.

The June 10th reverse stock split vote results also merit attention given potential implications for market perception although uncertainties persist regarding ultimate share price behavior post-split given prevailing market conditions [S3][N3]. Continued announcements around product enhancements or new partnership wins will further clarify growth momentum extending beyond current core markets.

Current Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $675mm | |

| 2026-03-31 | ||

| Current assets | $1188mm | |

| 2026-03-31 | ||

| Current liabilities | $721mm | |

| 2026-03-31 | ||

| Current ratio | 1.65x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Marqeta’s liquidity position remains robust with nearly $675 million in cash reserves supporting working capital needs comfortably reinforced by a current ratio standing at approximately 1.65 as of March-end 2026 [F1][S2]. While balance sheet strength does not preclude future volatility given operating losses historically recorded through December prior year (-$13.9 million net income FY2025-end), recent positive earnings performance signals improving cash flow dynamics underpinned by disciplined expense management complemented by stable investing activities primarily catering to software development capital expenditures [F1][S17]. This enables continued funding flexibility spanning product innovation investments alongside selective share repurchase programs albeit moderated relative to prior periods reflecting capital allocation prudence amidst market headwinds.

This analysis reflects information available through May 6, 2026 based on SEC filings including the latest quarterly Form 10-Q dated May 5th, supplemental company disclosures filed contemporaneously per Form 8-Ks on May 5th as well as documented earnings commentary accessible via public transcripts. All figures pertain specifically to reported GAAP or reconciled non-GAAP measures cited from primary sources without speculative extrapolation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments