Atomera Advances MST Licensing Amid Semiconductor Innovation Spotlight

Atomera’s latest quarterly update underscores continued progress and challenges in commercializing its MST thin film technology in semiconductors.

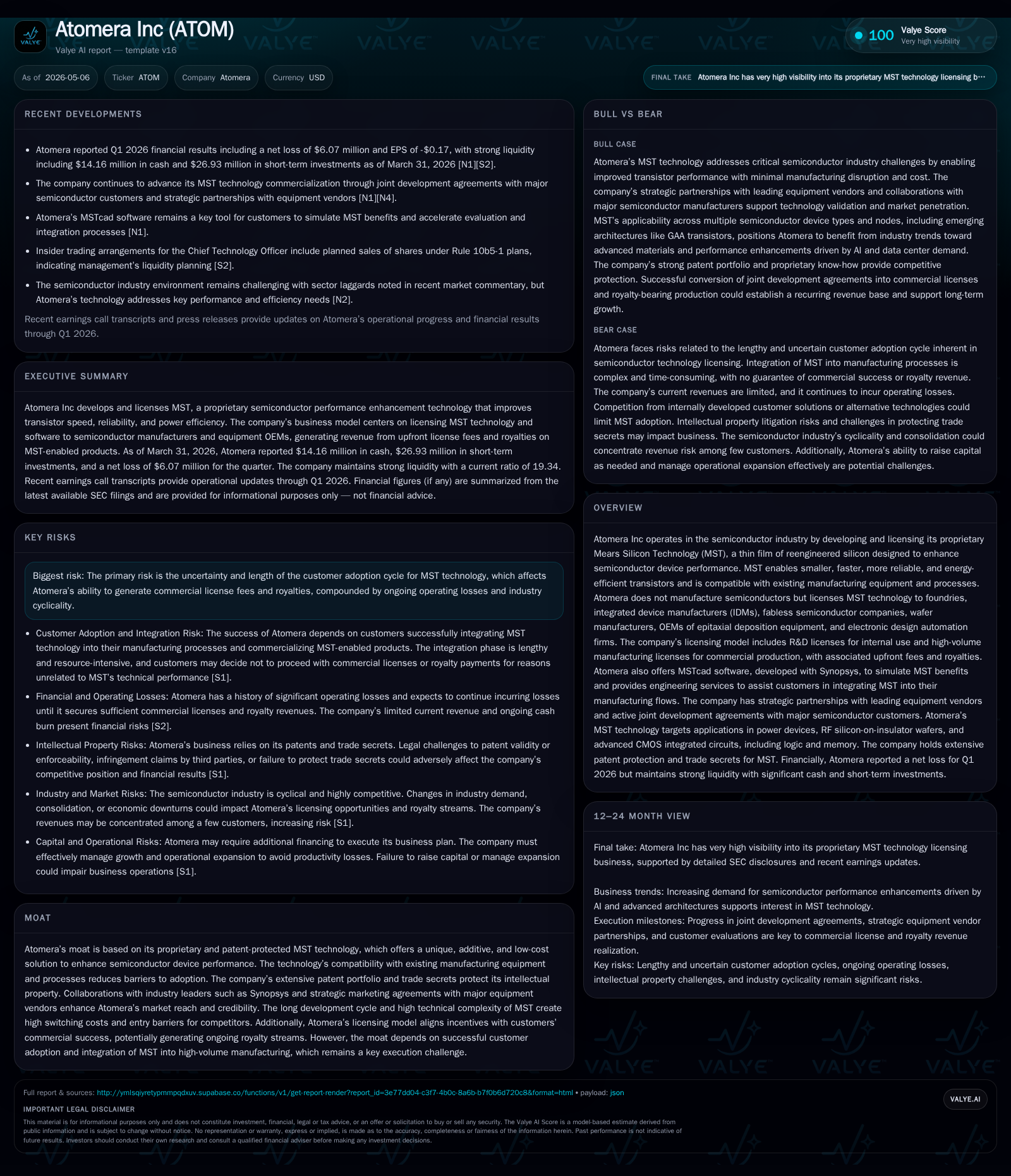

Atomera Inc’s 10-Q filing for Q1 2026 reveals steady advancement in its licensing efforts and engineering collaborations, reflecting incremental milestones toward commercial adoption of its proprietary MST technology. The company remains within early-stage commercialization, highlighted by joint development agreements with leading semiconductor firms but continues to face delays typical of semiconductor material innovation. Its licensing model aligns incentives with foundries, IDMs, and fabless manufacturers through upfront fees and royalties, supported by patented additive silicon technology that enhances transistor performance. Critical upcoming catalysts include conversion of R&D licenses to high-volume manufacturing licenses and progress in technology qualification phases. Risks persist around adoption cycle length, customer concentration, and intellectual property enforcement.

Latest Quarterly Update: Key Developments from the 10-Q Filing

Atomera’s Q1 2026 10-Q filing [S2] alongside an accompanying 8-K release [S3] highlights the company’s continued focus on advancing its proprietary Mears Silicon Technology (MST) toward commercial licensing agreements. The firm remains engaged in active joint development agreements with semiconductor manufacturers aiming to validate MST integration within fab processes. Although the company has not announced new commercial license signings this quarter, it reports engineering progress consistent with moving toward qualification milestones required before high-volume manufacturing (HVM) licenses can be granted.

Management emphasizes the gradual transition path—from paid evaluation licenses enabling internal use and testing up through full commercial licenses tied to wafer production royalties. The filings also note no material changes in risk factors while reaffirming ongoing operating losses aligned with R&D investments. Concurrently, two Rule 10b5-1 trading plans adopted by the CTO suggest normal leadership equity monetization during this phase [S2]. Operator discussions during the contemporaneous earnings call transcript [N1] stress measured optimism but acknowledge semiconductor industry cyclicality and extended qualification timelines.

Atomera’s Business Model: MST Licensing and Ecosystem Integration

Atomera earns revenue primarily by licensing its patented additive silicon thin-film technology—MST—to various semiconductor industry players including foundries, integrated device manufacturers (IDMs), fabless companies outsourcing production, wafer manufacturers supplying substrates, OEMs producing epitaxial deposition equipment (epi-tools), and electronic design automation (EDA) software firms [S1]. The model involves granting research & development licenses for internal evaluation or engineering services that facilitate customer integration efforts.

Once customers complete successful process integration and validation phases spanning wafer fabrication tool recipes and process design kits (PDKs), Atomera grants commercial high-volume manufacturing licenses enabling royalty-bearing product shipments. Royalties are typically based on wafer or device sales prices. Additionally, Atomera offers MSTcad™ simulation software developed jointly with Synopsys that leverages TCAD methods for evaluating MST benefits at the device design level—effectively lowering technical risk and accelerating customer adoption cycles.

This approach allows Atomera to monetize at multiple points along the innovation funnel: initial simulation/modeling access; paid engineering integration services; evaluation licenses; then fully licensed production releases. It also fosters ecosystem partnerships especially with epi machine OEMs who supply standard tools configured to deposit MST films seamlessly into existing fabs. A strategic marketing agreement signed in April 2025 with a major capital equipment vendor aims to diffuse MST technology across GAA logic and DRAM segments by embedding certified MST deposition processes into their reactor portfolios [S1].

Mears Silicon Technology: Technical Overview and Competitive Moat

MST is an engineered silicon thin film that when added within standard CMOS or compound semiconductor fabrication flows enables smaller transistor geometries with enhanced drive current, decreased leakage variability, improved reliability under stress conditions, and lower power consumption [S1]. Because it is additive rather than replacement technology, MST can be incorporated into existing epitaxial depositions using widely deployed machinery without significant capital expenditure for fabs.

This compatibility represents a strong moat: it reduces switching costs relative to both legacy processes and alternative enhancement methods that might require costly retooling or process redesign. MST's portfolio of patents protects key aspects of this engineered film technology as well as associated process recipes practiced under license. Trade secrets complement patent coverage around deposition parameters.

Collaborations with Synopsys provide embedded TCAD models forming MSTcad software that simulates realistic device-level impact on transistor speed and power profiles—an essential capability given typical engineer skepticism prior to adopting new semiconductor materials or processes. This method shortens evaluation cycles significantly since designers can predict performance gains before deploying wafers for costly physical trials.

Industry Positioning: Competitors, Collaborations, and Adoption Challenges

Within the broader semiconductor materials ecosystem—encompassing foundries like TSMC or Samsung fabs; IDMs such as Intel; fabless firms like Nvidia; capital equipment OEMs like Applied Materials—Atomera occupies a specialized niche focused on additive silicon film innovations addressing transistor-level improvement challenges.

Direct competitors offering comparable patented additive films appear absent according to company disclosures [S1], although indirect competition arises from internal process innovations pursued by large fabs' R&D groups or alternative material providers targeting device scaling hurdles differently.

Semiconductor materials innovation notoriously involves protracted qualification cycles averaging multiple years due to complex reliability testing requirements intrinsic to multi-billion-dollar fabs' risk tolerance profiles. In line with this industry dynamic, Atomera’s partnership pipeline includes JDAs whose progress sometimes stalls—as evidenced by the paused license qualification with ST Microelectronics reported as a risk factor [S4]. This stall illustrates typical hurdles faced when integrating nascent technologies into tightly controlled fab environments reliant on proven yield stability.

Catalysts for Growth: Licensing Milestones and Market Expansion Opportunities

Long-term growth prospects rest on successfully shepherding engaged customers through key licensing funnel stages—from paid internal evaluation via JDAs toward consummated commercial HVM licenses accompanied by royalty streams derived from volume product sales [S1]. Demonstrated in recent filings is progress in wafer runs performed under JDAs aimed at generating qualifying data sets that can unlock these upgrades.

Strategic marketing collaboration with a leading epi tool OEM has potential multiplier effects by combining equipment sales growth with increased diffusion of MST recipes pre-embedded in hardware offerings marketed to GAA logic node customers and DRAM fabricators targeting sub-10nm geometries [N1]. Additionally, diversification into compound semiconductors such as gallium nitride (GaN) offers new applications where MST serves as a defect-buffer layer enhancing yield/cost tradeoffs sought by power/RF segment actors [S1].

Incremental license fee recognition alongside royalty accruals triggered by production ramp-up drives revenue visibility—and creates sustainable recurring cash flow aligned firmly with customers’ own business success since royalties scale proportionally with device volumes/prices.

Risks and Constraints: Adoption Delays, Customer Concentration, and Legal Exposure

The company continues to face considerable execution risks inherent in early-stage tech commercialization including elongated timescales for customer qualification approval processes that have historically taken over a decade within semiconductors [S4]. For Atomera this translates into delayed revenue generation impacting operating losses already elevated during intensive R&D phases.

Additionally, dependency on relatively few major partners poses concentration risks if those entities halt progression—as witnessed currently with ST Microelectronics’ license qualification temporarily paused [S4]. Legal risks also loom given possible patent infringement enforcement scenarios: litigation could disrupt relationships or cause distracting cost overruns diverting management attention away from core development priorities.

Furthermore, fluctuations in semiconductor industry cycles may compress customers’ capital expenditure budgets thereby slowing adoption rates even if technical merits stand firm. Intellectual property must remain vigorously defended via patents plus trade secret protections else unauthorized usage could erode competitive advantage.

Monitoring Ahead: Milestones, Customer Progress, and Industry Trends

Investors and observers should track announcements regarding conversion from evaluation JDAs into full-fledged manufacturing licenses indicating tangible traction milestones reached. Close attention is warranted regarding updates on license status specifically any reactivation or advancement regarding ST Microelectronics’ engagement or new customers entering similar phased processes [S2][N1].

Further indicators include royalty stream commencement referenced during quarterly calls signaling volume production initiation plus expansion of partnerships within capital equipment suppliers embedding MST recipes into standardized tools for broader market adoption.

Macro trends include monitoring semiconductor market demand dynamics powered by AI-induced compute growth incentivizing next-generation node transitions requiring advanced materials innovation such as offered by MST [S1]. Regulatory shifts or pricing adjustments in epi machines also affect how quickly fabs can embrace complementary enhancements like MST films integrated seamlessly.

Financial Profile and Liquidity Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $14.16mm | |

| 2026-03-31 | ||

| Current assets | $42.06mm | |

| 2026-03-31 | ||

| Current liabilities | $2.18mm | |

| 2026-03-31 | ||

| Current ratio | 19.34x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026, Atomera holds $14.16 million in cash & equivalents against $2.18 million in current liabilities, yielding a robust current ratio of approximately 19.3—a conservative liquidity position indicative of prudent balance sheet management amid ongoing negative cash flows from operations rooted principally in sustained R&D investments [F1]. Current assets total nearly $42.06 million providing additional buffer flexibility.

While revenues remain minimal reflecting early commercial ramp constraints ($62k reported end-2020 as last revenue marker absent update), losses continue consistent with expected pre-profitability phases foundational to licensing businesses transitioning from technology development towards monetization ramps [F1].

This analysis is based solely on publicly available filings and statements as of May 2026; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments