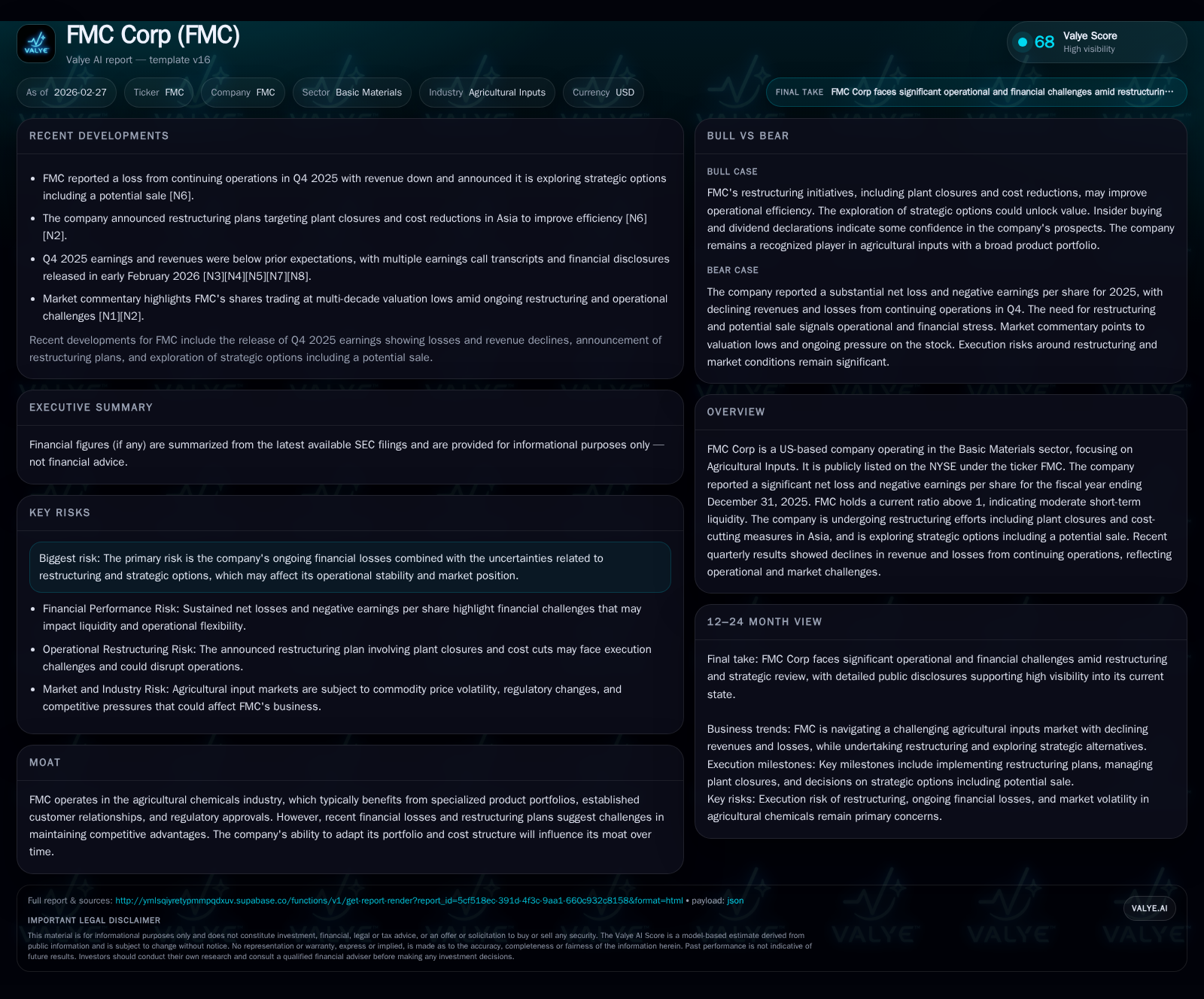

FMC Corp’s 2025 Downturn and Strategic Crossroads in Agricultural Inputs

FMC's significant financial losses and restructuring efforts in 2025 mark a pivotal juncture for its position in the global agrochemical sector.

After years of robust revenue growth fueled by proprietary insecticides and herbicides, FMC Corp suffered steep operating and net losses in fiscal 2025 amid declining prices and operational challenges. The company is executing strategic restructuring including geographic rationalization with asset sales and plant closures, especially in Asia, while advancing innovation around its diamide insecticides and precision ag platform. Capital allocation shows sustained dividends but no buybacks, reflecting constrained cash flow. Key forthcoming milestones include progress on restructuring outcomes and pipeline commercialization that will influence FMC’s ability to recover competitive footing.

From Growth Leader to Loss-Maker: Reviewing FMC’s Historical Financial Trajectory

FMC Corp demonstrated substantial revenue expansion leading up to fiscal 2018 when annual top-line reached approximately $4.29 billion according to SEC company facts [F1]. This growth reflected successful commercialization of proprietary agrochemicals, particularly within insecticides and herbicides segments. However, this momentum reversed sharply by 2025: operating income swung from positive $235 million in 2024 to a loss of $1.42 billion while net income plunged from a minor loss to a substantial deficit exceeding $1.7 billion [F1]. This severe margin pressure occurred despite relatively stable revenues underscoring cost structure challenges alongside pricing pressures.

Operating cash flow followed a similar trajectory; after generating healthy inflows through prior years (e.g., $737 million CFO in 2024), FMC posted negative operating cash flow in 2025 (-$6.2 million), signaling operational disruptions impacting cash generation capabilities [F1]. Concurrent capital expenditures increased year-over-year by nearly 42% to $96 million — indicating maintenance or growth investments despite profit compression.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -1721 | -6 | -1417 | 96 | -10457.1% |

| 2024 | -16 | 737 | 235 | 68 | -101.5% |

| 2023 | 1099 | -300 | 18 | 134 | +301.1% |

| 2022 | 274 | 660 | 395 | 142 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 291 | 0 | -102 |

| 2024 | 291 | 0 | 669 |

| 2023 | 291 | 75 | -434 |

| 2022 | 268 | 100 | 518 |

Source: SEC companyfacts cache [F1].

Note: Revenue values are principally available for FY2018; detailed revenue breakdowns for subsequent years are limited.

Key Drivers of Revenue Decline and Operating Losses in 2025

Several factors contributed to FMC's disappointing financial performance during late-2025 periods. Pricing deterioration across critical pesticide classes—driven by intensifying competition and macroeconomic pressures affecting crop input affordability—significantly eroded margins [N3][N4]. Operational headwinds included plant shutdowns primarily within Asian markets as part of strategic realignment efforts aimed at cost reduction and efficiency improvement [N1][S1]. These closures impacted production volumes and sales cadence.

Additional market challenges arose from softness in insecticide/herbicide demand linked to variable crop planting patterns and farmer spending cycles exacerbated by volatile commodity prices. FMC also acknowledged delays or softness in emerging markets contributing to overall revenue weakness late in the year [N3][N5].

Despite declining revenues, fixed manufacturing overheads and costs associated with plant closures exerted pressure on profitability driving deep operating losses.

Strategic Restructuring: Portfolio Rationalization and Geographic Focus

In response to worsening profitability trends, FMC initiated an aggressive restructuring focused on portfolio pruning and geographic rationalization [S3]. The company classified its India operations as held-for-sale—a move indicating intent to exit non-core or lower-margin markets [S1]. Disclosures show significant reductions in long-lived assets across Europe, Middle East & Africa (EMEA) and Asia regions between FY2024 and FY2025—from approximately $3.69 billion to $2.36 billion and $251 million to $124 million respectively—reflecting divestitures or write-downs aligned with strategic focus shifts [S1].

These actions aim not only to streamline cost structures but also reposition resources toward FMC’s core strengths, notably North America where the asset base remained stable near $843 million. Plant closures primarily within Asia reduce operational complexity though introduce execution risks around customer retention if supply adjusts materially.

Cost-cutting extends beyond site-level actions encompassing administrative expense reductions and productivity initiatives designed to restore competitiveness amid challenging market conditions.

Technology Edge: FMC’s Crop Protection Innovation Amidst Market Pressures

Despite near-term setbacks, FMC continues investing heavily in differentiated chemistry platforms supporting future growth potential [S1]. Central is its diamide-class insecticide portfolio highlighted by Rynaxypyr® (chlorantraniliprole), which generated approximately $800 million revenues during FY2025 alone—underscoring its global leadership status with broad-spectrum applications [S1]. These products benefit from unique modes of action reducing resistance risk, enabling sustainable crop protection alternatives.

Beyond synthetic chemistries, FMC pursues biological innovations characterized by stability under varied environmental conditions, compatibility across formulations, and low use rates—all promoting sustainability via reduced chemical load per acre [S1]. This growing suite complements the synthetic portfolio responding to increasing market preference for environmentally friendly solutions.

Digital agronomy tools constitute an additional pillar via FMC Precision Agriculture’s Arc™ platform—a mobile intelligence solution delivering predictive pest pressure modeling by integrating entomological data with real-time hyper-local weather inputs and sensor data across more than twenty-five countries managing twenty million acres currently [S1]. This scalable offering improves farmer decision-making on pesticide timing/application enhancing input efficiency while addressing sustainability imperatives.

Capital Structure and Liquidity: Navigating Cash Flow Constraints Amid Losses

Liquidity metrics suggest moderate short-term solvency despite stress. At year-end FY2025, current assets totaled approximately $4.96 billion against current liabilities near $3.76 billion yielding a current ratio around a comfortable 1.32—a modest buffer indicating short-term liquidity adequacy [F1]. However, cash flow dynamics reveal contraction with slightly negative operating cash flows (-$6.2 million) alongside elevated capital expenditures ($96 million), resulting in negative free cash flow approximating -$102 million during the year [F1].

SEC filings note ongoing debt obligations alongside unchanged credit facilities; management highlights risks related to funding flexibility if losses persist without operational turnaround or liquidity injections [S4][S5]. These stresses underscore the importance of swift execution of restructuring measures to stabilize profitability while controlling working capital demands tightly.

Capital Allocation Trends: Dividends Maintained Amid Cessation of Buybacks

Despite financial distress, FMC maintained dividends near consistent levels (~$291 million paid in FY2025), reflecting commitment or contractual obligations despite deteriorating earnings capacity [F1]. Conversely, share repurchase programs ceased post-2023 after prior reductions—indicating a conservative approach preserving liquidity amidst uncertainty compared with earlier buyback activity totaling up to $100 million annually.

Increasing capital expenditures amid restrained buybacks suggest prioritization of essential investments possibly linked to innovation projects including biologicals development or digital platform expansions despite margin pressures.

This balanced approach reflects efforts to support investor yield expectations through dividends while conserving cash given adverse operating conditions.

Outlook and Milestones: Monitoring Strategic Execution and Innovation Progress

Key upcoming milestones include progress updates on strategic alternatives such as potential sales processes involving regional units like the India business; execution milestones for planned plant closures predominantly across Asia/Emerging Markets; and observable improvements or stabilization of quarterly revenue post-restructuring phases [N1][N2].

Regulatory clearance timelines for novel active ingredients within the diamide pipeline remain critical catalysts for longer-term margin recovery once commercialized given their unique chemistries protected by intellectual property rights [S1]. Additionally, monitoring adoption rates and geographic expansion of the Arc™ precision agriculture platform will provide insight into successful leveraging of digital agronomy trends underpinning future sustainable growth vectors.

Together these factors form a strategic crucible determining FMC’s medium-term competitive positioning within an intensifying global agrochemical industry.

This analysis is based exclusively on information extracted from publicly available SEC filings ([F1], [S#]) and reputable news sources ([N#]) as indexed above through February 27, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments