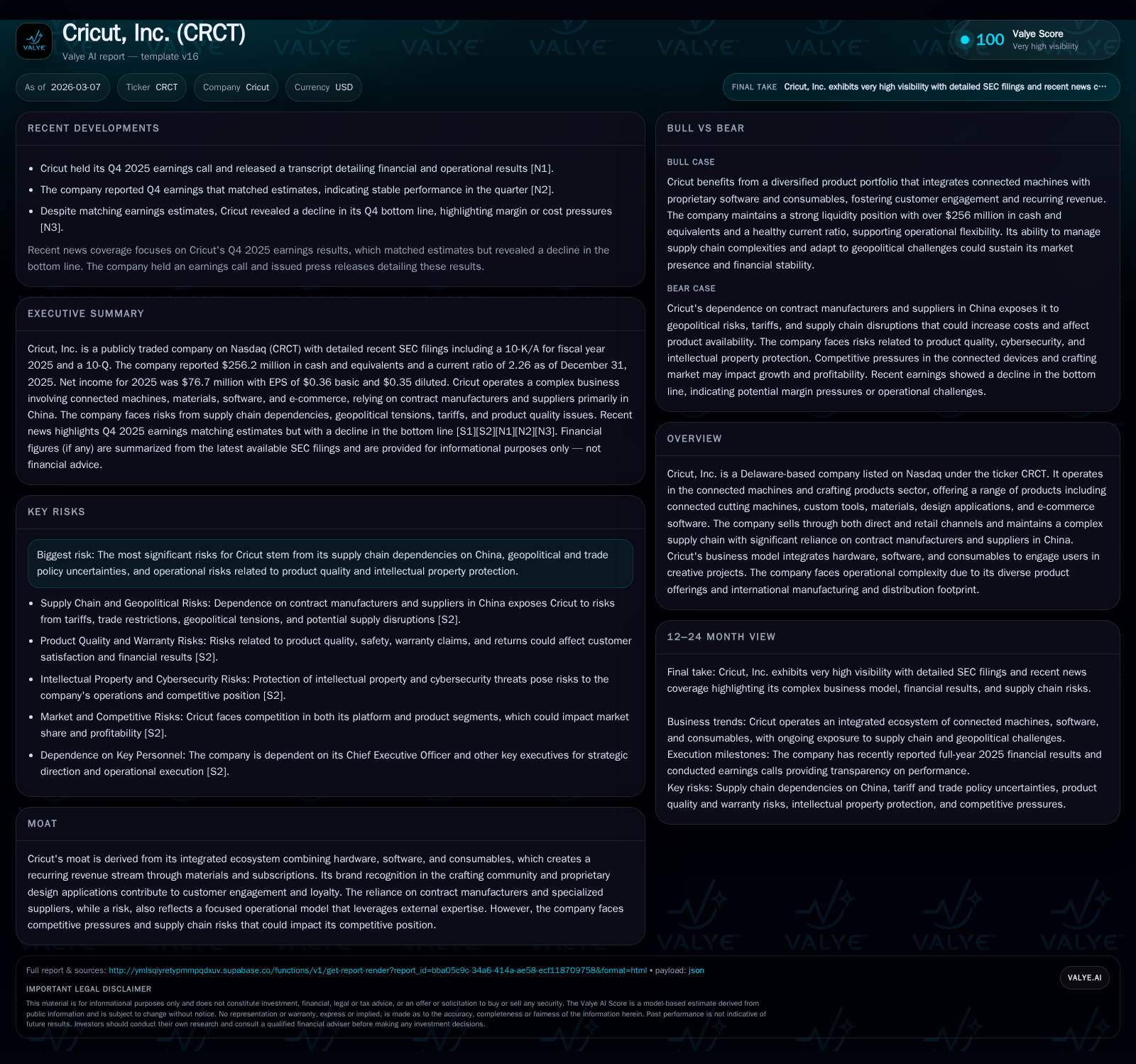

Cricut, Inc. Strengthens Earnings and Navigates Supply Risks in Connected Crafting

Cricut reports robust operating and net income growth driven by its integrated ecosystem despite mounting geopolitical supply chain challenges.

In fiscal 2025, Cricut, Inc. boosted its operating income by 26.2% and net income by 22.1%, fueled primarily by rising sales of materials and subscription services within its integrated hardware-software-consumable ecosystem. However, the company faces heightened risks from its concentrated supply chain in China amid evolving U.S. trade policies and export controls, which pose operational uncertainties. Notably, cash flows declined year over year due to shifting working capital needs, while capital expenditures increased to support growth initiatives. Investors should monitor subscription uptake and supply chain diversification efforts as key near-term indicators.

Profit Momentum: Reviewing Historical Growth Drivers Through FY2025

Cricut’s fiscal 2025 annual report reveals a pronounced acceleration in profitability driven by an increasingly sticky revenue model anchored on materials sales and subscription services linked to its connected crafting devices [F1]. Operating income grew sharply by 26.2% year over year from approximately $76.1 million in FY2024 to $96.0 million in FY2025, signaling substantial margin leverage associated with higher attachment rates in consumables and software monetization.

Net income followed suit with a 22.1% gain to $76.7 million over the same period, albeit trailing operating income growth slightly due to non-operating factors not extensively disclosed [F1]. Despite these earnings improvements, operating cash flow fell by around 24.4% year over year to $200.2 million—reflecting increased working capital needs likely tied to inventory buildup or accounts receivable growth amidst expanding direct-to-consumer channels.

Capital expenditure jumped nearly 69% from $2.05 million in FY2024 to $3.46 million in FY2025, marking investment into platform enhancement or scale-up efforts [F1]. This indicates Cricut’s commitment to innovation within its integrated product ecosystem even as it navigates complex supply environments.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 77 | 200 | 96 | 3 | +22.1% |

| 2024 | 63 | 265 | 76 | 2 | +17.1% |

| 2023 | 54 | 288 | 70 | 3 | -11.6% |

| 2022 | 61 | 118 | 80 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 202 | 25 | 197 |

| 2024 | 110 | 38 | 263 |

| 2023 | 294 | 20 | 285 |

| 2022 | 0 | 19 | 113 |

Source: SEC companyfacts cache [F1].

Operating income rebounded strongly after a dip in FY2023; CFO contraction relates possibly to changes in working capital; capex scaled up in FY2025.

The Dynamics of Cricut's Integrated Business Model and Recurring Revenue Streams

Cricut constructs competitive moats through an ecosystem approach where its hardware — precision cutting machines — functions synergistically with proprietary design software platforms and ongoing consumable sales such as materials and specialized tools [N1][S1]. This strategy leverages an expanding attach rate: as users own machines longer, they require consistent replenishment of craft materials and premium design content via subscriptions.

Such recurring revenue weight arising from SaaS integrations and e-commerce software differentiates Cricut from pure hardware vendors vulnerable to one-time purchase cycles [N1]. Management highlighted during the Q4 FY2025 earnings call that subscription metrics improved notably alongside material sales volume increases—a clear indication of cross-selling efficiencies within the ecosystem [N1].

The bespoke nature of Cricut’s design apps enhances user engagement while creating a switching cost barrier; combined with frequent new material launches aligned with craft trends, this encourages sustained consumer spending beyond initial hardware outlays [S1]. This model underpins both top-line resilience and margin enlargement through higher-margin consumables.

Geopolitical Trade Challenges and Their Impact on Manufacturing Operations

A critical operational constraint for Cricut lies in its significant dependency on contract manufacturers located in China along with component sourcing through specialized Chinese suppliers [S7][S8][S9]. Such concentration exposes the company to trade compliance risk exacerbated by escalating U.S.–China tensions encompassing tariff impositions, export controls on technology products, and inclusion of suppliers on restricted party lists such as the Entity List managed by the U.S Department of Commerce's BIS agency [S10][S11].

These regulatory actions have led to increased tariffs on Chinese-origin goods relevant to Cricut’s product components since 2018—with additional layers introduced more recently—forcing management to absorb higher costs or pass them partially downstream [S7][S9]. Export controls specifically challenge access to critical components like semiconductors sourced from Taiwan but assembled or integrated within Chinese manufacturing facilities [S9], inducing vulnerability amid geopolitical instability.

The potential need for manufacturing relocation or alternative supply routes presents significant cost inflation risks coupled with operational disruption during transition phases [S9]. While Cricut pursues mitigation strategies such as diversifying suppliers or exploring alternative locations, these remain imperfect shields against evolving government policies [S10]. The company discloses that failure to adapt rapidly could materially impact margins or product availability adversely [S11].

Emerging Growth Catalysts and Market Constraints to Watch

Forward-looking commentary emphasizes continued innovation within the connected crafting market as a principal catalyst for growth [N1][N2]. Key drivers include expansion of subscription services that deepen customer lifetime value, new machine models integrating advanced features appealing to diverse user segments, and geographic market penetration despite amplified tariff headwinds [N1][S3].

Concurrently, the company underscores the importance of navigating uncertainties related to international trade policies that could shape supply chain configurations materially [N1]. From an analytical perspective, monitoring metrics such as attach rate progression for consumables subscriptions alongside incremental international sales gains will be crucial signals.

Should Cricut achieve meaningful decoupling from Chinese manufacturing without severe margin erosion, it may unlock expanded addressable markets weighted toward direct digital commerce models leveraging SaaS platforms—a structural advantage against offline competitors [N2][S3]. Conversely, persistent geopolitical friction might cap growth velocity or delay new product deployments.

Capital Deployment: Evaluating Dividends, Buybacks, and Cash Flow Efficiency

Cricut’s capital allocation strategy reflects prudence tempered by a shareholder-friendly orientation [F1][S19][S22]. Dividend payouts more than doubled from approximately $110 million in FY2024 to over $202 million in FY2025 even as buyback volumes decreased from roughly $38 million down to approximately $25 million—signaling priority toward stable income distributions amid operating uncertainty.

Despite operating performance gains, declining CFO levels highlighting working capital tightening necessitate cautious liquidity stewardship [F1]. The modest absolute scale of capex (~$3-4 million) suggests focused investments rather than large-scale capacity builds.

An approximate return on equity near 22%, calculated by dividing latest fiscal net income ($76.7M) by fiscal year-end equity ($343M), points toward efficient profit generation relative to capital employed albeit against a backdrop of equity base contraction over recent years potentially due to buyback activity or other balance sheet shifts [F1].

Overall, capital deployment balances sustaining shareholder yield with corporate reinvestment needs amid geopolitical pressures constraining free cash flow expansion.

Forecast Signposts: Near-Term Milestones and Analytical Expectations

Explicit forward guidance was not prominently disclosed in recent SEC filings or earnings transcripts; however, key operational milestones include tracking subscription service adoption rates which directly influence recurring revenue strength alongside any announced product launches aimed at broadening addressable markets internationally [N1][N2].

On the supply side, progress toward diversification away from China-linked manufacturing chains will materially shape cost structures and availability profiles—areas ripe for investor focus based on public disclosures outlining relocation plans or supplier expansions [N1][S9].

Analytically, watching quarterly trends in margins relating to tariff impacts combined with updates on new software features enhancing ecosystem integration should serve as pulse checks for sustainability of current earnings momentum.

This analysis is based solely on publicly disclosed financial data filed with the SEC and management commentary available as of March 7, 2026 ([F1],[N1],[N2],[S#]). It does not constitute investment advice but aims to furnish a detailed understanding of Cricut’s recent financial trajectory alongside salient operational challenges inherent in global crafting device markets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments