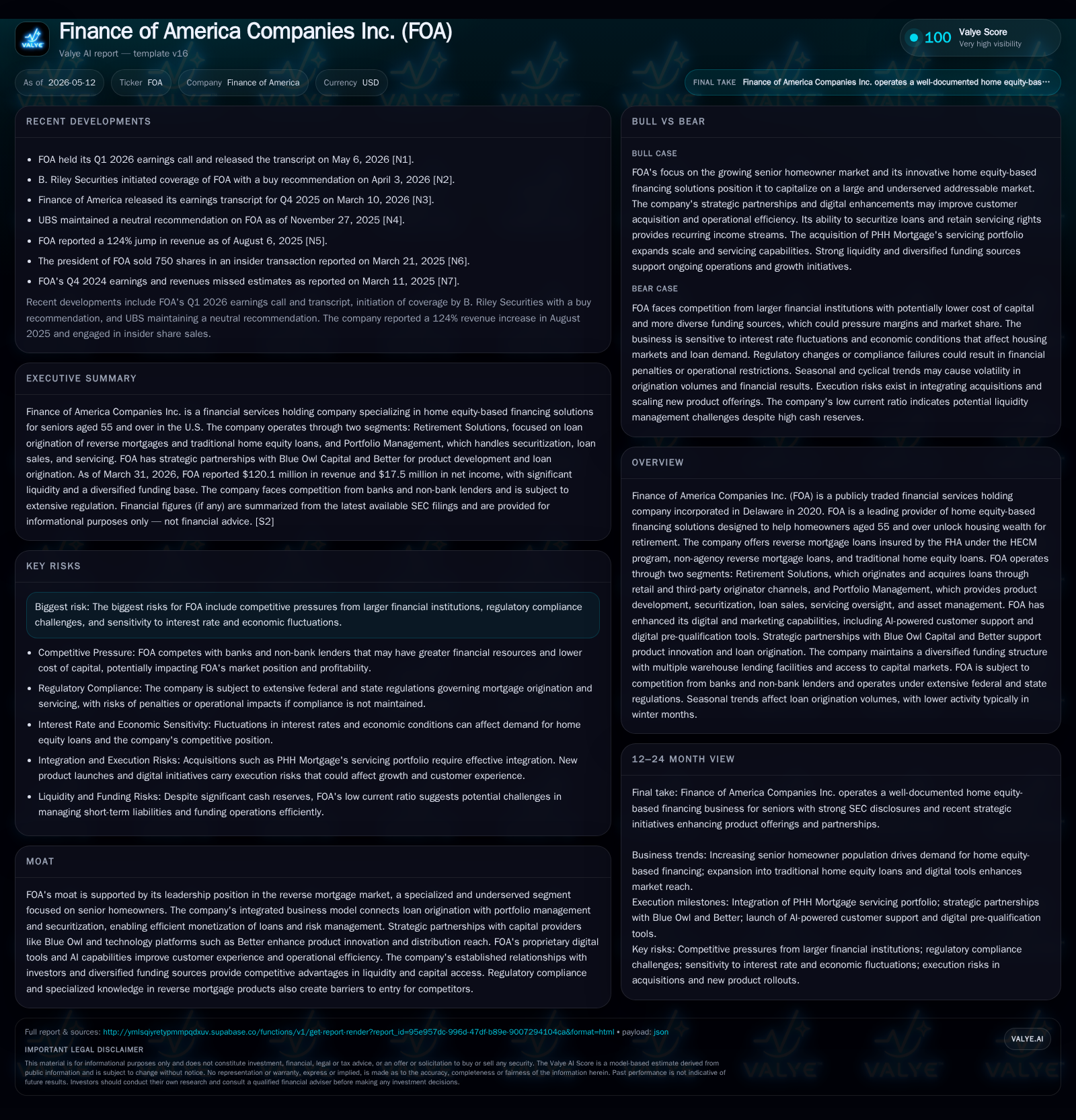

Finance of America’s Fresh Quarter Highlights Expanding Reverse Mortgage Innovation

FOA’s Q1 2026 reflects measurable progress in product diversification, capital partnerships, and operational efficiency within the reverse mortgage niche.

Finance of America Companies Inc. reported key operational advances in its first quarter of 2026, notably expanding traditional home equity loan origination alongside its core reverse mortgage products. The company extended strategic partnerships, particularly with Blue Owl, enhancing capital access and product innovation. Its integrated business model across origination and portfolio management continues to underpin competitive advantages in serving the underserved senior homeowner segment. Emerging digital tools, including AI-powered customer support and rapid pre-qualification, illustrate FOA's focus on customer experience and scalability amid a growing demographic tailwind.

Key Operating Developments in Q1 2026

The latest quarterly filing for Q1 ended March 31, 2026 [S2] reveals that Finance of America (FOA) has made substantive steps toward expanding its product suite beyond traditional reverse mortgages. For the first time in early 2026, FOA commenced originating traditional home equity loans via an AI-driven platform provided by Better Home & Finance Holding Company [S29]. These loans cater to borrowers seeking higher loan-to-value solutions than what reverse mortgages typically offer. Most notable is that this product launch complements FOA's existing reverse mortgage offerings, widening its addressable market.

Strategic partnership dynamics also stood out in early 2026 filings [S3], reaffirming the $2.5 billion purchase commitment from Blue Owl Capital funds for reverse mortgage loans originated or acquired by FOA Reverse LLC (FAR). These collaborations boost FOA's capital access for originating large volumes while continuously innovating financial offerings tailored for seniors wanting to unlock housing wealth.

Operationally, FOA expanded its digital capabilities with AI-integrated consumer tools: The 'Joy' chatbot enhances telephone support with ongoing expansion plans for online interactive support; a rapid three-minute pre-qualification digital tool launched mid-2025 now shows sustained traction [S1][N1]. Such initiatives intend to improve customer conversion rates and reduce loan processing friction.

Servicing improvements are underway to streamline resolution timelines on maturing loans and provide more borrower touchpoints post-loan maturity — critical given the complex servicing requirements specific to non-agency reverse mortgages [S4][S7]. This holistic approach to servicing aims to mitigate losses and optimize overall portfolio yield.

Finally, FOA announced intentions around acquiring a residential reverse mortgage portfolio from PHH Mortgage Corporation under terms subject to regulatory approvals [S24][S25], which would expand scale and servicing income if consummated.

Business Model: Specialized Reverse Mortgage and Home Equity Solutions

FOA’s revenues derive principally from two segments delineating the loan lifecycle stages: Retirement Solutions and Portfolio Management [S1][S6][S7].

Retirement Solutions handles all loan originations—principally encompassing loans insured by FHA’s HECM program (government-backed reverse mortgages), non-agency reverse mortgage loans (not FHA insured), and newly initiated traditional home equity loans since late 2025. Originations occur through both centralized retail channels and a broad network of third-party originators (TPOs), consisting primarily of mortgage brokers who facilitate volume but also require specialized compliance knowledge due to the FHA rules involved.

Portfolio Management takes originated loans to securitize them into different capital market instruments like HMBS guaranteed by Ginnie Mae or private MBS issuance for non-agency loans. The segment provides vital functions including product development, risk management, servicing oversight (often partnering with sub-servicers), asset sales or holding strategies for investment purposes, and managing retained interests. This integration allows FOA control over pricing discovery, risk retention decisions, and monitoring eventual loan performance beyond origination — a critical differentiator within the reverse mortgage ecosystem.

Revenue mechanics thus blend upfront origination fees with ongoing income from interest accruals on held portfolios plus performance-linked participation income retained after securitization—aligning incentives between loan quality at inception and long-term servicing outcomes.

Industry Position: Niche Leader with Integrated Origination and Portfolio Services

FOA occupies a unique leadership position in the U.S. senior home equity finance sector where few competitors specialize deeply within FHA-insured or non-agency reverse mortgages [S10][S11]. This niche benefits from high regulatory complexity that raises barriers to entry due to licensing requirements across all states plus the intricacies of federal housing programs such as HECMs.

The company’s dual-segment model affords integrated control over product designs tailored specifically for seniors aged 55+, enabling it to capture value both at loan origination and through capital markets channels more efficiently than peers relying on outsourcing or limited investor networks.

Partnerships with well-capitalized entities like Blue Owl furnish stable funding sources, allowing FOA to scale originations while managing interest rate exposure prudently [S11]. FOA’s direct broker-dealer registration facilitates market innovation and price discovery essential for proprietary securitization structures—a meaningful moat versus less established originators.

Moreover, FOA has invested heavily in digital customer engagement tools that reduce friction in application processes versus traditional mortgage industry standards—where paperwork delays historically hinder adoption among older borrowers [N2][S29].

Despite competitive pressures from larger banks or fintech entrants with broader resources, FOA’s blend of regulatory compliance expertise, targeted marketing (including national campaigns under “A Better Way with FOA”), sophisticated portfolio management strategies, and proprietary AI-enhanced services creates durable competitive differentiation [S19][N2].

Growth Drivers: Product Innovation, Market Penetration, and Capital Partnerships

The core growth driver remains secular demographic trends — approximately 11,400 Americans turn age 65 daily through at least 2026 [S1], expanding the addressable senior homeowner segment holding $14.66 trillion in aggregate home equity [S1]. Despite this affluent base, only an estimated ~2% currently utilize reverse mortgage products [S1], indicating substantial penetration headroom.

FOA’s recent product expansion into traditional home equity loans represents a strategic play targeting borrowers requiring financing solutions beyond typical reverse mortgage constraints on LTV ratios [S29]. This diversification responds to evolving client needs seeking more flexible borrowing against housing wealth while preserving primary mortgages.

Second lien non-agency reverse mortgages further widen FOA’s suite — prioritizing borrowers wishing to maintain existing low-rate first liens while adding reverse mortgage flexibility through subordinate positions. Plans to distribute these products via reseller servicer partnerships aim to accelerate adoption velocity by embedding offerings within existing mortgage servicing ecosystems [S6][S11].

Capital partnership synergy remains central; Blue Owl commitments provide durable purchasing capacity ensuring FOA can continually monetize new originations effectively while joint initiatives foster future pipeline innovation focused on retirement security enhancement programs tailored specifically for seniors’ evolving financial preferences [S11][N1].

Digital innovation contributes incremental efficiency gains: Automated pre-qualification cuts initial approval timeframes massively versus industry averages; AI chatbots enhance constant consumer engagement reducing service costs while improving satisfaction scores—supporting higher application completion rates thus fueling pipeline growth at scale [N1][S29].

Risk Factors and Challenges: Regulatory Sensitivities, Competition, and Economic Cycles

FOA operates under stringent federal regulations due to FHA-insured products alongside overlapping state licensing regimes across all operating jurisdictions [S21][S27]. Compliance demands impose ongoing costs impacting margins negatively should rules tighten further or enforcement intensify.

Interest rate environment volatility poses risks as elevated rates dampen borrower demand or alter loan economics adversely—competitors with locked-in lower capital costs may price more aggressively during rising rate cycles constraining FOA’s market share potential temporarily [S10][N2].

Competition from larger banks or diversified non-bank lenders armed with deeper pockets could pressure pricing; however FOA’s specialized knowledge offers a buffer against commoditization risks common in broader conventional mortgage sectors.

Cybersecurity remains a material concern given sensitive personal data collected throughout lending processes. The appointment of an experienced CISO with government and financial sector pedigree underscores proactive risk mitigation focusing on robust IT security frameworks overseen directly by Board Audit Committees ensuring alignment between governance priorities and operational safeguards [S21].

Servicing complexity intrinsic to aging loan portfolios requires continuous operational investments; lapses can lead to losses or reputational harm especially as borrower heirs navigate loan maturities [S4][S7].

Upcoming Milestones and Monitor Points

Attention will focus on Q2 onward earnings releases evaluating origination volume trends following new product launches including second lien reverses. Execution on the PHH portfolio acquisition scheduled per agreements contingent on Ginnie Mae approvals offers incremental scale benefits worth tracking closely [S24][S25]. Continued enhancements in digital tools deployment efficacy metrics such as pre-qualification completion rates or chatbot issue resolution effectiveness will also serve as leading indicators around customer acquisition improvements. Furthermore, developments regarding HMBS 2.0 securitization eligibility expansions could unlock new capital market channels altering future loan monetization economics positively for FOA [S11]. Finally monitoring payment delinquency trends or changes in regulatory frameworks concerning consumer protection could signal operating cost shifts necessitating management response.

Latest Financial Snapshot Supporting Operational Analysis

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $108mm | |

| 2026-03-31 | ||

| Total debt | $358mm | |

| 2025-12-31 | ||

| Net debt | $250mm | |

| 2025-12-31 | ||

| Current ratio | 0.05x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Amount (USD) |

|---|---|

| Cash & Equivalents | $107,656,000 |

| Total Debt | $357,547,000 |

| Net Debt | $249,891,000 |

| Annualized Revenue | $497,432,000 |

As of quarter-end March 31, 2026 cash reserves remain robust at approximately $108 million while total debt measured at end-2025 stands near $358 million. The resulting net debt position supports sufficient liquidity for ongoing growth initiatives including marketing expansion and technology investments without acute refinancing pressures identified in recent disclosures [F1][S2]. Annualized revenues approximate $497 million illustrating operational scale enabling reinvestment into innovation pipelines critical for sustaining competitive positioning within this specialized sector.

This analysis synthesizes publicly filed SEC materials as well as corroborative news transcripts without providing investment advice or recommendations. All financial figures are precisely referenced per XBRL data points or official SEC disclosures. Readers are encouraged to review original filings for comprehensive detail.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments