Odyssey Marine Exploration Advances Merger Plans Under Capital Constraints

The company's latest quarterly update underscores active merger progress amid significant liquidity challenges and regulatory risks.

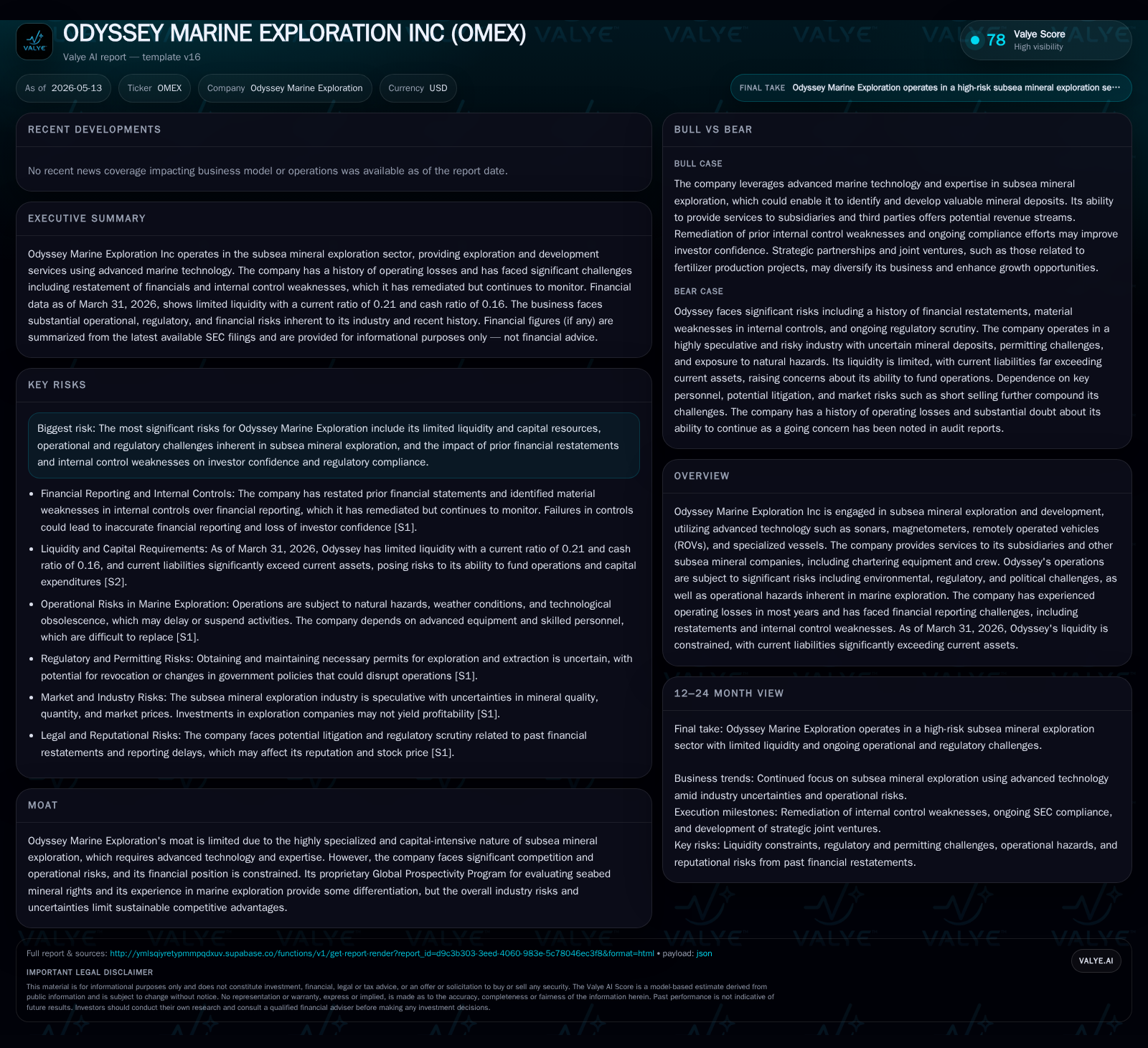

Odyssey Marine Exploration's May 2026 10-Q reveals tangible operational shifts aligned with its ongoing merger execution with American Ocean Minerals Corporation (AOM), aimed at bolstering scale and resource capacity. This strategic transition unfolds against a backdrop of severe liquidity constraints, intense subsea mineral exploration competition, and the legacy of financial reporting challenges that have impacted investor confidence. Growth prospects hinge heavily on merger-related synergies and regulatory milestone achievements, while near-term risks include delayed merger closing, governance uncertainties, and persistent capital scarcity.

Latest Operating Developments Highlight Merger-Driven Transition

Odyssey Marine Exploration's most recent quarterly filing dated May 12, 2026 ([S2]) foregrounds the active pace of its proposed merger with American Ocean Minerals Corporation (AOM), targeting completion in the late second to early third quarter of 2026. Key operational highlights from this 10-Q emphasize that Odyssey has progressed materially in executing the Agreement and Plan of Merger signed April 8, 2026 ([S27]), including arrangements for equity issuance under exemption from registration to facilitate transaction funding ([S3], [S10]).

The merger terms convert outstanding AOM shares into Odyssey shares at a conversion ratio of approximately 4.5:1, with preferred stock issuance contingencies designed to manage aggregated ownership thresholds ([S27], [S28]). These structural elements underscore both strategic consolidation intent and governance considerations necessary under current market realities.

Operationally, management has signaled focus on transitional cost control and integration readiness while acknowledging potential expense variability intrinsic to the pending transaction ([S3], [S5]). Such commentary is critical given Odyssey's existing liquidity limitations noted later. Furthermore, the company is advancing reorganization related to its Oceanica Resources Mexico (ORM) assets—transferred into a liquidating trust structure intended to preserve value pending Mexican government approvals for project advancement ([S20], [S9]).

Collectively, this operating update signals that Odyssey's near-term business emphasis is pivoting significantly toward consummating a complex merger transaction that could shore up resource base but also involves meaningful execution risk.

Business Model Overview: Subsea Mineral Exploration’s Capital Intensity and Specialized Offerings

At its core, Odyssey Marine Exploration generates revenue primarily via subsea mineral exploration employing specialized vessels equipped with technology such as remotely operated vehicles (ROVs), sonars, magnetometers, as well as proprietary analytical programs like its Global Prospectivity Program ([S1]). The company leases vessels and equipment both internally within subsidiaries and externally to other industry players.

This niche demands substantial upfront investment given the scale of marine hardware deployment combined with long lead times typical in seabed mineral rights evaluations and resource development phases ([S1]). Odyssey’s offering is differentiated modestly through experience in navigating challenging deep-sea environments and data-driven prospectivity assessments; however, competitive pressures arise from other entities wielding similar technological toolsets ([valye_report_excerpt.moat]).

Contract structures often include multiphase commitments contingent on exploration success metrics or regulatory clearances which influence revenue timing and profile stability. Customer switching costs appear low given several competitors operate within overlapping geographic zones; this dynamic curtails durable pricing power despite the technical barriers.

Industry Context and Competitive Dynamics in Subsea Resource Services

The subsea mineral exploration sector is characterized by high capital intensity compounded by environmental regulation complexity across multiple jurisdictions ([S1], [S11]). International laws around seabed mining remain fluid—complicating permit acquisition—and amplify political risk for operators like Odyssey facing potential restrictions or delays.

Key competitors range from similarly focused exploration firms to diversified mining conglomerates eyeing underwater resource diversification. Entry barriers hinge on access to expensive vessel fleets capable of ocean-floor operation depths requiring advanced ROV technology combined with geo-data processing capabilities ([valye_report_excerpt.moat]).

Operational hazards intrinsic to marine environments impose regular maintenance cycles along with insurance cost layers that further constrain margin expansion.

Merger-Related Growth Drivers and External Enablers

Odyssey’s pending merger with AOM carries significant promise as a catalyst for scale economies by combining complementary fleets, intellectual property including proprietary seabed prospectivity models, and management expertise ([S3], [S4], [S5]). The merger also targets improved capital access through PIPE subscription agreements outlined in filing exhibits ([S23]), which are critical given Odyssey’s constrained funding situation.

External demand drivers stem from prolonged secular interest in subsea minerals fueled by global decarbonization trends increasing reliance on battery metals and rare earth elements found on ocean floors. This macro tailwind supports expansion prospects subject to overcoming operational hurdles.

Successful completion of the ORM asset disposition described as integral to the merger deal will unlock capital for reinvestment or reduce balance sheet strain once Mexican government project approvals are secured ([S20], [S9]). These enablement milestones mark important KPIs tied directly to enlarged resource potential.

Risk Factors Exacerbated by Financial Reporting History and Market Conditions

The risk profile for Odyssey remains elevated principally due to its history of financial restatements which have resulted in material weaknesses within internal controls over financial reporting ([S1], [S11]). Though remediation efforts are underway per disclosures ([S11]), lingering concerns diminish investor confidence and expose the company to regulatory scrutiny.

Liquidity constraints manifest starkly with a March 31 snapshot showing cash reserves at approximately $2.1 million against current liabilities exceeding $13.3 million resulting in a precarious current ratio of 0.21 ([F1]). This imbalance amplifies execution risks related to funding ongoing operations or any unanticipated merger-related expenses.

Additional operational risks include potential seizures of pledged assets if payment obligations falter ([S11]), dependence on volatile stock price compliance for Nasdaq listing continuity ([S29]), plus exposure to legal actions stemming from prior restatements or merger transactions litigation risk ([S11],[S12],[S8]).

Competitive dynamics may further pressure operating margins if rivals capitalize more successfully on environmental permits or faster vessel deployment rhythms.

Near-Term Milestones and Key Indicators to Watch

Market participants should monitor several time-sensitive events crucial for validating Odyssey’s renovation trajectory:

- Completion of shareholder approval processes facilitated through anticipated proxy statement/prospectus filings post-merger agreement disclosure ([S7], [S21], [S24])

- Closure of PIPE financing rounds implicit in meeting cash flow requirements needed for effective post-merger operations ([S3], [S23])

- Regulatory progress concerning ORM HoldCo asset disposition steps aligned with Mexican governmental project sanctioning impacting long-term asset liquidity ([S9])

- Integration cost disclosures within subsequent SEC filings indicating management’s ability to forecast synergy realization without excessive budget overruns ([S2],[S5]) Watching equity share price trends relative to Nasdaq listing rules compliance thresholds remains important due to delisting risks underlying liquidity fears ([S29]).

Current Financial Profile and Liquidity Assessment

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $2mm | |

| 2026-03-31 | ||

| Current assets | $3mm | |

| 2026-03-31 | ||

| Current liabilities | $13mm | |

| 2026-03-31 | ||

| Current ratio | 0.21x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026, Odyssey Marine Exploration holds $2.1 million in cash and equivalents against current liabilities of $13.3 million leading to a notably stressed current ratio of 0.21 reflecting immediate liquidity challenges ([F1]). The company reported no outstanding debt as per best-effort data available from historical trackers but remains highly dependent on timely capital infusions mainly derived from merger-related equity issuances documented in recent SEC event filings ([F1], [S2],[S3]).

This financial snapshot underscores the imperative nature of successful merger closure combined with external financing access as linchpins enabling continuation of exploration activities without asset disposals at distress prices risking operational viability.

This analysis synthesizes publicly filed disclosures finalized through May 12, 2026 focusing exclusively on substantiated operating facts without forecasting performance outcomes or providing investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments