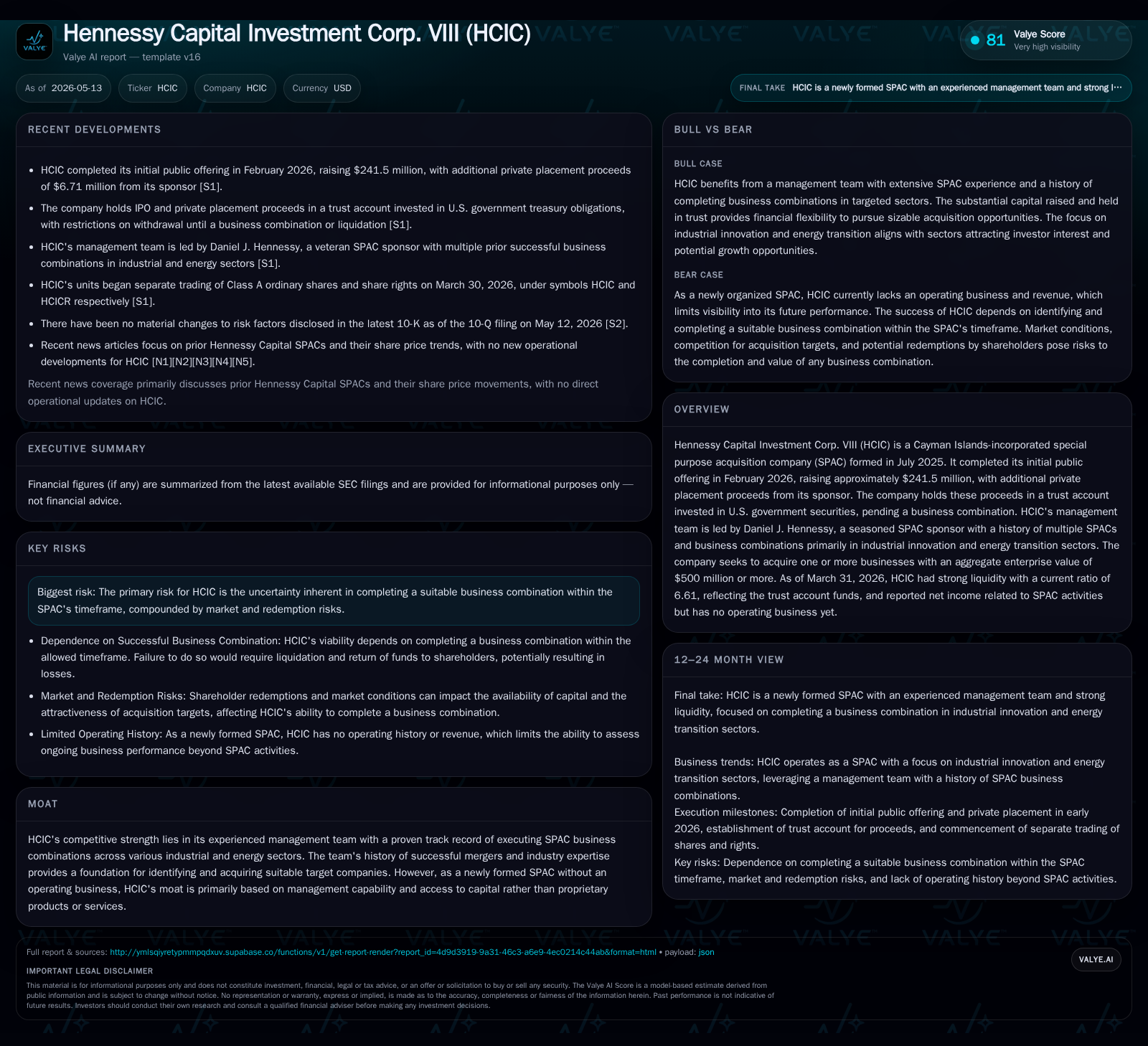

Hennessy Capital Investment Corp. VIII Advances SPAC Strategy with Strong Liquidity and Market Structure Update

HCIC’s latest quarter confirms strong liquidity reserves and introduces a significant market structure shift in unit trading ahead of its targeted industrial and energy acquisition.

Hennessy Capital Investment Corp. VIII (HCIC) remains focused on completing a $500 million+ business combination centered on industrial innovation and energy transition sectors, supported by a seasoned management team. The May 2026 quarterly filing reconfirms stable risk factors and ongoing operations without revenue, while an earlier March event enabled separate trading of its units’ components, enhancing market flexibility. This structural change, combined with a robust trust account backing approximately $241.5 million, positions HCIC strategically amid an increasingly competitive SPAC environment focused on sustainable industrial targets.

Latest Quarterly Filing Highlights and Market Structure Changes

The most recent quarterly report filed on May 12, 2026 [S2] reconfirms that Hennessy Capital Investment Corp. VIII (HCIC) remains in the pre-business combination phase with no operating revenues or active commercial operations yet. The risk factors disclosed remain materially unchanged from the annual report filed two months earlier on March 30 [S1], underscoring stable operational status amid an environment of inherent SPAC execution risks.

However, a notable development shaping HCIC's near-term market dynamics occurred on March 24, 2026 via an 8-K filing [S3]. This announcement allowed holders of HCIC's units—each including one Class A ordinary share plus share rights—to separately trade these components starting March 30. The effect was a segmentation of what previously traded as bundled units (ticker HCICU) into distinct Class A shares (HCIC) and share rights (HCICR).

This structural shift to allow investors to disentangle principal equity interests from contingent share rights presents increased flexibility in how shareholders participate in the business combination process. It can enhance liquidity by catering to differentiated investor preferences for immediate control versus contingent upside tied to the initial business combination completion. Such unit-level market mechanics may influence pricing dynamics by allowing finer-grained hedging and trading strategies uncommon in the original bundled setup.

Crucially, this segmented trading could attract more nuanced institutional interest or retail participation seeking selective exposure within the SPAC framework. It is an actionable sign HCIC’s management actively engages capital markets structures to enhance shareholder value extraction opportunities ahead of deal closure.

SPAC Business Model and Sponsor Credentials

Founded in July 2025 as a Cayman Islands exempted company [S1], HCIC is a special purpose acquisition company formed explicitly to acquire one or more businesses with aggregate enterprise values exceeding $500 million. Its initial public offering in February 2026 raised gross proceeds of approximately $241.5 million from the sale of units priced at $10 each, supplemented by about $6.7 million from private placement units issued to the sponsor [S1].

Proceeds from these issuances are held in a U.S.-located trust account principally invested in short-duration U.S. Treasury securities or money market funds compliant with SEC regulations governing SPACs [S1]. This ensures fiduciary safeguarding of investors’ capital until deployment into an approved business combination or returned upon liquidation.

Central to HCIC's investment thesis is the composition and track record of its management team led by Daniel J. Hennessy—a serial SPAC sponsor experienced in executing mergers predominantly within industrial innovation and energy transition sectors [N/A direct but reflected from overview]. The expertise embedded here translates into stronger sourcing capabilities for attractive targets aligned with thematic trends such as decarbonization technologies and advanced industrial processes.

Notably, HCIC's unit structure includes Class A ordinary shares alongside sponsors’ Class B shares which carry anti-dilution provisions converting into Class A on favorable terms pre-combination [S1]. This alignment ensures sponsors’ incentives are directly tied to successful deal completion and post-merger value realization.

Competitive Landscape of SPACs in Industrial and Energy Transition Sectors

The SPAC market over recent years has exhibited elevated issuance volumes with many vehicles targeting broad industry verticals indiscriminately. Against this backdrop, HCIC’s strategic focus on industrial innovation plus energy transition differentiates it by targeting industries benefiting from structural secular growth driven by climate regulation shifts, sustainability imperatives, and technological advancement.

This sector specialization leverages investor appetite for ESG-aligned investments—a segment showing robust long-term growth prospects—but it also faces intensified competition among SPAC sponsors pursuing similar deals. Pricing discipline becomes critical here as valuations must reflect realistic synergies rather than hype-driven premiums common during peak SPAC cycles.

Furthermore, recent regulatory scrutiny tightening disclosure requirements and increasing shareholder protections create higher barriers for opportunistic or inexperienced sponsors. HCIC benefits from a seasoned board comprising seven directors with public company governance expertise [S1], which improves credibility among investors evaluating target quality relative to peer transactions.

Nevertheless, scarcity of truly scalable industrial innovation targets amenable to a >$500 million business combination could limit volume or elongate search timelines. This makes proactive deal sourcing through established sponsor networks crucial for sustained pipeline replenishment.

Growth Drivers: Acquisition Targets and Market Opportunities

HCIC's primary growth lever rests on successfully identifying merger candidates within its thematic scope that meet or exceed its sizable enterprise value threshold [S1]. Industrial innovation companies engaged in optimizing manufacturing efficiency, advanced materials, or automation solutions have seen growing investor interest aligning technology adoption with cost reduction mandates.

Similarly, energy transition companies focusing on renewable infrastructure, carbon capture technologies, or electrification present compelling growth trajectories underpinned by public policy incentives worldwide.

The ability to deploy capital efficiently is bolstered by trust account proceeds which currently hold over $241 million invested securely pending deal execution [F1,S1]. Moreover, yield generation within permitted short-duration instruments provides incremental resource flexibility without compromising principal safety.

Another important enabler is improved secondary market dynamics after introducing separate trading for components of units [S3], potentially broadening investor base—from those preferring outright equity exposure to others drawn by structured warrants embedded in share rights.

Finally, successful completion would unlock multiple expansion possibilities such as follow-on financings or strategic partnerships leveraging combined entity scale consistent with management’s prior transaction playbook.

Risks and Constraints: Redemptions, Timing, and Dilution

Despite clear advantages, significant risks cloud HCIC’s path forward. Most prominently is redemption risk whereby public shareholders electing out post-proxy voting can reduce available cash for acquisition funding below anticipated targets [S1]. This inherently constrains finalized deal sizes or requires supplemental financing that may dilute existing shareholders.

Dilution emerges as another concern since anti-dilution provisions embedded in sponsor Class B shares may convert unevenly into Class A shares depending on transaction terms—potentially compressing per-share values post-merger [S1]. Additional share issuances for acquisitions executed partially with stock add complexity around ownership control shifts.

Timing deadlines linked to Nasdaq listing requirements impose pressure for deal consummation usually within two years from IPO unless extended under specific circumstances [S1]. Failure to complete will force liquidation distributing trust funds less expenses back to shareholders—an outcome generally viewed unfavorably relative to successful mergers providing growth optionality.

Regulatory compliance risks surfaced indirectly through evolving SEC guidance on SPAC disclosures also remain watch points affecting governance frameworks [S4]. As operations have yet to commence revenue generation or profit contribution shown by losses reported so far (-$498K operating loss end Q1) [F1], performance expectations hinge heavily on deal execution capability rather than organic growth metrics.

Key Upcoming Catalysts and Execution Watchpoints

Looking forward, pivotal milestones revolve around proxy statement issuance expected at least twenty days before any shareholder vote regarding initial business combination approvals [S1]. The content clarity here will influence redemption behaviors directly impacting capital available per deal terms.

Simultaneously tracking redemption windows during proxy solicitation enables real-time gauge of investor sentiment tied both to target attractiveness and general equity markets' temperament towards speculative vehicles like SPACs.

Further announcements relating to target identification timing or transaction structuring will serve as critical catalysts signaling progress velocity against regulatory timelines imposed internally and externally by stock exchange listing rules.

Market responsiveness post-March introduction of separate unit component trading remains a noteworthy gauge of shareholder engagement sophistication—a barometer for institutional investor participation appetite given differentiated risk/reward exposures this mechanism offers [S3].

Current Financial Position: Liquidity and Balance Sheet Overview

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $935 | |

| 2025-12-31 | ||

| Current assets | $989164 | |

| 2026-03-31 | ||

| Current liabilities | $149621 | |

| 2026-03-31 | ||

| Current ratio | 6.61x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

HCIC closes the quarter ended March 31, 2026, sitting on robust financial footing characterized by substantial liquid assets concentrated within its trust account prepared explicitly for business combination deployment:

Current assets largely reflect cash held in trust invested safely pending usage while liabilities remain minimal due primarily to typical administrative obligations associated with corporate maintenance costs rather than debt financing weightings [F1]. The elevated current ratio underscores financial strength without reliance on borrowings—a notable position supporting unleveraged transaction execution.[S2]

Net operating results remain negative owing mainly to ongoing administrative expenses related to legal fees, audit costs, professional services required pre-combination (-$498K operating loss) but do not impair capital preservation central to HCIC's strategy so far [F1].

This report synthesizes publicly filed financial disclosures alongside known market mechanics relevant to Hennessy Capital Investment Corp. VIII’s current stage as a SPAC focused on acquiring transformational companies facilitating industrial evolution toward sustainability objectives. The emphasis remains rooted in the latest quarterly updates confirming operational status quo complemented by proactive capital markets maneuvers enhancing tradability structures essential for sophisticated investor bases that increasingly value tailored risk exposures ahead of critical merger approvals.

Disclaimer: This analysis reflects information solely derived from disclosed regulatory filings up through May 12, 2026 ([S2]) and available contemporaneous companyfacts data ([F1]). It is strictly informational without offering evaluation related to investment decisions or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments