Primis Financial Corp. Reinforces Stability with Strategic Branch Optimization and Mortgage Integration

Primis Financial’s recent quarterly update underscores its focus on fortifying regional banking strength via branch network efficiency and enhanced mortgage lending capabilities.

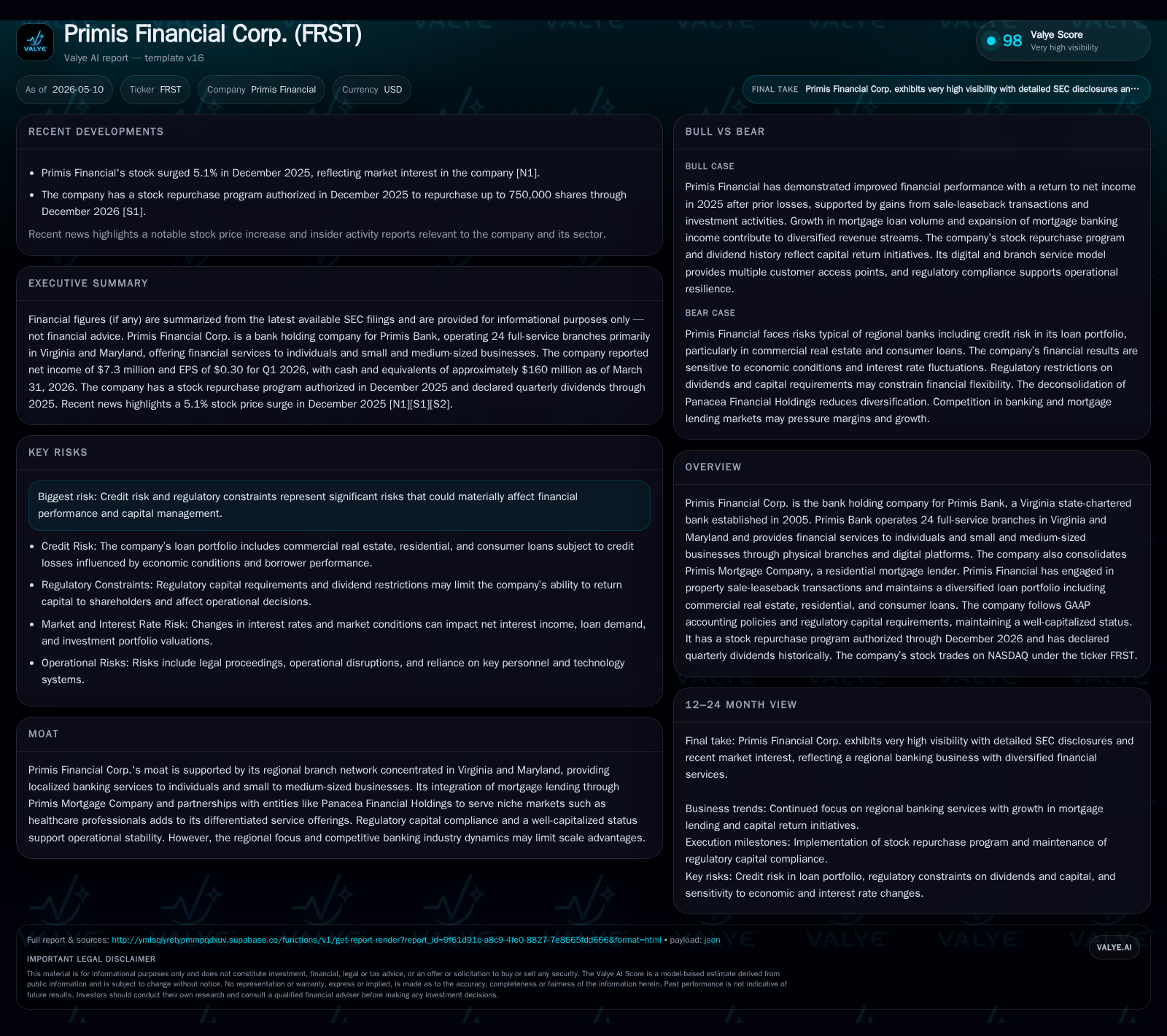

In its Q1 2026 filings, Primis Financial Corp. detailed sustained operational resilience supported by a well-capitalized balance sheet, steady branch network presence in Virginia and Maryland, and deepening integration with its residential mortgage lending unit. The company’s dividend declaration and ongoing stock repurchase authorization signal capital return discipline balanced against growth initiatives. Amid competitive pressures in regional banking, Primis leverages niche partnerships and digital platforms to diversify its loan portfolio and capture SME demand. Risks remain linked primarily to credit exposure in commercial real estate and regulatory capital requirements restricting flexibility.

Q1 2026 Operating Update: Key Developments and Dividend Policy

Primis Financial Corp.'s latest quarterly filing for the period ended March 31, 2026 delineates a steady operating footing characterized by continued compliance with regulatory capital requirements and disciplined capital return activity. Notably, in an April 23, 2026 press release incorporated by reference in an 8-K filing, the company declared a quarterly dividend payable May 22, 2026 to shareholders of record on May 8, confirming adherence to a consistent dividend distribution track record established since 2012 [S2][S3]. Concurrently, the Board maintains an active stock repurchase program authorized through December 18, 2026 with up to 750,000 shares eligible for buyback contingent on market conditions — underscoring a balanced focus on shareholder returns alongside strategic deployment of capital resources [S17].

Operationally, the quarterly report does not flag significant liquidity disruptions or material adverse events affecting financial condition. The continuity of a well-capitalized status underlines stable asset quality metrics and robust risk management practices across the diversified loan portfolio encompassing commercial real estate (CRE), residential mortgages, and consumer credits [S2][F1]. This foundational stability provides a platform for measured growth initiatives embedded within regional market dynamics.

Business Model Overview: Retail Banking and Mortgage Lending Integration

Primis Financial Corp. functions as the holding company for Primis Bank—a Virginia state-chartered bank with origins dating to 2005—and Primis Mortgage Company which collectively deliver integrated local financial services focused primarily on Virginia and Maryland markets [S1]. The bank's revenue model hinges on interest income generated from loans extended to individuals and small-to-medium enterprises (SMEs) embedded within its deposit-gathering network of 24 full-service physical branches supported by complementary digital delivery platforms [S1].

A critical component enhancing Primis' strategic position is its consolidated mortgage business where home loan origination complements core lending activities serving both individual consumers and real estate developers. This synergy bolsters fee income streams alongside interest income while enabling cross-selling within an established customer base attentive to localized service nuances prevalent in mid-Atlantic states [S1]. Further, property sale-leaseback transactions executed in recent years strategically monetize branch real estate assets while maintaining operational footprints via leases—an approach optimizing balance sheet efficiency [S1].

The customer base predominantly comprises retail consumers seeking deposit accounts, consumer loans including home equity products, alongside business owners requiring credit facilities tailored for CRE projects or general operational funding needs. This segmentation allows Primis to finesse product offerings adapting to cyclical economic factors affecting SMEs while sustaining engagement via physical presence complemented by evolving digital banking capabilities.

Competitive Landscape: Regional Focus and Differentiated Service Offerings

Within the Mid-Atlantic regional banking sector—dominated by a mix of national banks, regional bank franchises, and community banks—Primis occupies a niche defined by its concentrated branch network in Virginia (22 branches) and Maryland (2 branches) supplemented by strategic partnerships that extend reach into specialized customer segments [S1]. The company's alliance with Panacea Financial Holdings exemplifies this targeted approach by delivering financial products tailored specifically for healthcare professionals—a demographic exhibiting both creditworthiness and stable income patterns that can enhance portfolio resilience.

Scale limitations inherent in regional banking impede economies enjoyed by larger institutions; however, Primis mitigates this through localized customer relationships fostering loyalty via service customization unavailable from bigger peers. Regulatory capital constraints mandate prudent asset growth paced against maintaining "well capitalized" designations under federal guidelines restricting leverage elasticity—thus influencing loan-to-deposit ratios and provisioning allowances [S1].

The differentiated offering bridging conventional retail deposits with integrated mortgage products, accompanied by investment in digital engagement channels, presents competitive advantages achieving stickiness in client relationships amid commoditized banking services. Pricing power appears moderate: while standard deposit margins are compressed industry-wide due to macroeconomic factors, specialized SME lending supported by relationship banking affords some margin preservation opportunities.

Growth Drivers: Digital Channels, Niche Market Partnerships, and Loan Portfolio Diversification

Primis Financial’s advancement pivots on three principal growth catalysts. First is leveraging enhanced digital platforms that augment customer acquisition and retention especially among tech-savvy younger demographics and SMEs seeking convenience without sacrificing personalized advisory support. These tools improve usage intensity metrics (e.g., transaction volumes per active customer), contributing incrementally to non-interest income streams while supporting broader deposit capture efforts [S2].

Second is expanding niche partnerships such as with Panacea Financial Holdings targeting healthcare professionals; this strategy offers improved credit profile balance within the loan portfolio by attracting borrowers engaged in relatively stable economic sectors less susceptible to cyclicality than broad CRE or consumer segments [S1].

Third is deliberate diversification of lending categories encompassing commercial real estate financing (both owner-occupied and non-owner occupied properties), construction loans tied to local development projects, residential mortgage originations through Primis Mortgage Company, as well as consumer loans including home equity lines of credit. This diversification reduces concentration risks typical for community banks reliant heavily on single loan product classes or geographies [S2][S1].[F1]

Together these drivers support steady albeit incremental growth aligned with conservative underwriting standards essential to managing credit cycles inherent to regional economies.

Risks and Constraints: Credit Exposure, Regulatory Compliance, and Market Limitations

Despite its strengths, Primis confronts multiple operational headwinds warranting close surveillance. Credit risk represents a foremost concern given sizable exposure to commercial real estate financing which is sensitive to economic downturns impacting tenant occupancy rates or property valuations locally [S1]. Rising delinquencies or valuations decline could materially affect loan loss provisions straining profitability.

Regulatory constraints impose another layer of complexity: maintaining capital ratios sufficient to sustain "well-capitalized" status curtails leverage capacity limiting rapid expansion alternatives without issuing new equity which could dilute incumbent shareholders. Dynamic adjustments required under evolving federal prudential standards require ongoing compliance investments diverting resources from growth initiatives.

Geographic concentration confined mainly within two states precludes benefits achievable through broader national diversification thereby amplifying exposure to localized economic disruptions or competitive encroachments from larger players entering Mid-Atlantic markets aggressively.

Furthermore technological adoption imperatives necessitate continual IT spend upgrades creating operational expenses that must be balanced against incremental income benefits amid an environment of compressed net interest margins generally affecting community banks nationally.

Outlook and What to Watch: Guidance, Capital Management, and Strategic Initiatives

Looking ahead through late 2026 the market will closely track several key indicators indicative of Primis’ execution trajectory. Loan portfolio composition shifts—especially relative contributions between CRE versus residential mortgage originations—will reflect management’s response to regional economic conditions as well as interest rate cycle influences shaping borrower demand patterns [S3].

Progression of the authorized stock repurchase program remains a barometer of confidence communicated by leadership regarding intrinsic valuation assessments coupled with expected capital adequacy under stress scenarios; any material acceleration or suspension will signal notable shifts in corporate capital strategy balance between shareholder returns and growth reinvestment priorities [S3][S17].

Digital channel adoption rates reported velocity of new account openings or active user increases will offer tangible cues about competitive positioning gains especially among younger consumers or SMEs favoring seamless fintech interfaces combined with bespoke advisory service inclusions.

Dividend policy consistency will be monitored as dividends depend on upstream payments from Primis Bank subject to regulatory limits emphasizing sustainable payout ratios congruent with earnings retention needs supporting organic growth funding requirements.

Management may issue updated guidance either formally during upcoming quarters or implicitly via investor presentation materials released periodically that elucidate shifts in strategic priorities addressing emerging risks or capitalization outlook adjustments disclosed contemporaneously with earnings releases or corporate events [S3].

Financial Profile: Capital Adequacy and Liquidity at Quarter-End

As of March 31, 2026, cash and cash equivalents totaled approximately $159.9 million providing a solid liquidity cushion vital for routine operational flexibility including loan funding requirements or contingencies arising from collateralized loan commitments or other contingent obligations per regulatory expectations [F1].

No material long-term debt commitments were highlighted restricting debt capacity; this prudent structural stance allows prioritization of organic growth funded principally through retained earnings supplemented judiciously by authorized common stock repurchases when accretive under defined price parameters [S2][S17].

In aggregate these capital adequacy metrics underpin Primis’ capability to pursue disciplined lending growth calibrated against prevailing Mid-Atlantic economic conditions without compromising statutory thresholds crucial for operational continuity.

Disclaimer: This analysis is based solely on publicly available SEC filings dated through May 8, 2026 ([S2], [S3], [S1]) supplemented by current companyfacts data ([F1]) as interpreted herein. It does not constitute investment advice or recommendations but aims to provide an informed perspective on business fundamentals rooted in evidenced disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments