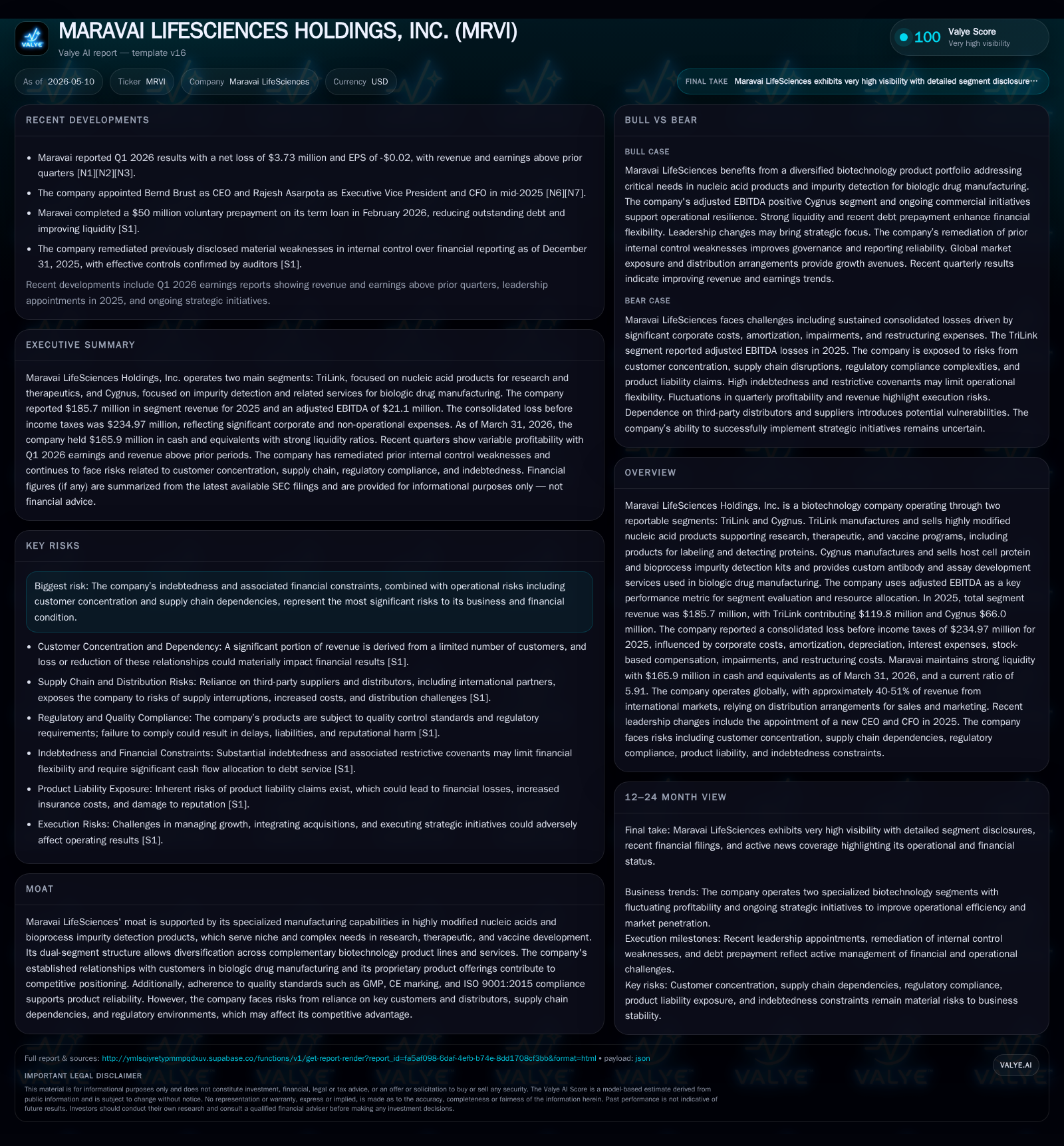

Maravai LifeSciences Faces Profitability Challenge Amid TriLink Segment Headwinds and Debt Constraints

Recent quarterly results reveal operating losses driven by TriLink segment weaknesses, highlighting capital structure pressures and risk amid competitive biotechnology markets.

Maravai LifeSciences Holdings, Inc. reported a challenging first quarter in 2026 with continuing adjusted EBITDA deficits in its TriLink segment despite solid contributions from Cygnus, which underscores structural demand shifts in nucleic acid manufacturing. The company's dual-segment business model offers diversification but faces margin pressures and customer concentration risks that complicate growth prospects. A sizable debt load and restructuring costs constrain financial flexibility, while competition from larger biotechnology firms and regulatory factors add execution risk. Monitoring segment revenue trends, cost management effectiveness, and debt servicing capacity will be critical in assessing Maravai’s path toward sustainable profitability and market relevance.

Recent Operating Update: Q1 2026 Performance Highlights

Maravai LifeSciences Holdings filed its latest 10-Q on May 8, 2026 ([S2]), delivering its first-quarter results that underscore persistent profitability issues despite incremental operational improvements. Segment revenues now total approximately $185.7 million for full-year 2025 as per the previous annual report ([S1]). However, the company reported continued adjusted EBITDA losses dominated by the TriLink segment’s performance drag. Cash balances remain robust at $165.9 million with total debt around $242.9 million as of March 31, 2026 ([F1]), positioning Maravai with a net debt level near $77 million but within manageable liquidity parameters reflected by a strong current ratio of 5.91.

The Q1 earnings call transcripts ([N1], [N2]) reinforce that while Cygnus maintains stable contribution margins through its bioprocess impurity detection kits, the TriLink segment faces demand fluctuations linked to vaccine program commercialization cycles and R&D spending volatility amidst evolving pandemic response frameworks.

Business Model Overview

Maravai operates through two synergistic segments:

TriLink: This segment focuses on highly modified nucleic acid products tailored for research, therapeutics, vaccine development programs (notably mRNA vaccines), and labeling tools used in protein detection assays within cell and tissue biology. These products are typically bespoke or semi-customized life science reagents requiring sophisticated manufacturing processes conforming to GMP standards.

Cygnus: Provides host cell protein detection kits, impurity profiling tools critical for biologics safety testing, viral clearance prediction technologies, along with custom antibody production and assay services integral to biologic drug manufacturing workflows.

Revenue derives principally from established pharmaceutical clients outsourcing specialized raw material needs or bioprocess analytics components vital to their drug development pipelines ([S10]). Pricing is influenced by complexity of product customization, volume contracts for commercial vaccine production (especially CleanCap® technology), and service-level agreements for bespoke antibody-based solutions.

Management measures segment health via adjusted EBITDA to exclude non-operational noise such as amortization or restructuring costs ([S22]). The dual-segment structure insulates Maravai somewhat from cyclicality inherent in biopharma R&D budgeting; Cygnus delivers defensive revenue streams concentrated around validated biologics quality control needs.

Industry Structure & Competitive Position

Maravai competes in a fragmented yet intensely competitive biotech specialty reagents market where numerous large-cap pharmaceutical suppliers coexist with niche innovators ([S23]). Established competitors often leverage scale advantages through expansive product portfolios enabling cross-selling bundles at lower per-unit costs—a challenging proposition for Maravai given its narrower focus.

Despite this competitive pressure, Maravai's core moat lies in proprietary manufacturing technologies underpinning highly modified nucleic acids (TriLink) and advanced impurity detection kits (Cygnus), buttressed by strict quality accreditations like ISO 9001:2015 certification and CE marking ensuring global regulatory acceptance ().

Critical differentiation stems from its ability to deliver complex biologics-grade reagents that meet rigorous clinical-grade purity specifications—a barrier not easily overcome by less technically equipped peers. Longstanding relationships with pharmaceutical developers entrenched through custom assay capabilities further defend market share but expose dependency risks.

Growth Drivers

- Expansion Within Biologics Manufacturing: Cygnus stands to benefit from accelerating adoption of host cell protein detection mandates globally as biologics penetration rises; customizable antibody services offer cross-sell opportunities into new therapeutic modalities.

- Emerging Therapeutic Nucleic Acid Demand: TriLink's portfolio aligns with growing investment in RNA therapeutics beyond vaccines—targeted gene therapies requiring chemically modified oligonucleotides could unlock new high-margin revenue streams.

- Strategic Acquisitions & Partnerships: Management has signaled intent to pursue bolt-on acquisitions enhancing novel reagent capabilities or geographic reach; successful integration would expand TAM exposure.

- Cost Rationalization Efforts: The ongoing organizational restructuring aimed at >$50 million annualized savings initiated in mid-2025 ([S26]) intends to improve adjusted EBITDA margins via workforce reduction (~25% cut) and operational efficiencies.

Risks & Constraints

- Financial Leverage: Total indebtedness restricts operational flexibility; interest expense pressures reported at $27 million annually limit reinvestment capacity [F1]. Debt covenants impose constraints on dividends, acquisitions, or asset disposals ([S20]).

- Customer Concentration & Payment Risk: A limited number of major customers constitute a significant portion of revenues; delayed payments or loss of key contracts could materially stress cash flows ([S19]).

- Dependency on Regulatory & Clinical Trial Activity: Shifts in FDA policies or reduced funding in clinical stages can dampen demand for research reagents outsourced to TriLink ([S11], [S18]).

- Competitive Innovation Pressure: Larger rivals' R&D budgets may outpace Maravai's technology development efforts risking product obsolescence if newer modalities gain traction faster ([S23]).

- Supply Chain Vulnerabilities: Reliance on specific raw material suppliers heightens risk; disruptions may impact timely fulfillment.[S11]

- Execution Risk Related to Restructuring: Workforce reductions could affect morale and productivity potentially limiting responsiveness to market opportunities or customer support demands ([S26]).

- Impairment Charges Impact Profitability Perspective: Significant goodwill impairment recorded ($68.7 million in 2025) signals prior acquisition overhang challenging asset value realization.[S22]

What to Watch Next

- Quarterly revenue splits between TriLink and Cygnus segments for signs of stabilization or acceleration post restructuring.

- Margins improvement trajectory driven by cost-cutting completion timelines announced last year.

- Cash flow generation relative to interest obligations indicating debt service sustainability.[F1]

- New or renewed contracts reflecting expanded penetration into emerging nucleic acid therapeutic markets.[N2]

- Progress toward strategic acquisitions or alliances enhancing technology breadth.[N3]

- Regulatory developments affecting client R&D budgeting impacting order volumes.[S11]

- Workforce attrition metrics post restructuring influencing operational resilience.

Financial Profile Summary (Latest Quarter)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $166mm | |

| 2026-03-31 | ||

| Total debt | $243mm | |

| 2026-03-31 | ||

| Net debt | $77mm | |

| 2026-03-31 | ||

| Current assets | $252mm | |

| 2026-03-31 | ||

| Current liabilities | $43mm | |

| 2026-03-31 | ||

| Current ratio | 5.91x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period End |

|---|---|---|

| Cash & Equivalents | $165.9 million | |

| 2026-03-31 | ||

| Total Debt | $242.9 million | |

| 2026-03-31 | ||

| Net Debt | ~$77 million | |

| 2026-03-31 | ||

| Current Assets | $251.7 million | |

| 2026-03-31 | ||

| Current Liabilities | $42.6 million | |

| 2026-03-31 | ||

| Current Ratio | 5.91 | |

| 2026-03-31 |

The balance sheet displays ample current assets coverage yet elevated gross leverage presents refinancing risks amid tight credit markets ([F1], [S2]). Operating losses continue to weigh on equity returns with operating income at -$215 million for FY2025 reflecting restructuring costs and goodwill impairment charges.[F1] Historical operating losses underline the need for sustained operational turnaround effectiveness.

This analysis summarizes recent public filings of Maravai LifeSciences Holdings, Inc., focusing on operational developments without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments