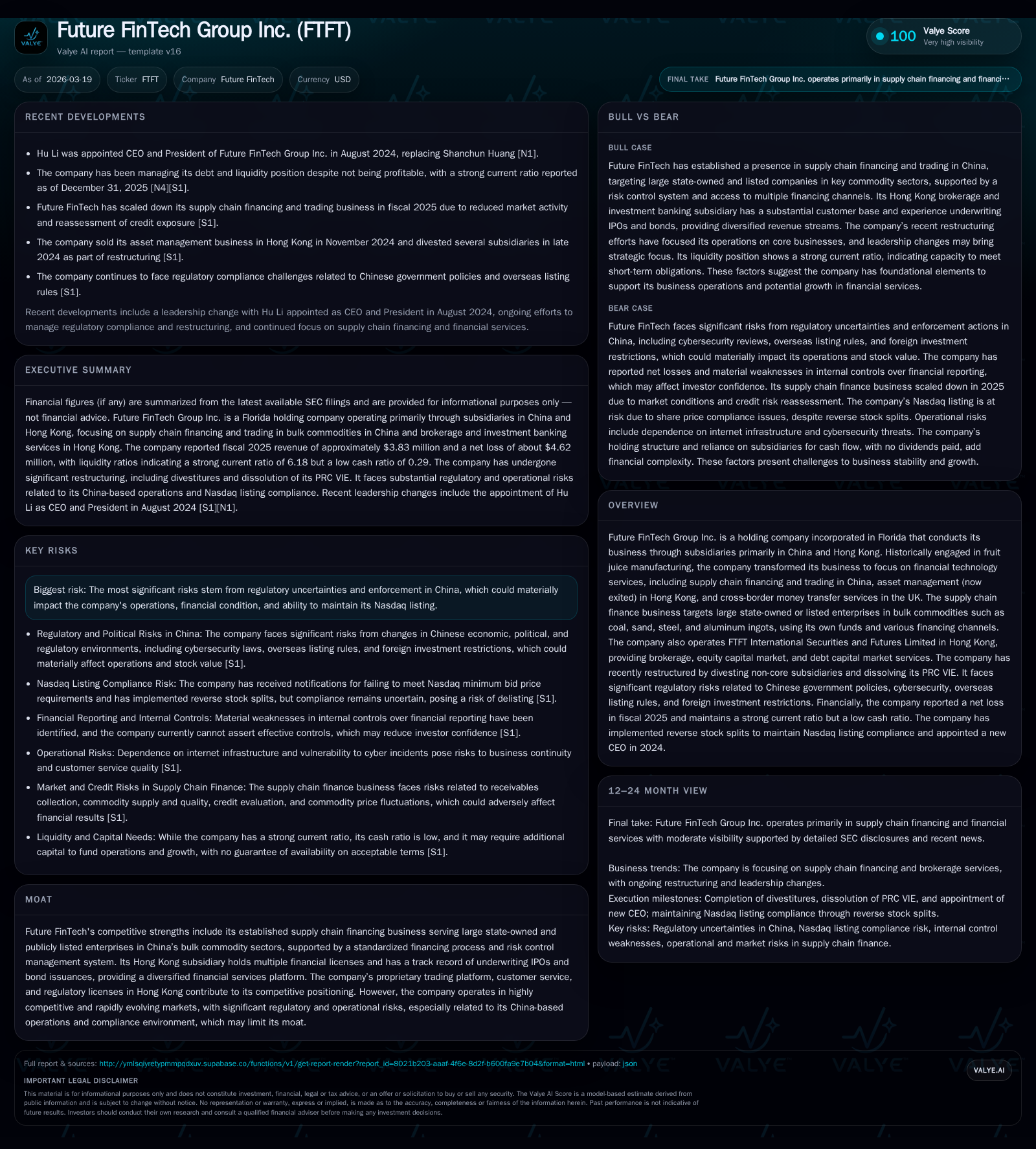

Future FinTech Group’s Strategic Shift Challenges Profitability Amid Competitive and Regulatory Pressures

The company’s transformation from fruit juice manufacturing to fintech services highlights growth ambitions constrained by operational losses and regulatory risks.

Future FinTech Group Inc. has transitioned from fruit juice production to focus on supply chain financing, brokerage, and cross-border fintech services targeting China and Hong Kong. Revenues rebounded strongly in 2025 following prior declines amid business restructuring. Despite this, the company continues to face significant operating losses driven by scaling down commodity trading and investment in new segments. Its brokerage and investment banking operations in Hong Kong, alongside nascent listing readiness consulting services, represent growth opportunities but operate in highly competitive and regulated environments. The firm maintains a solid liquidity position with positive free cash flow, yet ongoing legal issues and regulatory uncertainties pose challenges to near-term performance and strategic execution.

Historical Performance and Business Transformation

Future FinTech Group Inc., originally a fruit juice concentrate manufacturer in China, has repositioned itself as a holding company focused on financial technology services across China, Hong Kong, and the UK ([S1], [S4]). The shift was driven by rising production costs and environmental regulations impacting its original beverage business. The company divested non-core subsidiaries including asset management operations in Hong Kong (sold late 2024) and various digital finance entities in the U.S., while dissolving its PRC variable interest entity subsidiary after minimal revenue generation since 2021 ([S21], [S23]).

Financially, revenues declined sharply during the transition—from $23.9 million in 2022 to $2.2 million in 2024 during scaling down supply chain finance due to weaker bulk commodity markets and credit reassessments ([F1], [S4])—before rebounding by nearly 77.5% to about $3.8 million in fiscal year 2025 ([F1]). Operating income remains deeply negative at around a $34 million loss annually, reflecting restructuring charges and challenges establishing new revenue streams ([F1]). Net income improved from an extreme loss of over $32 million in 2024 to a loss near $4.6 million in 2025 ([F1]).

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | OpInc ($mm) | Capex ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 4 | -5 | -34 | 3720 | +77.5% | +86.0% |

| 2024 | 2 | -33 | -34 | 34056 | -93.8% | +2.1% |

| 2023 | 35 | -34 | -24 | +46.0% | -164744.0% | |

| 2022 | 24 | 0 | -17 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -10.5 |

| 2024 | -227.9 |

| 2023 | -76.5 |

| 2022 | 0.0 |

Source: SEC companyfacts cache [F1].

Revenues sharply declined through early transition years then rebounded slightly; persistent operating losses reflect restructuring impact.

Business Segments: Current Operations

Supply Chain Financing & Trading

This legacy segment focuses on working capital financing around bulk commodities including coal, steel, sand, and aluminum ingots for large state-owned or publicly listed enterprises such as subsidiaries of China Datang Corporation ([S4], [S5]). The company employs its own funds combined with bank loans and factoring facilities structured via purchase-sale agreements while managing delivery logistics.

Despite implementing standardized risk controls—including customer screening favoring high-credit enterprises—and operational efficiencies through process digitalization ([S7], [S25]), subdued upstream demand and a challenging infrastructure environment have suppressed revenue from this segment making it immaterial as of late 2025 ([S4]). Market uncertainty combined with intensified competition from larger players with deeper capital bases clouds prospects for scale expansion ([S9], [S13]).

Brokerage and Investment Banking Services: FTFT International Securities

Acquired in late-2023 as Alpha International Securities (Hong Kong) Ltd., renamed FTFT International Securities & Futures Ltd., this unit holds licenses for securities trading (Type 1), futures contract trading (Type 2), and securities advisory (Type 4) granted by Hong Kong’s Securities & Futures Commission ([S16], [S22]). It offers retail online brokerage for Hong Kong and U.S. equities via partnership arrangements; underwrites Hong Kong IPOs—participating in at least 29 since acquisition—and facilitates U.S. dollar-denominated bond issuances for Chinese issuers.

This segment benefits from advanced proprietary trading platforms serving over 60,000 customer accounts providing diversification beyond supply chain finance. Nonetheless intense competition exists from major global financial institutions offering broader service suites including commercial lending or margin financing which FTFT currently does not provide ([S9], [S11]). Market gains depend on technological differentiation and client experience amid pricing pressures.

Listing Readiness & Preparatory Consulting Services

Launched recently through Future FinTech (Hong Kong) Limited along with a limited-operating PRC subsidiary specializing in corporate governance consulting for private companies preparing for public listings ([S17], [S25]). Revenue contribution was nominal ($135K recognized for full year 2025), consistent with early development stage ([S25]). Regulatory ambiguity regarding licensing classification exposes this segment to execution risk if authorities require additional approvals or impose restrictions ([S17]). Growth depends on market uptake alongside evolving regulations.

Capital Allocation & Financial Position

Future FinTech maintains conservative liquidity with cash & equivalents exceeding $2.3 million versus current liabilities near $8.2 million yielding a current ratio above six—indicative of short-term solvency stability ([F1]). Capital expenditures remain minimal (~$3.7K in fiscal year 2025), reflecting restrained investment outside operational needs; this conservative spending contributed to positive free cash flow approximated at $2.7 million last year derived from operating cash flow less capex ([F1]). Despite these strengths the company posts negative return on equity near -10%, consistent with net losses relative to shareholder equity around $44 million at year-end 2025.

Strategic disposals include selling NTAM asset management for approximately HK$2.4 million (~$300K USD) due to unattractive returns linked to high labor costs and sluggish Hong Kong capital markets ([S23], [S27]). Other divestitures include U.S.-based digital finance subsidiaries associated with legal judgments impacting cash flow ([S23]).

Risks: Regulatory Environment & Competition

Key challenges include navigating China's opaque regulatory landscape where policies can abruptly affect overseas-listed firms like FTFT ([S6], [S19], [S21]). The dissolution of the PRC variable interest entity reflects limited activity post-COVID disruptions ([S21], [S23]). Cybersecurity threats raise compliance costs and risk disrupting transaction systems critical for customer trust ([S14], [S26]). Competition is intense against larger financial institutions with diversified product portfolios including lending products absent at FTFT that pressure market share particularly in brokerage services ([S9], [S13]).

Legal contingencies persist given class actions related to prior accounting practices settled partially via SEC fines exceeding $1.6 million requiring ongoing internal control reviews imposed since mid-2023 increasing governance expenses ([S19]). These proceedings may divert management focus despite adequate reserves.

Outlook: Growth Prospects & Monitoring Points

While explicit forward guidance is not provided post-2025 filings, key milestones include monitoring integration progress of FTFT International Securities’ underwriting mandates alongside client account growth; regulatory developments within China’s evolving fintech framework; and whether listing readiness consulting scales materially beyond initial revenues signaling strategic diversification.

Economic headwinds or recessionary pressures plus continued commodity sector challenges could impede supply chain finance recovery curtailed last fiscal year ([S4], [S18], [S28]). Pricing pressures threaten margin sustainability pushing FTFT toward innovation-dependent differentiation strategies.

Future FinTech stands at a pivotal juncture transitioning from manufacturing toward diversified fintech solutions targeting industrial clients alongside financial customers across jurisdictions. Recent results highlight structural adjustment pains manifesting through deep losses despite improving revenues; cautious optimism hinges on legal resolution progress coupled with successful adaptation amid tightening external controls over China-linked fintech activities.

This analysis relies exclusively on publicly available SEC filings dated through March 18th, 2026 without extrapolation beyond reported data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments