Genesis Energy LP's Strategic Shift Amid Midstream Market Challenges

Analysis of Genesis Energy LP's operational restructuring and financial dynamics post-Alkali divestiture.

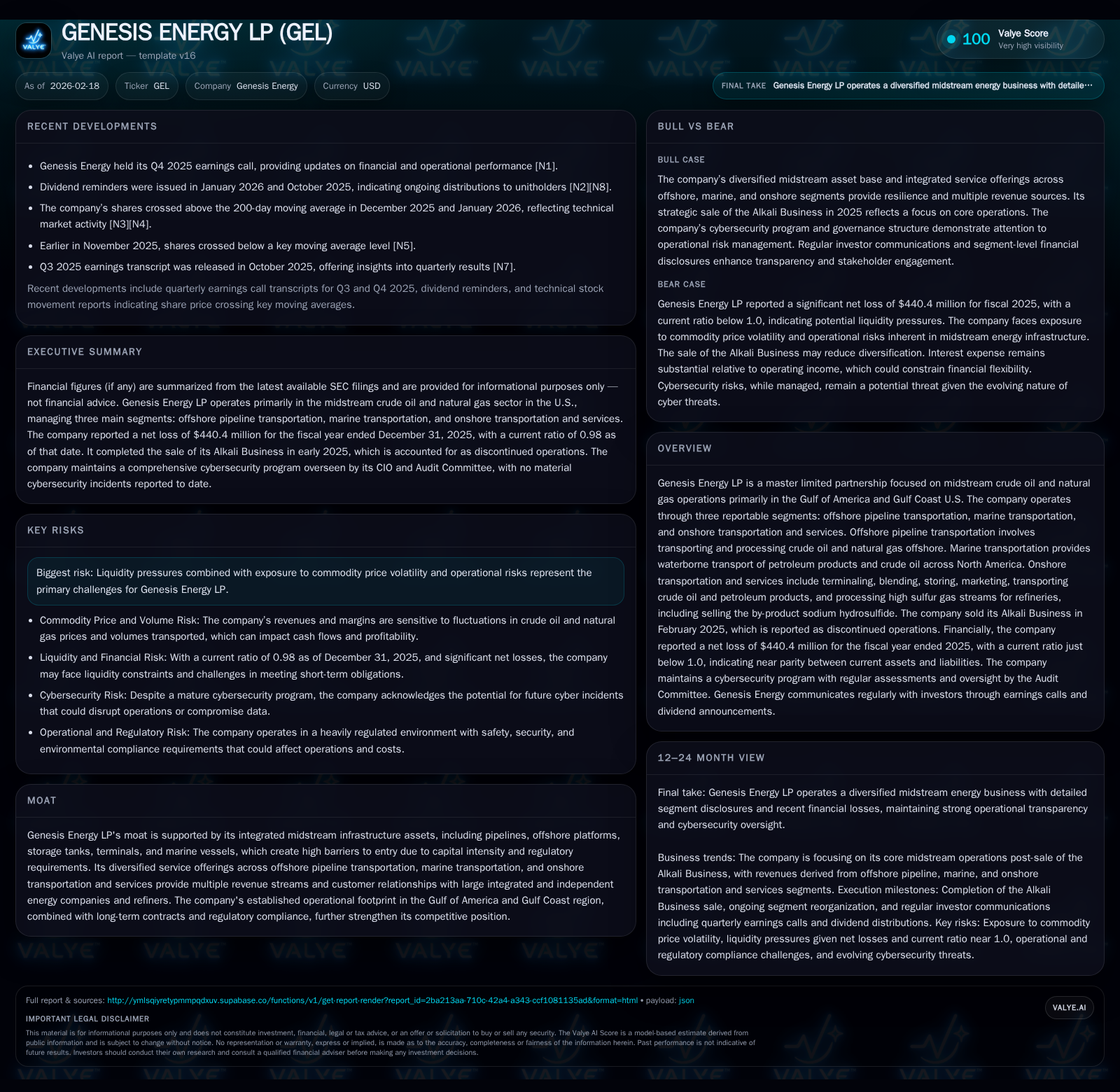

Genesis Energy LP, a master limited partnership operating integrated midstream assets in the Gulf regions, has recently undergone significant portfolio changes with the divestiture of its Alkali Business in early 2025. This strategic shift has materially impacted revenue composition and heightened financial volatility despite operating income growth. The company faces a challenging capital structure and liquidity profile while adjusting its capital allocation amid declining capex and absent share repurchases. Oversight of operational risks and commodity exposure is critical as it seeks to sustain cash flow amidst evolving contract durations and market conditions.

Integrated Midstream Legacy and Recent Operational Transformation

Genesis Energy LP has long established itself as an integrated midstream operator within the Gulf of America and Gulf Coast U.S., marked by its tripartite reporting segments: offshore pipeline transportation, marine transportation, and onshore transportation and services [N1][S1]. These segments collectively leverage capital-intensive infrastructure assets including pipelines, offshore platforms, storage terminals, and marine vessels that form significant entry barriers due to regulatory scrutiny and high fixed costs.

A watershed moment arrived in February 2025 when Genesis completed the divestiture of its Alkali Business—previously reported under discontinued operations—which had comprised processing high sulfur gas streams for refineries alongside sodium hydrosulfide by-product sales [N1][S1]. This move realigned the company’s portfolio deeper into its core transportation-centric activities, effectively trimming diversification but consolidating focus on fee-based midstream services.

This strategic rationalization reflects not only an asset portfolio simplification but also a reshuffling of revenue streams that historically buffered earnings against commodity price swings. The effective removal of the Alkali segment reduces exposure to chemical processing markets but elevates dependence on midstream throughput volumes and contract stability within the remaining segments.

Recent Financial Performance: Gains in Operating Income during Net Loss Pressures

In the FY2025 results period, Genesis demonstrated an intriguing financial dichotomy: operating income surged 21.2% year-over-year to $258.2 million while net income plunged into a pronounced loss of $440.4 million compared to a -$63.9 million loss in FY2024 [F1]. This divergence signals underlying profitability at operational levels offset by substantial non-operating expenses or impairments.

Analysis of XBRL-coded financials reveals that despite revenue declining modestly (a -4.3% YoY change), operating margin expansion underpinned positive operating income growth—a testament to cost containment or improved contract terms [F1]. However, the sharp deterioration in net income likely traces to one-time charges—potentially related to debt refinancing costs, asset impairment linked to divestiture, or write-offs from redemption of senior unsecured notes [N1][S3].

Operating cash flow exhibited pressure consistent with these developments, contracting 35.5% YoY to $252.8 million, reflecting a normalization from prior periods possibly inflated by working capital fluctuations or timing [F1]. Nonetheless, positive cash flow sustains operational funding needs albeit with less buffer.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -440 | 253 | 258 | 187 | -588.7% |

| 2024 | -64 | 392 | 213 | 587 | -154.3% |

| 2023 | 118 | 521 | 329 | 620 | +56.0% |

| 2022 | 75 | 334 | 315 | 424 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) |

|---|---|---|

| 2025 | 0 | 66 |

| 2024 | 0 | -195 |

| 2023 | 1044000 | -99 |

| 2022 | -90 |

Source: SEC companyfacts cache [F1].

Note: Data limitations restrict full year-by-year column completion; YOY calculations pertain primarily to latest years.

Segment Contributions and Shifting Revenue Drivers After Alkali Business Divestiture

Post-divestiture segment reporting shows Genesis refocused on three pillars: offshore pipeline transportation primarily servicing crude oil/natural gas flows offshore; marine transportation handling waterborne fuel oil, asphalt, heavy refined products distribution; and onshore transportation plus terminaling services including blending/storage operations along with sulfur services now consolidated into this segment following reclassification [S2][S17].

While precise segment revenues for FY2025 are not disaggregated here, MD&A commentary points to stable or improving fee-based contract contributions from offshore pipeline operations complemented by marine transport activity driven by North American refinery demand [N1][S17]. Onshore services gained relative weight given the removal of alkali operations but shifted toward crude oil logistics rather than chemical processing.

Within midstream parlance, this reshuffle heightens exposure to throughput volumes across pipelines and vessels while increasing reliance on fee-based agreements—where contract tenors and volume commitments underpin predictable segment margins—especially critical given commodity market volatility manifesting risk to volumetric throughput assumptions.

Liquidity Position, Debt Structure, and Covenant Adjustments

Genesis Energy's liquidity landscape reflects tight balances with current assets ($687 million) slightly below current liabilities ($699 million) yielding a current ratio close to 0.98 at fiscal year-end 2025 [F1]. Cash equivalents stood at just $6.4 million indicating limited short-term flexibility absent revolving facility access.

Debt composition showcases a senior secured credit facility maturing 2028 (originally $900 million reduced post-Alkali sale to $800 million) alongside over $3 billion in senior unsecured notes spanning maturities through early 2030s [S4][S8][S15]. Facility borrowings oscillated between roughly $60–70 million during H2 2025 Q3/Q4 quarters reflecting active liquidity management under covenant constraints.

Leverage ratio covenants have seen temporary relaxation amid transitional periods ending around late 2025—including increased maximum leverage thresholds (from 5.50x up to 5.75x) balanced against easing interest coverage minima—from 2.40x down to approximately 2x during fiscal quarters spanning late 2024 through most of 2025 [S8][S9]. Amendments allow additional cash netting against drawn debt if undrawn at period-end improving leverage metrics—a concession aligned with deleveraging post-disposition capital inflows.

Interest rate spreads on credit borrowings vary dynamically per quarterly recalculated leverage ratios: alternate base rate margins range roughly from 1.25%–2.50%, while Term SOFR-based loans carry premiums up to ~3.50%, underscoring sensitivity of financing costs to balance sheet leverage profiles [S6][S14][S16]. Such weighted average borrowing costs impose financial pressure in volatile midstream environments.

Capital Allocation: Capex Reduction, Dividend Policy, and Share Repurchase Trends

Strategically, Genesis has curtailed its capex outlays dramatically—the FY2025 amounting to approximately $187 million fell nearly two-thirds from over $587 million in the prior year—signaling focused capital discipline likely reflecting completion of major projects coupled with an emphasis on sustaining existing assets rather than expansion [F1][N1]. This reduction aligns with asset base pruning post-Alkali sale reducing reinvestment needs.

Despite shrinking capital expenditures, free cash flow remains positive but compressed; subtracting capex from operating cash flows yields roughly $66 million FCF in FY2025 versus stronger cash-flows in earlier years [F1]. With growing net loss pressure though, sustaining distributions or other shareholder returns could be challenged without operational improvement.

Dividend payment details follow standard MLP distribution cadence but explicit figures are scarce in tagged disclosures; however, ex-dividend notices confirm ongoing payouts without accompanying share repurchase activity—the latter showing zero buybacks in both FY24 and FY25 after modest repurchases preceding periods [N2][F1][S28]. Capital allocation appears squarely focused on maintaining liquidity buffers over equity returns amid uncertain earnings sustainability.

Emerging Risks: Commodity Volatility, Operational Challenges, and Cybersecurity Measures

Commodity price gyrations impart direct impacts on midstream firm fees linked to throughput volumes; lower barrel counts squeeze margin potential notwithstanding fee-based contracts often featuring minimum volume guarantees or escalators .[F1]

Operational risks inherent in offshore platform maintenance plus marine vessel safety protocols demand rigorous compliance with maritime regulations enforced by the U.S. Coast Guard under MTSA standards alongside pipeline security mandates overseen by TSA directives [S1].

Cybersecurity is robustly managed via network segmentation designed for industrial control environments plus layered defenses combining continuous monitoring with scenario-based incident response drills—critical protections against escalating threats targeting pipeline infrastructure that could disrupt flows or data integrity [S1]. Vendor risk assessments supplement this posture ensuring supply chain cyber-resilience integral to enterprise risk frameworks overseen by Board Audit Committees.

Outlook Considerations: What Drives Future Cash Flow and Growth Prospects?

Absent explicit forward guidance beyond official filings or conference calls reviewed here [N1], key variables influencing Genesis’ trajectory include timing/mix of contract renewals across all core segments—as longer-term contracts offer visibility while spot-exposed agreements could amplify volatility.

Infrastructure investment opportunities may be constrained given slashed capex budgets unless opportunistic projects arise that enhance throughput capabilities or extend contract longevity at favorable yields.

Throughput retention represents another focal point; sustained crude oil production levels in Gulf regions alongside stable refining demand underpin volume flows essential for revenue robustness amid market fluctuations.

Capital structure maneuvering including covenant management will continue affecting financial flexibility particularly as maturing debt instruments require refinancing or repayment choices coordinated with market conditions.

Valuation Perspectives: What Investors Should Monitor Ahead

From an analysis standpoint without explicit ROE figures available within data tags nor direct valuation multiples disclosed here, key metrics for monitoring include free cash flow trends relative to net losses highlighting earnings quality alongside leverage ratio dynamics reflecting resilience under macroeconomic stress).

Close attention should be given to covenant compliance disclosures particularly as amended thresholds approach expiration dates post-September-2025 periods potentially impacting borrowing capacity or cost structures.[S9]

Shifts in segment margin contributions influenced by evolving revenue mix post-divestiture will further inform profitability assessment while observing capex reacceleration signals may indicate renewed growth appetite addressing midstream competitive pressures.

Overall stewardship of liquidity reserves amid sustained distribution commitments remains pivotal for balanced stakeholder confidence as Genesis navigates a complex midstream landscape reshaped substantially since early-2025.

Disclosure: This analysis reflects information available as of February 18, 2026 based on filed SEC documents (10-K/10-Q/8-K), recent earnings call transcripts, company reports and Valye News proprietary sector knowledge without extrapolative assumptions beyond cited facts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments