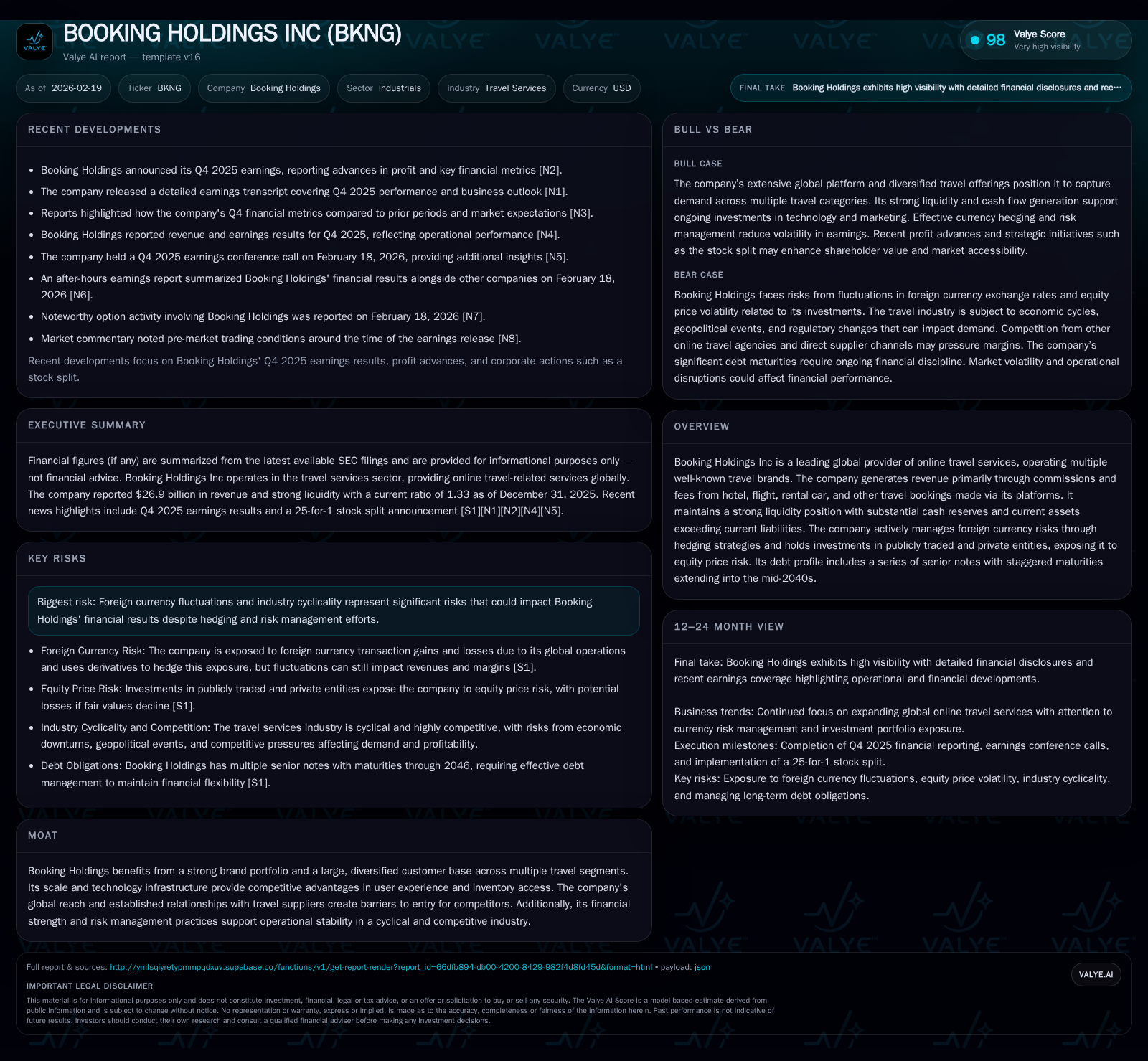

Behind Booking Holdings' Surge: Revenue Gains and Redeploying Capital

Booking Holdings exhibits robust revenue growth alongside disciplined capital returns amid currency risk management and evolving travel market dynamics.

Booking Holdings Inc. has demonstrated impressive year-over-year revenue acceleration driven by strong demand across its diversified travel platforms, contributing to a 13.4% revenue increase in fiscal year 2025. Operating income expanded nearly 17%, supported by efficient capital expenditure control and favorable operating cash flow generation. The company actively manages foreign currency risks through sophisticated hedging strategies, mitigating margin volatility on a global scale. Capital allocation remains focused on significant share repurchases complemented by stable dividend payments, illustrating a commitment to shareholder returns while maintaining liquidity against a staggered debt maturity profile extending into the 2040s. Continued investment in technology infrastructure and supplier relationships fortifies its competitive moat within the highly cyclical travel services sector.

Historic Growth: Dissecting Booking’s Revenue and Profitability Surge

Booking Holdings has posted compelling financial momentum over the past four fiscal years through the end of 2025. Revenue climbed from $17.1 billion in FY2022 to $26.9 billion in FY2025—an aggregate increase reflecting a compound annual growth rate significantly above industry peers given ongoing recovery trends in global travel demand [F1]. Specifically, fiscal year-over-year (YoY) revenue rose by 13.4% from 2024 to 2025 alone, underscoring acceleration after pandemic disruptions.

Operating income exhibited excellent leverage expansion, growing by 16.8% YoY to $8.825 billion in FY2025 from $7.555 billion the prior year. This outpacing of revenue growth represents gainful cost controls and operating efficiencies achieved despite inflationary inputs that often challenge digital platform operators in travel services.

Operating cash flow mirrored this positive trend, increasing by nearly 13% YoY ($9.409 billion in FY2025 versus $8.323 billion in FY2024). Notably, capital expenditures (Capex) reduced sharply by approximately 25% YoY to just $322 million in FY2025, compared to a peak of $429 million in FY2024—a sign of disciplined capex investment prioritizing scalable cloud infrastructure upgrades without excess spend [F1]. This capital discipline combined with strong CFO conversion supports sustained free cash flow generation exceeding $9 billion.

Historical performance (annual)

| FY | Rev ($bn) | CFO ($bn) | OpInc ($bn) | Capex ($mm) | Rev YoY |

|---|---|---|---|---|---|

| 2025 | 26.9 | 9.4 | 8.8 | 322 | +13.4% |

| 2024 | 23.7 | 8.3 | 7.6 | 429 | +11.1% |

| 2023 | 21.4 | 7.3 | 5.8 | 345 | +25.0% |

| 2022 | 17.1 | 6.6 | 5.1 | 368 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Net, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($bn) | FCF ($bn) |

|---|---|---|---|

| 2025 | 1248 | 6.4 | 9.1 |

| 2024 | 1174 | 6.5 | 7.9 |

| 2023 | 10.4 | 7.0 | |

| 2022 | 6.6 | 6.2 |

Source: SEC companyfacts cache [F1].

Table Note: Net income series insufficient for current period analysis due to outdated last available data from FY2012.

Navigating Currency Swings: Risk Management and Impact on Margins

Given Booking Holdings’ multinational operations generating substantial transactional volumes across diverse currencies, foreign exchange (FX) risk materially affects reported earnings and margins [S1][S7]. The company employs sophisticated derivative instruments as tactical levers to hedge exposure on transactional balances denominated outside subsidiaries’ functional currencies.

A core element in currency risk mitigation is the strategic designation of portions of Euro-denominated debt as hedges of net investments in Euro functional currency subsidiaries—effectively managing translation exposure that arises from fluctuating EUR/USD rates over reporting periods [S1][S7]. This hedge accounting treatment stabilizes volatility in comprehensive income related to currency movements.

Nevertheless, transactional FX gains or losses persist driven by net asset fluctuations within these subsidiaries combined with second-order impacts from equity price changes linked to publicly traded or private entity investments held on the balance sheet; for instance, a hypothetical uniform -10% fair value change would have imposed approximately $60 million before-tax losses recognized in net income for fiscal year-end December 31, 2025.

The use of derivatives such as forward contracts and options also limit short-term exposure while granting flexibility amid adverse rate shifts—terms frequently referenced among travel services companies due to complex revenue recognition timing across global markets.

Future Growth Trajectory: What the Company’s Guidance and Market Signals Indicate

Although explicit forward-looking guidance specifics are limited outside quarterly conference disclosures [N1], commentary reveals targeted investments in technology that enhance user engagement via AI-powered personalization algorithms and connectivity features enabling multi-legged trip planning (connected-trip enhancements).

Management underscores expanding TAM (total addressable market) via channel diversification beyond traditional accommodation bookings—extending into ancillary segments like car rentals and experiences—which could incrementally foster top-line growth further if user penetration widens organically or through partnerships [N8].

These initiatives dovetail with continued enhancement of mobile platforms optimizing transaction velocity and customer retention programs embedded within loyalty ecosystems—a critical lever given fiercely competitive dynamics in online travel intermediaries where take rates are tight but volume scales exponentially.

Risks remain tied closely to macroeconomic sensitivities including consumer discretionary spending patterns affected by inflation pressures or geopolitical tensions disrupting cross-border tourism flows; however, structural positioning with diversified brands partially inoculates Booking from single-market downturns.

Capital Allocation Dynamics: Returns to Shareholders through Buybacks and Dividends

Capital stewardship reflects a clear strategic priority at Booking Holdings: maximizing shareholder value primarily via aggressive stock buybacks supplemented by consistent dividend distribution.

In fiscal year ending December 31, 2025, share repurchases totaled an estimated $6.44 billion while dividends paid reached roughly $1.25 billion—this preference signals management’s confidence deploying capital internally versus external M&A or excessive debt repayment given current favorable operational cash inflows [F1][S9][S10].

The buyback cadence described aligns with industry terms such as opportunistic repurchases'' wherein repurchasing activity is calibrated based on market valuation signals rather than mechanical fixed schedules; this dynamic approach enhances capital redeployment efficiency'' providing enhanced EPS accretion potential.

At the same time, free cash flow generation remains robust at over $9 billion annually (operating cash flow minus Capex), affording capacity to sustain these return policies without undue leverage expansion even amid escalating operational complexity post-pandemic recovery.

Conversely, approximate return on equity (ROE) calculated from last reported net income versus shareholders’ equity shows negative figures (-5.2%) driven primarily by negative equity attributable to cumulative share repurchases diminishing book equity levels substantially—a phenomenon not uncommon when buybacks materially reduce outstanding shares over time [F1].

Debt Maturity Profile and Liquidity Cushion: Balancing Leverage with Financial Flexibility

Booking Holdings maintains an extensive debt structure composed mainly of senior notes maturing across staggered intervals from near-term (2026-27) to long-dated maturities extending into mid-2040s [S3][S8][S11].

This debt laddering reduces refinancing risk concentration by smoothing out principal repayment schedules—key for sustaining borrowing cost competitiveness over credit cycles prevalent in global capital markets serving industrial sectors with volatile revenues.

Liquidity positioning appears solid with current assets totaling approximately $22.26 billion exceeding current liabilities at about $16.70 billion—yielding a current ratio near 1.33 which provides ample working capital buffer amid cyclicality inherent in leisure travel bookings especially around seasonal demand shifts [F1].

Available cash and equivalents stand robustly at nearly $17.2 billion evidencing strong internal funding sources supporting both operational needs and strategic initiatives without reliance on incremental external financing under typical conditions.

Technology Infrastructure and Market Position: Defending the Moat in Travel Services

Booking Holdings operates multiple recognized global brands whose scale grants significant network effects—the more consumers using its platforms increases inventory access bargaining power with suppliers while enhancing personalized recommendation engine efficacy through aggregated data analytics .

Proprietary technology underpins seamless user experience integrating hotel stays, flights, car rentals—all converging within single transaction flows minimizing friction typical among fragmented competitors lacking integrated supply chains or cross-segment loyalty programs.

Supplier relationships cultivated over years afford privileged access pricing along with priority product placement opportunities thereby deepening barriers for new entrants who would require substantial capital spend to replicate equivalent breadth across geographies.

Customer retention programs leveraging behavioral insights further reinforce stickiness—a crucial competitive edge considering low switching costs characteristic of digital travel marketplaces where consumers regularly compare offers yet reward convenience paired with trusted brand reputation.

What to Watch: Earnings Drivers, Potential Risks, and Emerging Opportunities

Key indicators heading into upcoming reporting periods include tracking how well Booking sustains margin expansion relative to top-line growth amidst uncertain FX landscapes; elevated volatility could compress operating leverage benefits if transactional hedges prove insufficient during abrupt currency moves [N7][S6].

Monitoring consumer travel demand normalization post-COVID remains essential given structural shifts including increased remote work trends altering traditional business-to-leisure trip ratios impacting overall booking patterns.

Emerging opportunities pivot significantly on harnessing AI capabilities powering next-generation search optimization plus tailoring bundled trip packages leveraging connected-trip frameworks discussed publicly which could unlock higher customer lifetime values if effectively monetized within brand ecosystem architecture [N8].

Geopolitical risks coupled with macroeconomic headwinds might induce episodic slowdowns especially affecting international inbound tourism segments where regulatory changes impose new compliance costs or restrictions—factors necessitating agile management response balancing innovation investment against prudent cost control.

This analysis synthesizes information available from public disclosures including SEC filings and recent earnings materials without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments