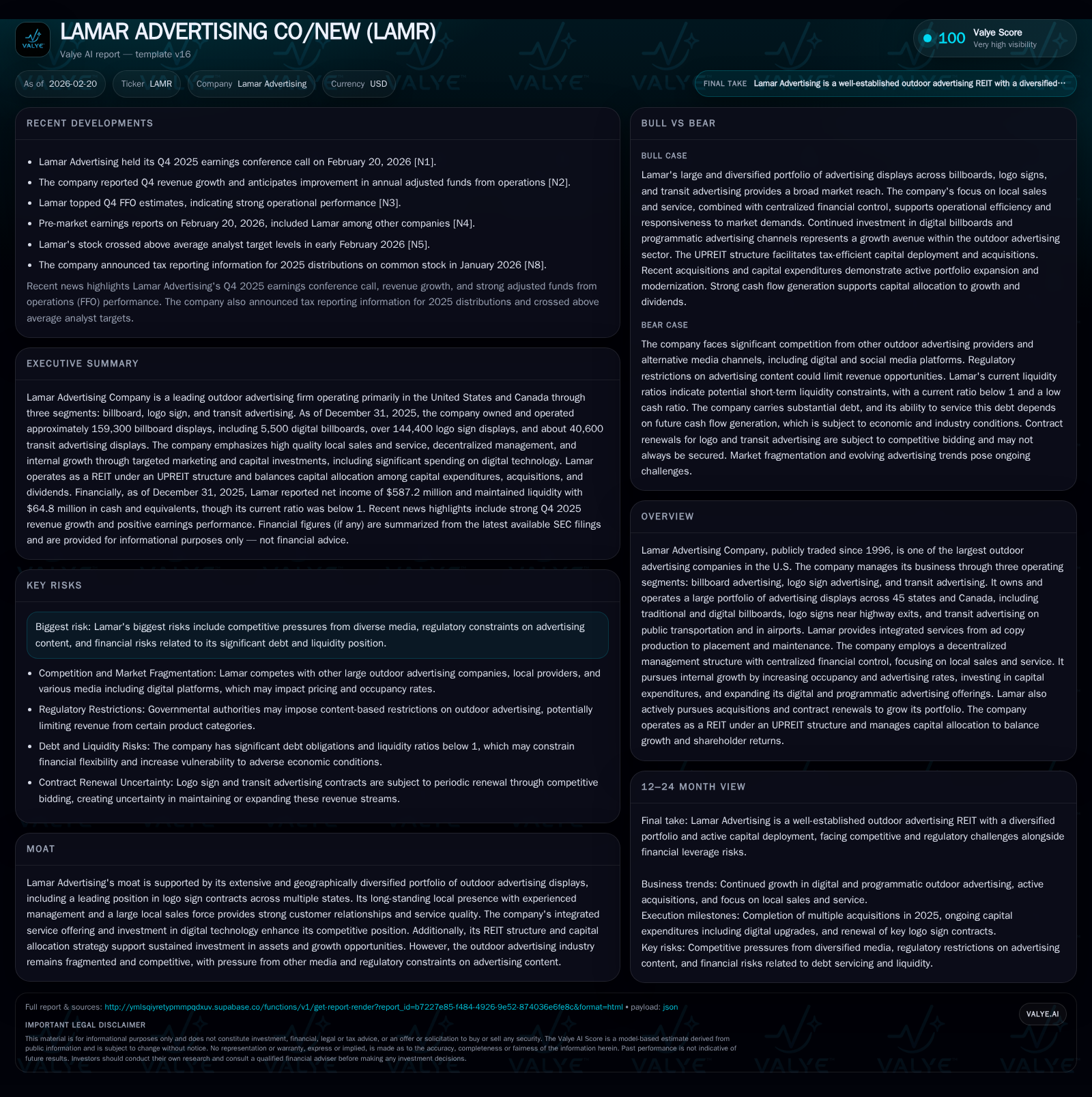

Lamar Advertising's Growth and Leverage Balance Tests Outdoor Ad Resilience

Lamar Advertising leverages a diversified portfolio and digital investments to drive growth despite debt-related constraints.

Lamar Advertising Company (LAMR) operates one of North America's largest outdoor advertising networks, spanning billboards, logo signs, and transit advertising. Its historical growth reflects targeted local sales efforts, significant capital investment in digital displays, and expansion of programmatic offerings, supporting strong operating income and net income gains in 2025. However, high leverage and debt covenant constraints pose financial risks, while competition from diversified media and regulatory pressures may limit future growth. The company plans to continue reinvesting in digital infrastructure and pursue contract renewals, with dividends sustained but share repurchases varying as part of capital allocation.

Business Overview and Historical Performance

Lamar Advertising Company (NASDAQ: LAMR) is a leading outdoor advertising firm with roots dating to 1902. It operates primarily across three segments: traditional/digital billboards; logo signage near highway exits; and transit advertising in bus shelters, airports, and public transportation vehicles. As of December 31, 2025, the company manages an expansive portfolio totaling roughly 360,791 displays spread over 45 U.S. states and Canada [S1][S4][S26].

Billboards (both static and digital) compose the largest segment by display count (~165,353 including ~5,500 digital units), while logo signs constitute over 148,400 units predominantly under long-term privatized state contracts. Transit advertising includes around 40,600 displays across more than 80 urban markets [S1][S19]. This geographic reach underpins Lamar’s diversified revenue stream.

Financially Lamar has demonstrated robust profit improvement over recent years supported by strategic capital deployment and operational execution [F1]:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 587 | 864 | 774 | 181 | +62.3% |

| 2024 | 362 | 874 | 532 | 125 | -27.0% |

| 2023 | 496 | 784 | 675 | 178 | +13.0% |

| 2022 | 439 | 782 | 578 | 167 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 157 | 158 | 683 |

| 2024 | 143 | 5 | 748 |

| 2023 | 128 | 6 | 605 |

| 2022 | 122 | 11 | 615 |

Source: SEC companyfacts cache [F1].

* Dividends data as of Q3 only; buybacks full-year available via narrative.

Operating income rebounded strongly by +45.5% in FY2025 after a dip in FY2024 likely impacted by macro uncertainties. Net income similarly rose sharply +62.3%. Operating cash flow was stable near $864 million despite inflationary cost pressures.

Capital expenditure jumped into the $180 million range driven by enhancements focused on upgrading existing digital assets—$90.9 million allocated solely for digital technology investments—which is nearly doubling spending compared to prior year [S7][F1]. The firm also pursues new construction initiatives internally to expand footprint.

Dividends increased steadily year-over-year with payout obligations around $157 million through Q3 alone in FY2025 (roughly aligned with full-year dividend trends). Notably, share repurchases surged markedly to $157.9 million in FY2025 from low single-digit millions previously indicating increased capital returned to shareholders during improving earnings environment [F1][S17].

Industry Positioning and Competitive Edge

Lamar's moat centers on:

- A vast asset base spanning multiple display types that combines scale with local market penetration.

- Long-term exclusive contracts for logo signs — leading provider of these privatized state programs holding majority of U.S. contracts.

- Expertise offered through an integrated service model covering design to placement fostering deep advertiser relationships.

- Strategic emphasis on digital transformation including programmatic out-of-home advertising where unsold digital inventory is monetized via partnerships [S1][S7].

Despite consolidation trends within outdoor ads, fragmentation persists industry-wide with several large players such as Clear Channel Outdoor and Outfront Media vying in overlapping markets [S9]. Competition also comes from broad media categories including television, online/social platforms, radio, print ads plus emergent nontraditional OOH media like mall kiosks or in-vehicle screens.

Advertisers evaluate competing media on impressions reach balanced against cost efficiency; Lamar highlights its relative cost-efficiency for geographically targeted exposure leveraging broad highway networks plus urban transit nodes [S9]. Regulatory constraints are an ongoing factor especially restricting certain product categories — e.g., tobacco ads have effectively been eliminated which impacts revenues in affected segments [S9][S29].

Future Growth Drivers and Constraints

Looking forward, several internal catalysts may propel Lamar’s growth trajectory:

- Incremental gains in billboard occupancy rates enhanced by focused local sales teams deploying targeted marketing initiatives.

- Pricing power enabling selective rate increases underpinned by core market demand resilience.

- Further geographic expansion after renewing or securing additional logo sign contracts — seven existing contract expiries loom in calendar year ’26 creating renewal risk but also opportunity [S27].

- Scaling programmatic buying channels which remain nascent (~2% current mix) yet promising for more dynamic inventory monetization [S7].

- Sustained commitment toward digitizing static assets converting them into higher-margin digital inventory allowing flexible ad rotations contributing elevated average selling prices [N3][S15].

However notable headwinds persist:

- Significant leverage constrains flexibility; over $3.4 billion debt stokes exposure to rising interest rates especially given variable-rate component tied to senior credit facilities and securitization programs [S11][S8].

- Covenant compliance risk given tight financial ratio requirements within debt agreements could restrict acquisitions or dividend ramp ups absent operating performance staying ahead [S6][S11].

- Competitive threats from increasingly sophisticated online marketing budgets shifting consumer attention away from traditional OOH mediums.

- Regulatory risk stemming from possible expansions of prohibited advertising categories or content restrictions affecting key customer segments.

- Contract renewal uncertainty concerning transit agreements awarded by municipalities which require high upfront capex costs before revenue generation [S26][S27].

Financial Profile & Capital Allocation Review

Lamar’s approximate return on equity based on trailing twelve months net income over shareholders’ equity stands impressively near 49%, highlighting efficient use of invested capital despite heavy leverage [F1]. Operating cash flows have been broadly stable north of $800 million annually supporting a solid free cash flow cushion after capex needs ($683 million estimated FCF in ’25).

The firm maintains REIT status requiring distribution of majority taxable income as dividends—this maintains strong dividend coverage though fluctuating depending on earnings quality and tax structures utilizing NOL carryforwards [S17]. Capital allocation has historically balanced reinvestment (capex skewed toward digital asset buildout), steady dividends that have grown year-on-year roughly following earnings progression, plus opportunistic buybacks which notably accelerated last year reflecting board confidence amidst profitability strength.

Leverage metrics—while precise debt ratios aren’t disclosed herein—are material enough to trigger operational constraints highlighted by company statements cautioning about liquidity vulnerabilities if profitability softens or if economic downturn curtails demand temporarily [S8][S11]. The company is actively managing capital structure but sensitivity to rate environment persists given large amount of floating-rate borrowings under credit facilities which today face rising SOFR-based rates [S8].

Operational Structure & Market Strategy Insight

Lamar employs a decentralized operational model where local management teams run day-to-day market activities supported by centralized finance functions node-wide optimizing compliance and scalability [S15]. This facilitates nimble responses tailored to local demographics but retains group-level oversight for reporting consistency.

The focus remains on multisource revenue growth internally rather than big acquisitions — maximizing yield via occupancy uplift alongside measured expansion of display inventories across all verticals plus technology upgrades that enable flexible creative cycling widely attractive to advertisers seeking effective urban commuter impressions.

Given seasonality common in outdoor demand spikes aligning with travel increases and consumer discretionary spending contexts such as holidays or sporting events, Lamar's diverse portfolio helps smooth volatility across regions mitigating concentrated downturn risks .

Key Milestones To Watch / Industry Context For Investors & Analysts (Analysis)

Absent explicit forward guidance beyond planned capital spend (~$186 million projected capex largely continuing digital commitment) and commentary about contract expiries next year [N3][S7], the following monitoring points provide useful forward context:

- Renewal outcomes for key logo sign contracts expiring mid-decade will materially influence display count stability.

- Programmatic channel adoption rates elevating above current ~2%, potentially signaling incremental margin upside.

- Macro-economic indicators impacting regional traffic patterns since vehicular exposure correlates closely to impression volume metrics driving pricing power.

- Interest rate trajectory stability affecting borrowing costs amid predominant variable-rate debt weightings.

- Potential regulatory developments around content policy affecting allowable advertiser categories particularly sensitive industries (e.g., cannabis legalization effects).

Disclaimer

This report aims to provide an objective analysis based on publicly available information including SEC filings and recent news items up to early February ’26 without offering investment advice or recommendations. Readers should consider this assessment as informational context regarding LAMAR ADVERTISING CO/NEW's business dynamics and financial profile within the outdoor advertising sector.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments