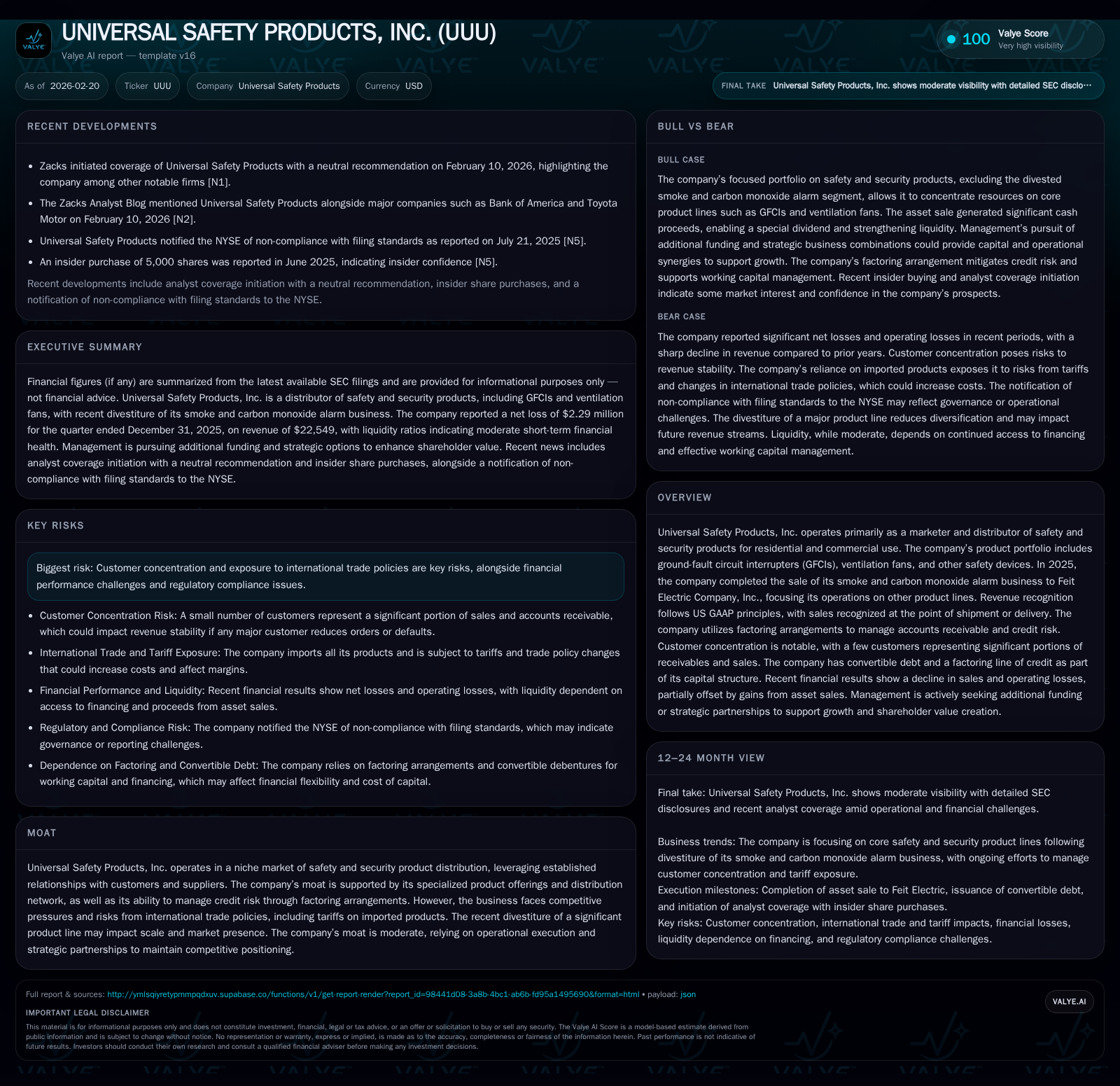

Universal Safety Products' Strategic Refocus Reduces Scale but Tests Profitability in 2025

The divestiture of smoke and CO alarms shrinks revenue base while credit management and capital structure adjustments shape near-term results.

Universal Safety Products, Inc. (UUU) experienced a sharp revenue contraction in the first nine months of fiscal 2025 following the sale of its smoke and carbon monoxide alarm business. This strategic divestment refocused the company on ground-fault circuit interrupters (GFCIs), ventilation fans, and other safety devices but also diminished overall scale and gross margins. The company’s moderate moat, based on niche product specialization and factoring arrangements to manage credit risk, faces pressure amidst competitive dynamics and customer concentration. Operational cash flow turned negative in FY 2025 despite a positive net income outcome for the prior fiscal year, with convertible debt issuance and factoring line usage impacting liquidity and capital structure. Monitoring the company’s efforts to improve operating efficiency alongside broader market acceptance of remaining product lines will be key going forward.

Historical Performance and Business Context

Historical performance (annual)

| FY | Rev ($mm) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2026 | ||||||

| 2025 | 24 | 500684 | -1048612 | 402049 | +18.4% | +226.5% |

| 2024 | 20 | -395790 | 604076 | -264805 | -10.3% | -154.9% |

| 2023 | 22 | 720411 | 1491943 | 972574 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2026 | |

| 2025 | 9.7 |

| 2024 | -8.0 |

| 2023 | 13.4 |

Source: SEC companyfacts cache [F1].

Universal Safety Products, Inc. reported revenues increasing steadily from roughly $19.5 million in FY2021 up to $23.56 million in FY2025 (year ending March), an increase of approximately 18.4% year-over-year [F1]. Operating income showed notable volatility, moving from a modest $69.7K gain in FY2021 to a peak near $972K in FY2023 before slipping into loss territory in FY2024 (-$264K), then recovering for FY2025 ($402K operating income). Net income reflected a similar pattern: losses through early years turning into positive $500K in FY2025 after swinging negative the previous year [F1]. This earlier growth was primarily driven by sales across multiple safety and security product lines including smoke alarms, carbon monoxide (CO) detectors, GFCIs, and ventilation fans.

However, during calendar 2025, Universal Safety Products strategically sold its smoke and CO alarm segment to Feit Electric Company, Inc., signaling a material refocus [S27]. This divestiture significantly impacted scale: net sales for the nine months ended December 31, 2025 shrank dramatically by approximately 73%, down to $4.61 million from about $17.34 million for the comparable period in the prior year [S27]. Gross margins fell from 23.7% during that prior period to just 19%, reflecting the loss of higher-margin products within that segment [S27]. Operating expenses remained relatively flat at around $4.32 million despite this sales collapse due partly to restructuring costs, incentive stock option charges (~$897K), reductions in workforce, and strategic planning efforts for merger alternatives [S27]. The latest reported quarter witnessed a steep operating loss exceeding $2 million and an even larger net loss of about $2.29 million concentrated mostly on non-cash items including derivative valuation changes on convertible debt instruments [F1][S27].

Customer Concentration and Receivables Management

The company operates with notable customer concentration risks: three customers accounted cumulatively for roughly 37% of trade accounts receivable as of December 2025 (13.7%, 12.8%, and 10.4%) although no single customer exceeded roughly 14% of quarterly sales recently reported [S4][S11]. Management mitigates some credit exposure via established factoring arrangements with Merchant Financial Group which allow borrowing against eligible trade receivables at up to 80%. However, usage under this factoring line declined sharply from over $2 million borrowed mid-year down to approximately $7,400 at fiscal year end December 31, 2025—a reduced dependence possibly reflecting tighter credit terms or collection efforts post-divestiture [S9]. The factoring line facilitates risk transfer but does not cover all risks as disputes or denied credits remain on Universal’s books.

Capital Structure: Convertible Debt and Liquidity Positioning

In August-September 2025, Universal Safety Products issued aggregate convertible promissory notes totaling $2.75 million at an effective interest rate of around 8%, structured with conversion options exercisable through late summer/fall 2026 at an approximately 20% discount to market price based on ten-day volume-weighted averages preceding conversion dates [S14][S24]. These notes had embedded derivatives requiring bifurcated accounting per ASC standards causing fair value adjustments recorded each period that influence reported earnings volatility—an expense totaling roughly $182K recognized over nine months ending December ’25 alone [S23][F1]. Post-quarterly filing developments saw partial conversion reducing outstanding convertible debt by ~$1.55 million exchanged into new shares effectively diluting equity but easing cash obligations somewhat [S26].

From a liquidity standpoint, proceeds from the sale of the smoke and CO alarm business generated approximately $4.5 million net cash inflow realized mainly during H1/FY2025 supporting ongoing operations despite negative operating cash flow trends later in the year [S12][S28]. The company also paid out a special dividend exceeding $2.3 million in late FY2026 Q3—a sizeable distribution amid operational stresses indicating possible shareholder return prioritization during transition phases or related strategic moves [F1][S26]. Current ratio stood at a healthy ~1.7x at latest quarter end balancing current assets near $5.5 million against liabilities around $3.2 million [F1], indicating sufficient short-term solvency excluding potential unpredictable demands.

Cash Flow Trends and Capex Profile

Operating cash flow reversed course sharply declining from positive ~$604K generated during FY2024 into a deficit exceeding one million dollars ($-1,048K) for FY2025 driven largely by working capital shifts timed with asset sales timing rather than core operating performance improvements [F1]. Capital expenditures were effectively nil during most recent years evidencing minimal reinvestment into fixed assets or manufacturing capacity consistent with its role as marketer/distributor rather than manufacturer [F1]. Thus, free cash flow dynamics remain tied closely to operational turnaround rather than capex cycles.

Future Growth Prospects

Post-divestiture Universal Safety Products is now concentrated on the marketing and distribution of GFCIs, ventilation fans, and safety devices aside from smoke/CO alarms previously held—the latter being historically significant contributors to top line revenue and gross margins [N1][N2][S27]. The success of these remaining product lines hinges upon sustaining strong supplier relationships (recent acquisition of select products from Eyston Company Ltd.), expanding penetration with existing customers while diversifying customer base beyond concentrated accounts to mitigate credit risk concentration effects documented as material historically [S7][S11].

Growth drivers could emerge from increased regulatory requirements enhancing demand for ground fault interrupters especially within residential/commercial renovation markets or ventilation solutions aligning with energy efficiency standards if effectively commercialized across broad channels including electrical distributors and manufactured housing sectors served indirectly through subsidiary Universal Electric Inc., formerly USI Electric Inc.[N2][F1][S21]. However technical product commoditization risks combined with tariff uncertainties on imported components may constrain margin expansion opportunities despite stable demand fundamentals noted across safety products generally {analysis}. Additionally, factoring reliance suggests potential liquidity constraints limiting aggressiveness in working capital-intensive growth scenarios without further capital infusion or strategic partnerships.

Forecasts and Milestones To Watch

While explicit forward financial guidance was not provided directly by management disclosures as per filings through February 2026 release dates, immediate events meriting close observation include progress on converting outstanding convertible notes scheduled for maturity by August/September 2026 potentially impacting capital structure stability post-conversion activity seen so far; updates on any further asset sales or acquisitions related to Universal DEFI LLC—the newly established subsidiary formed July ’25 yet inactive materially—which may signal directional shifts or growth initiatives beyond core distribution; continued trends in customer concentration metrics which remain elevated posing systemic risk if left unchecked; performance metrics relating to gross margin recovery or operational expense rationalization following strategic refocus documented alongside restructuring charges taken recently [N3][S26][S27].

Returns and Capital Allocation Summary

Return on equity approximates modest levels near 9.7% based on the most recent full fiscal year ended March ‘25 figures relative to equity balances just above $5M before subsequent share issuances diluted shareholders’ stakes accordingly [F1]. Dividends are non-recurring large special distributions rather than steady streams typical among mature industrials reflecting payout linked potentially more to asset-sale proceeds rather than sustained free cash generation capacity given negative CFO trending [$2.31M dividend paid late FY2026 Q3; F1][S26]. Buybacks have been absent historically aside minor repurchases years ago prior to recent restructuring efforts illustrating current emphasis is likely on deleveraging balance sheet via convertible note conversions plus maintaining liquidity buffers supported by factoring lines rather than returns-focused capital deployment.

Conclusion

Universal Safety Products embodies a classic mid-market distributor undergoing transition post major portfolio restructuring accompanied by heightened financial engineering via convertible debt issuance aimed at navigating liquidity needs amid episodic operational losses exacerbated by strategic realignment costs including deferred stock option expensing and severance-related provisions. Its niche moat anchored around specialized safety product distribution coupled with credit risk management through factoring offers moderate competitive insulation but still exposed notably to customer concentration pressures plus channel competition intensifying following exit from core smoke/CO alarm category which historically contributed disproportionately both revenue scale and gross margin resilience.

Market observers should carefully monitor execution efficacy particularly regarding expansion beyond incumbent customers using GFCIs/ventilation units while controlling overhead fixed expenses closely since leverage effects erode profitability quickly given lower absolute revenue base currently maintained vs peak historical volumes pre-divestiture; tracking convertible debt amortization schedules plus derivative valuation impacts will also be critical considering their meaningful influence on reported results unrelated directly to underlying operations.

Investors assessing Universal Safety Products may thus view fiscal ‘25 as a watershed representing reset/re-focus phase hinging heavily upon disciplined execution around monetizing residual product portfolios amidst constrained capital resources balanced against latent upside potential inherent in regulated safety device markets served.

This analysis is informational only and should not be construed as investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments