Figma’s Challenge to Innovation: Managing Growth While Integrating AI Across Design Workflows

Figma balances rapid expansion with deep AI integration and platform extensibility as it strives to sustain collaborative software innovation.

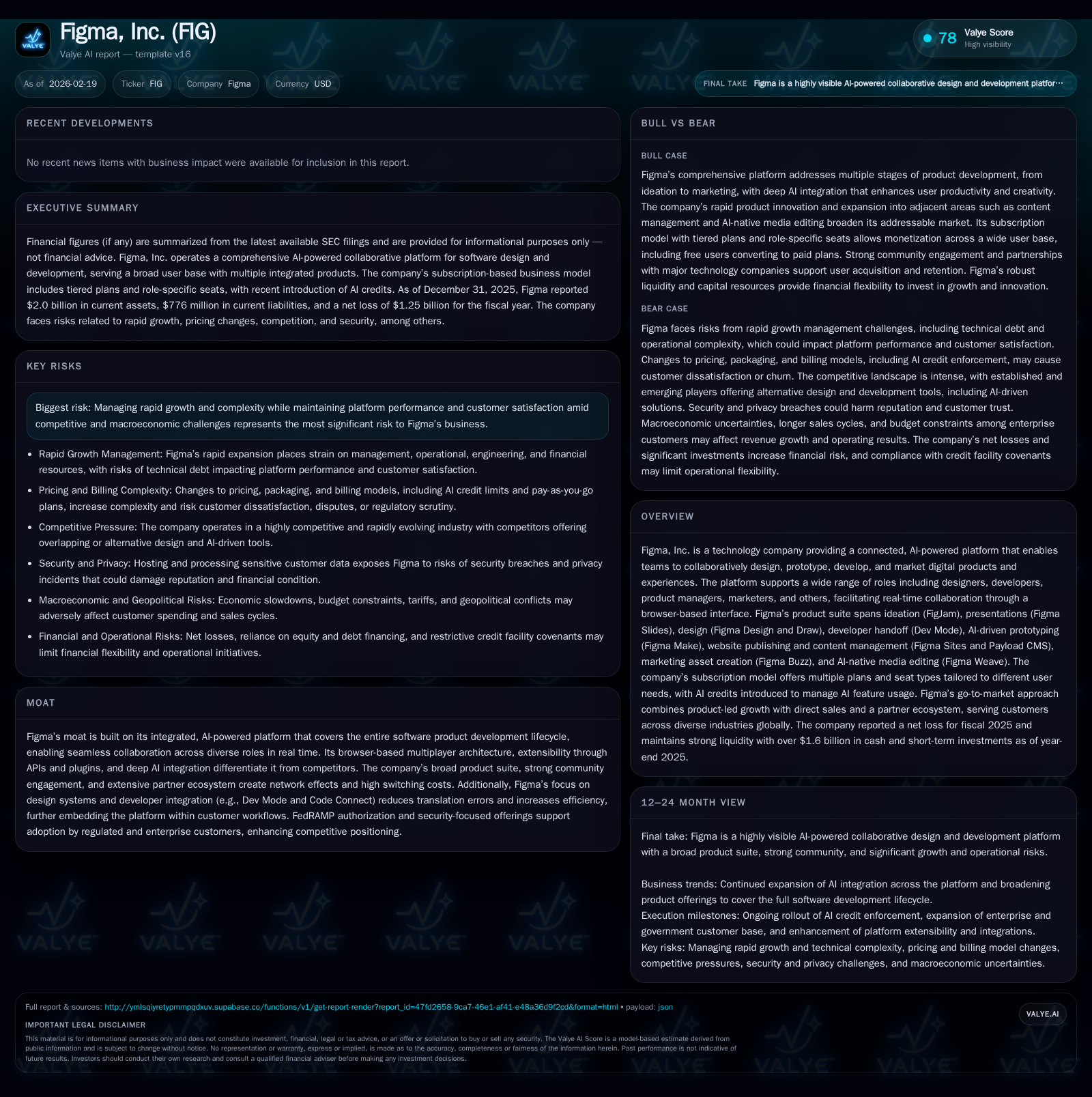

Figma, Inc. has emerged as a transformative force in digital product development by integrating AI and extensive collaboration tools within a browser-based platform that spans design, prototyping, development handoff, and marketing workflows. The company’s historical trajectory shows rapid revenue growth and workforce expansion juxtaposed against persistent operating losses reflecting aggressive investment in product innovation and scaling infrastructure. As its platform matures, Figma faces pressure to sustain growth amid intensifying competition and evolving customer demands, especially in monetizing AI enhancements. Capital management remains focused on sustaining cash flow through a revolving credit facility without returning capital via dividends or buybacks. Key milestones include the adoption pace of new AI-powered features like Figma Make and success in penetrating regulated enterprise markets supported by FedRAMP authorization.

Historical Growth Dynamics and Financial Performance Trends

Figma has surfaced as an influential player reshaping digital product creation through its connected collaboration platform that integrates design, development handoff, prototyping, content management, and marketing asset creation into a single browser-based environment. Historically, Figma's trajectory showcases rapid revenue scaling: according to recent SEC filings, annual revenues rose sharply from approximately $505 million in 2023 to $749 million in 2024, then surpassed $1.1 billion in 2025—an unequivocal demonstration of robust top-line momentum even though detailed revenue figures by year are disclosed only narratively rather than fully via XBRL data [S1][S2]. This rapid growth parallels an employee count nearly doubling from just over 1,000 at the end of 2022 to nearly 1,900 by December 2025 as the company bolstered teams across engineering, sales, marketing, and support functions.

Despite this scaling success on demand metrics and headcount buildout, Figma continues to report substantial operating losses that reflect its aggressive investment posture. Operating income loss widened from prior years with an approximate -$1.29 billion operating loss in FY2025 paired with a net loss near -$1.25 billion—the latter equating to a negative return on equity of about -82.8%, underscoring sustained reinvestment rather than profitability at this stage [F1]. Yet the company generated positive operating cash flow exceeding $250 million in FY2025 while maintaining relatively low capital expenditures (~$4.4 million), signaling strong core operations that are not yet translating to bottom-line profits due mainly to heavy R&D spending and go-to-market investments. The current ratio of ~2.58 further suggests comfortable liquidity buffers.

Historical performance (annual)

| FY |

|---|

| 2025 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Net, CFO, OpInc, Capex, Div, Buybacks, FCF, ROE%. Source: SEC companyfacts cache [F1].

Note: Revenue data is available only narratively; exact year-over-year comparisons are not possible from provided tags.

This historical profile presents Figma as an investment-stage company aggressively pouring resources into building a comprehensive suite while scaling usership significantly.

Evolution of Figma’s AI-Driven Product Ecosystem

Since its inception as a design tool empowered by real-time browser-based multiplayer collaboration, Figma has evolved into an expansive AI-powered platform encompassing stages of the software product lifecycle extending well beyond vector graphic design. Key modules such as FigJam for ideation whiteboarding; Figma Slides for presentations; Dev Mode facilitating developer handoff with direct code context; Figma Make enabling text-prompt-driven prototype generation; plus emerging products supporting website publishing (Sites CMS), scalable brand asset automation (Buzz), and native media editing with AI assistance now populate the offering landscape [S5][S6].

This breadth is complemented by sophisticated architecture: APIs enable plugin extensibility allowing customers to customize workflows by connecting designs directly with data systems or code repositories—vital for integrating disparate tools common in modern SaaS stacks. Moreover, FedRAMP authorization attained early 2025 facilitates regulated government customer adoption by meeting stringent compliance demands; such regulatory credentials underscore technical trustworthiness essential for large enterprise usage [S14].

Deep AI integration permeates these layers—from automation of repetitive UI design tasks within FigJam or Design products to agentic coding assistance woven into Dev Mode—shortening design-to-code cycle times while preserving fidelity. This implementation illustrates sector-native complexities surrounding multi-player web environments where latency control underpins collaborative effectiveness.

Sustaining Growth: Market Penetration and Platform Adoption Challenges

Despite impressive historical growth curves supported by word-of-mouth virality inherent to its collaborative model combined with direct sales targeting enterprise accounts, forecasting future momentum remains challenging amid a maturing market stage [S1][S2]. Competition spans entrenched incumbents boasting wider but more siloed offerings across design systems and application lifecycle management suites; alongside nimble startups leveraging novel AI models that compress workflows differently.

Further friction points include:

- Retaining diverse user cohorts beyond traditional designers—including developers now sizeable users thanks to Dev Mode—and non-design roles like marketers who increasingly leverage Buzz.

- International expansion complexity coupled with localization efforts amid evolving global data privacy regulations impose additional operational loads.

- Sales cycles lengthen especially for larger enterprises typical budget seasonality impacts billing recognition cadence.

- Pricing strategy recalibrations required due to differential usage patterns driven by newly introduced AI credits system launching enforcement in early 2026 constrains free generative AI usage without additional purchases [S16].

Management acknowledges expected deceleration in growth rates transitioning from hyper-growth toward broader market maturity where SaaS dynamics favor retention improvements alongside moderated net new customer acquisition rates.

Capital Management Underpinning Expansion: Cash Flow, Debt, and Investment Priorities

Financial stewardship reveals prudent liquidity management underscoring sustainability during aggressive scaling phases. At year-end 2025 unrestricted cash stood at approximately $403 million complemented by undrawn capacity on a $500 million revolving credit facility secured against company assets providing operational flexibility [F1][S4]. Notably the firm utilized up to ~$330 million on this revolver mid-2025 primarily for settling tax obligations linked to IPO-related restricted stock unit settlements but subsequently repaid portions using IPO proceeds—a testament to active balance sheet optimization [S7][S10].

Capital expenditures remain modest relative to overall cash flows—with FY2025 capex near $4.4 million outpaced substantially by net cash generated from operations ($251 million), resulting in positive free cash flow over $246 million indicative of scalable operational efficiency despite accounting losses [F1].

No dividends or share repurchases occurred over the period reflecting a capital allocation philosophy focused squarely on reinvestment aimed at sustaining innovation velocity and international coverage rather than shareholder distributions during nascent profitability horizons [F1].

Forecasting Milestones to Watch: Market Risks and Opportunities Ahead

While explicit forward guidance is limited per regulatory disclosures [N/A], investors should monitor adoption metrics of newly launched AI-centric modules such as Figma Make which promises automated prototype creation from simple text prompts—a potential catalyst enabling expansive use cases beyond traditional product teams.

Additionally critical is progress in deeper monetization strategies around AI credit management post roll-out phases starting March 2026 which introduces paid consumption plans reminiscent of usage-based pricing models now standard among generative AI platforms [S16].

Competitive landscape shifts warrant vigilance—especially moves by large integrated cloud vendors potentially bundling overlapping capabilities or startups innovating specific vertical workflows that might erode market share or depress pricing power.

Sensitivity also arises regarding macro headwinds including prolonged software budget caution among enterprises tied to geopolitical instability or inflationary pressures potentially impacting renewals or contract expansions [S9][S24]. These factors collectively shape a nuanced medium-term outlook balancing innovation potential against commercialization execution risks.

Strategic Positioning via Extensibility and Developer Integration

A defining moat lies in Figma’s multi-role collaboration environment bridging historically segmented stakeholders across design-to-code workflows via tightly integrated features such as Dev Mode coupled with Code Connect plugins which reduce translation errors between mockups and executable code—material efficiency gains highly prized by engineering organizations reliant on seamless handoffs [S6].

This ecosystem approach extends through robust APIs allowing firms to customize tooling landscape embedding Figma natively within broader CI/CD pipelines or project management dashboards enhancing stickiness through network effects where design artifacts become centralized system-of-record elements woven through product development lifecycles.

Such integration depth also supports dual acceleration strategies: top-down IT governance expanded via Governance+ add-ons supplementing security controls plus bottoms-up viral product adoption fueled through individual users championing platform engagement organically within teams—a vital mix given competitive pressures requiring both scale breadth and enterprise-grade trustworthiness.

Risks in Scaling Platform Performance and Customer Satisfaction

Underlying all ambitious scale-ups are substantial operational complexities especially when pioneering synchronized web-based multiplayer editing involving billions daily interactions globally requiring ultra-low latency responsiveness—a cornerstone for user satisfaction sensitive even to millisecond delays impacting creative momentum [S24][S1].

Balancing continuous feature enrichment—including expansive AI capabilities—with intuitive usability creates tension points risking either overwhelming novices or disappointing power users if poorly architected. Security vulnerabilities amplify risk profiles especially given high sensitivity around intellectual property housed within shared digital workspaces potentially targeted for breaches or phishing attacks necessitating sustained investments in cybersecurity hardening consistent with FedRAMP compliance efforts already underway. Failure modes related to integrating disparate third-party plugins heighten fault domains challenging seamless reliability central to premium pricing tiers offered mostly within large enterprises demanding strict SLAs. These operational risks interplay materially influencing renewal rates conversion curves thereby feeding back into financial health determinants fundamentally anchoring valuation narratives going forward.

Disclaimer: This report presents an analytical overview based exclusively on publicly available information without offering investment recommendations or price targets. The information herein should not be construed as financial advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments