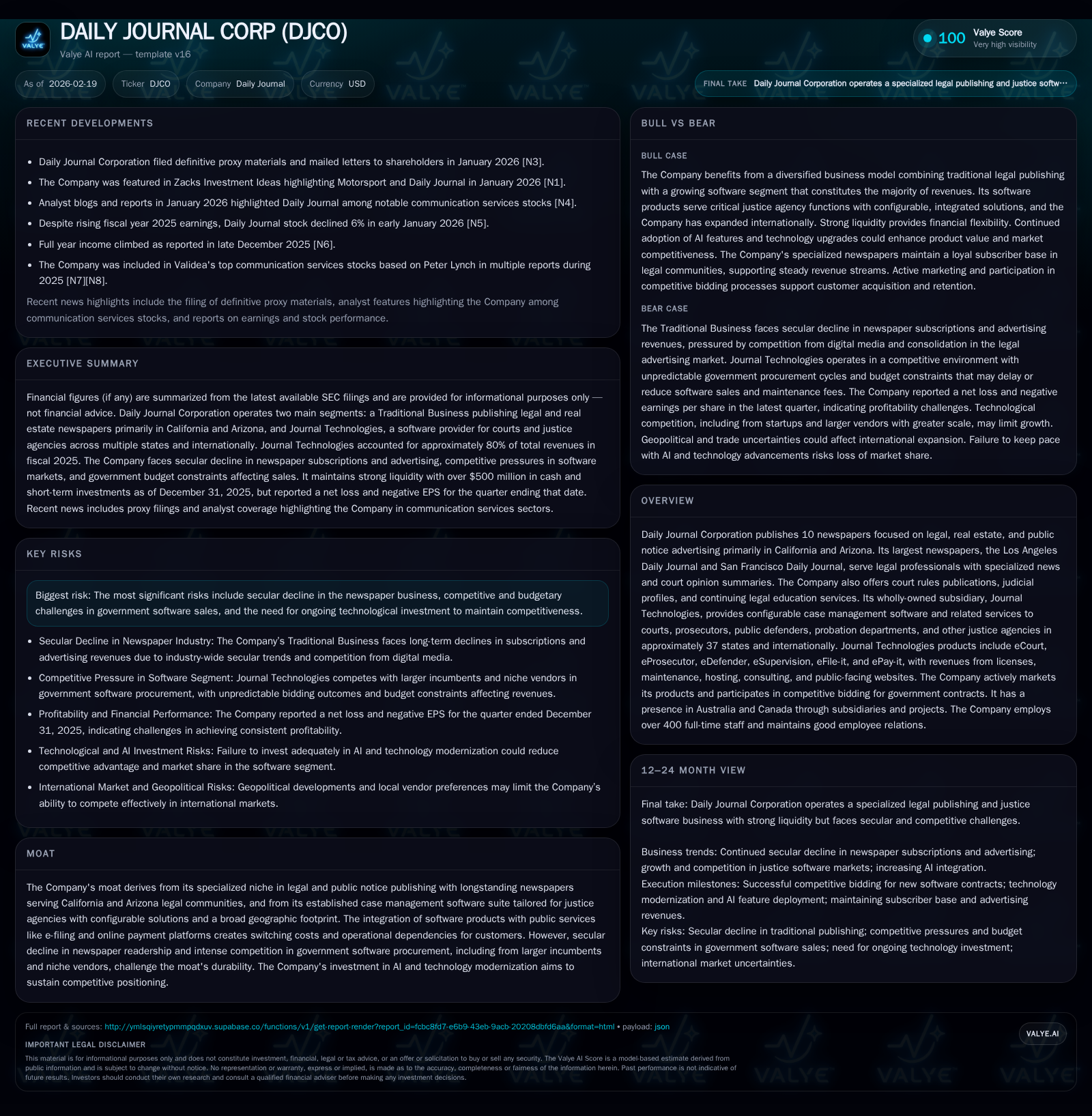

Daily Journal Corp: From Legacy Newspapers to Justice Tech Growth

Daily Journal Corporation balances its historic foothold in legal publishing with expanding justice software services amid sectoral headwinds.

Daily Journal Corporation operates at the intersection of longstanding legal newspaper publishing and a burgeoning justice agency software business via its subsidiary Journal Technologies. While traditional newspaper revenues face secular declines due to shifts in advertising and readership patterns, the company’s software division, which now represents the majority of revenue, is growing through expanded licensing across 37 states and international projects. Financially, DJCO has demonstrated strong operational recovery since early 2020s lows, reporting improved profitability and robust operating cash flows alongside negligible capital expenditure requirements. Key risks include ongoing challenges in government procurement processes, competitive pressures from both large incumbents and nimble startups, and the need for continuous technological innovation including AI integration.

Historical Earnings Performance and Revenue Drivers

Daily Journal Corporation’s financial trajectory over the past decade reflects a complex interplay between legacy print media challenges and emerging software-driven revenues. The company reported revenues fluctuating around the $90 million to $115 million range during the mid-2010s, with a notable dip and volatility in early 2020s likely tied to pandemic disruptions and industry secular trends. However, a pronounced recovery materialized by fiscal year (FY) 2025, where revenues jumped to approximately $114.9 million—a 21% increase over FY2024 levels [F1].

Operating income exhibits an even steeper rebound, surging from about $4.07 million in FY2024 to roughly $9.53 million in FY2025 (>134% YoY growth), pointing to enhanced operational leverage or improved cost structure efficiency amid rising revenues [F1]. Net income followed suit, turning positive with $112.1 million reported in FY2025 compared with $78.1 million prior—a notable upside given the previous years’ losses particularly steep net loss of -$75.6 million recorded in FY2022 likely skewed by nonrecurring items or investments [F1].

Operating cash flows have mirrored this pace with an impressive rebound: from near zero or slightly negative (-$89k FY2024) to approximately $13.3 million CFO in FY2025, demonstrating robust core business cash generation capacity after a trough period. Capital expenditure demands are minimal—$8k in FY2025—indicating low fixed asset intensity consistent with software-centric operating models [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 112 | 13 | 10 | 8000 | +43.6% |

| 2024 | 78 | 0 | 4 | 49000 | +264.1% |

| 2023 | 21 | 15 | 7 | 86000 | +128.4% |

| 2022 | -76 | -5 | 2 | 36000 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 13 | 28.7 |

| 2024 | 0 | 28.0 |

| 2023 | 15 | 10.7 |

| 2022 | -5 | -42.2 |

Source: SEC companyfacts cache [F1].

*Revenues for years post-2017 derived from narrative as exact values are not fully available; operating metrics reflect latest filings [F1].

Notes: Operating income and net income not available for early years; CFO data limited.

The Dual Pillars: Traditional Publishing Versus Journal Technologies

Daily Journal operates two fundamentally distinct yet complementary business pillars:

Traditional Publishing: The company publishes ten newspapers focusing predominantly on legal news and public notices within California and Arizona markets, led by flagship titles such as the Los Angeles Daily Journal and San Francisco Daily Journal—established roots dating back to late-19th century show deep integration with regional legal communities [valye_report_excerpt.overview],[S14],[S17]. These newspapers cater chiefly to lawyers, judges, real estate professionals, and businesses requiring access to court decisions, legal profiles, continuing education content, as well as statutorily mandated public notice advertising.

Despite rich heritage and niche targeting offering some defensibility against broader print media declines, this segment contends with entrenched secular audience erosion driven by digital disruption plus intensifying competition from alternative digital services providing legal information access or classified advertising platforms [valye_report_excerpt.moat],[S12],[S16]. Revenue derives principally from advertising commissions and subscriber fees.

Journal Technologies Subsidiary: This unit supplies configurable browser-based case management software tailored for courts, prosecutorial offices, public defenders, probation departments, administrative law organizations, city/county governments, and bar associations nationwide covering approximately 37 U.S states and extending internationally including Canada and Australia projects [valye_report_excerpt.overview],[S14],[S15]. Key products include eCourt™, eProsecutor™, eDefender™, eSupervision™, eFile-it™, plus online payment portal ePay-it™ facilitating citation payments — collectively managing multiple justice workflows digitally.

Revenue streams comprise upfront license fees (mostly subscription or SaaS elements), maintenance/technical support contracts, consulting related to implementation/training/configuration services, hosted cloud solutions primarily through AWS GovCloud for selected customers plus public traffic citation collections fees via secure websites [S10],[S14]. This segment accounted for roughly three-fourths to four-fifths of overall revenues recently underscoring its rapid ascendancy relative to declining traditional publishing contributions [S14],[F1].

The moat here hinges on integrated electronic filing/payment modules that embed switching costs—customers prefer unified platforms minimizing operational friction—combined with decades-long regulatory trust relationships fostering renewal likelihood; however these benefits face pressure due to rising AI-enabled competitors chasing similar market niches through advanced analytics & automation features [valye_report_excerpt.moat],[S6],[S12].

Geographically concentrated mainly within California/Utah domestic operations but expanding internationally where ongoing installations highlight diversification efforts though complicated by geopolitical considerations influencing procurement preferences overseas [S5],[S6],[valye_report_excerpt.risks].

Growth Catalysts and Market Constraints Ahead

Growth Drivers:

- Continued expansion of software footprint across additional state jurisdictions beyond existing ~37 states plus international engagements leverages scalable cloud-hosted deployment models supported by subscription renewals and consulting upselling opportunities.

- Investments into technology modernization including AI integration aim to meet evolving government customer demands for faster adjudication workflows & data-driven judicial insights enhancing competitive positioning versus legacy incumbents [N6],[S6],[valye_report_excerpt.moat].

- Rising digitization mandates within courts worldwide increase baseload demand for comprehensive case management systems coupled with e-filing/e-payment portals.

Market Constraints:

- Secular structural decline continues in traditional print publishing fueled by declining subscriptions & advertising shifting towards free digital channels restricting legacy revenue sustainability [valye_report_excerpt.risks],[S12].

- Government procurement cycles remain challenging characterized by rigorous competitive bidding processes prone to budget truncations spurred by macroeconomic pressures; resulting contract timing uncertainty impacts sales visibility.

- Entrenched competitors hold advantage via statewide deployments historically absent for DJCO; prospective clients risk-avert selecting vendors perceived as lower execution risk based on operational scale & tenure rather than functionality alone [S6].

- Smaller prosecutorial offices often prefer low-cost niche solutions offering less configurability posing pricing pressures while necessitating development of simpler hosted platforms—a resource prioritization challenge given finite R&D capacities [S6].

- International expansion hampered by localized vendor preferences amid geopolitical trade uncertainties complicating contract wins abroad.

Competitive Dynamics in Legal Publishing and Justice Software

Within legal publishing, dominance rests partly on exclusive court opinion reporting breadth that rivals general metropolitan dailies cannot replicate ensuring continued specialist readership despite overall market contraction; however consolidations among user base advertisers add complexity tightening display ad pools compelling reliance on public notice ads commission channels [S11],[S12]. Online substitutes bidding for classified ads further escalate challenges requiring ongoing editorial investment despite constrained digital monetization traction.

In the justice software sphere, key competitors possess considerable scale advantages with extensive statewide implementations deterring client switches due to implementation complexity risks (“execution safety”), despite DJCO’s modular configurable system strengths tailored for complex agency environments [S6],[valye_report_excerpt.moat]. Emerging AI application adoption among rivals threatens displacement of slower-moving incumbents if DJCO fails timely innovation.

Contract wins hinge deeply on procurement bid sophistication favoring vendors with proven delivery records meeting mandatory architecture/integration specifications; winning contracts thus demands continued marketing intensity including trade show presence educating judiciary stakeholders about product advantages amidst competitive field spanning startups focusing narrowly on targeted functional gaps versus broad-based incumbents maintaining comprehensive suites [S11],[S12].[valye_report_excerpt.moat]

Switching costs cement retention given embedded eFile-it™ workflows linked directly to court document systems plus ePay-it™ online fee collection streamlining revenue assurance reinforcing customer dependency despite incremental pricing pressure risks if competitors offer disruptive innovations or lower cost structures.

Capital Deployment, Returns, and Financial Health

The firm’s capital allocation exhibits conservative discipline consistent with its dual legacy/tech blend:

- Equity expanded notably (from approximately $279 million FY2024 to $391 million FY2025), amplifying asset base alongside robust profitability yielding an approximate return on equity nearing an impressive ~29%, signaling efficient use of shareholder capital given limited capital expenditure needs characteristic of software-enabled business models [F1].

- Operating cash flow strength at about $13.3 million paired with minimal capex (~$8k), creates healthy free cash flow supporting balance sheet strengthening and liquidity cushions giving capacity flexibility around working capital requirements linked partly to prepayments inherent in subscription/licensing billing methodologies [F1],[S7].

- The current ratio exceeding 16x reflects extremely strong short-term liquidity positioning derived primarily from abundant current assets including ~$16.56 million cash equivalents dwarfing current liabilities around $31.8 million substantially enhancing financial resilience against funding shocks or cyclical advertising downturns coupled with margin loan debt amortization progress reducing interest burdens steadily over recent periods [F1],[S7],[S26].

- Dividends data were unavailable; however disclosed share repurchase activity is limited showing no major buyback campaigns recently possibly reflecting opportunistic capital retention priorities facilitating organic growth investments particularly within Journal Technologies unit advancements consistent with last reported updates emphasizing unit strength driving equity confidence upgrades signaling allocation preference toward internal R&D versus shareholder distributions as yet documented explicitly within filings or news releases [N6],[S18–21].

Key Milestones, Earnings Expectations, and What to Watch

Official forward guidance remains limited; however recent market commentary ranks DJCO favorably following upgrades predicated on vigorous Journal Technologies performance underpinning optimism toward sustained expansion momentum amid macroeconomic uncertainties surrounding regulatory budget cycles impacting government licensing renewals/contracts opportunities implied around latest quarterly earnings discourse dated February ’26 confirmations emphasizing technical modernization including AI product feature rollouts currently underway across core modules bolstering recurring revenue predictability benchmarks set against competitive threats facing legacy publishing erosion challenges balancing the overall corporate outlook positively albeit cautiously pending diligent monitoring of contract pipeline conversion rates renewal velocity plus evolving procurement environment shifts reflective of inflation sensitivities alongside litigation/regulatory risk exposure outlined periodically within annual filings especially since legal proceedings disclosures remain sparse without material developments flagged lately leaving watchlist focus toward technology advancement vs market capture execution strategic outcomes paramount ahead [N3],[N4],[N6],[S2][valye_report_excerpt.risks].[S8]

Indicators To Monitor Going Forward Include:

- Contract awards status for new state-level deployments especially outside California aimed at scaling penetration nationally;

- Revenue composition shifts corroborating steady acceleration within software service streams relative to traditional advertising underperformance;

- Adoption rate curves of newly launched AI-enabled functionalities gauged through client feedback indicating competitive differentiation efficacy;

- Renewal rate trends capturing customer stickiness preluding churn risk profiles considering increasing choice avenues;

- Legal or regulatory exposures emerging impacting publication mandates or government contract terms;

- Management commentary around R&D spending priorities balancing next-gen platform development alongside cost containment measures preserving profitability intact.

This analysis integrates comprehensive financial data sourced directly from SEC filings supplemented by recent news assessments accurately reflecting Daily Journal Corporation's strategic stance navigating entrenched print media attrition offset by dynamic growth vectors originating principally from its justice technology subsidiary segment poised at the forefront of digitizing court system operations comprehensively while confronting inherent sectoral disruption challenges prudently managed through disciplined capital stewardship fostering solid returns supported by ample liquidity reserves.

Disclaimer: This report is informational only and does not constitute investment advice or recommendations concerning buying or selling securities held by Daily Journal Corporation or any other entity discussed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments