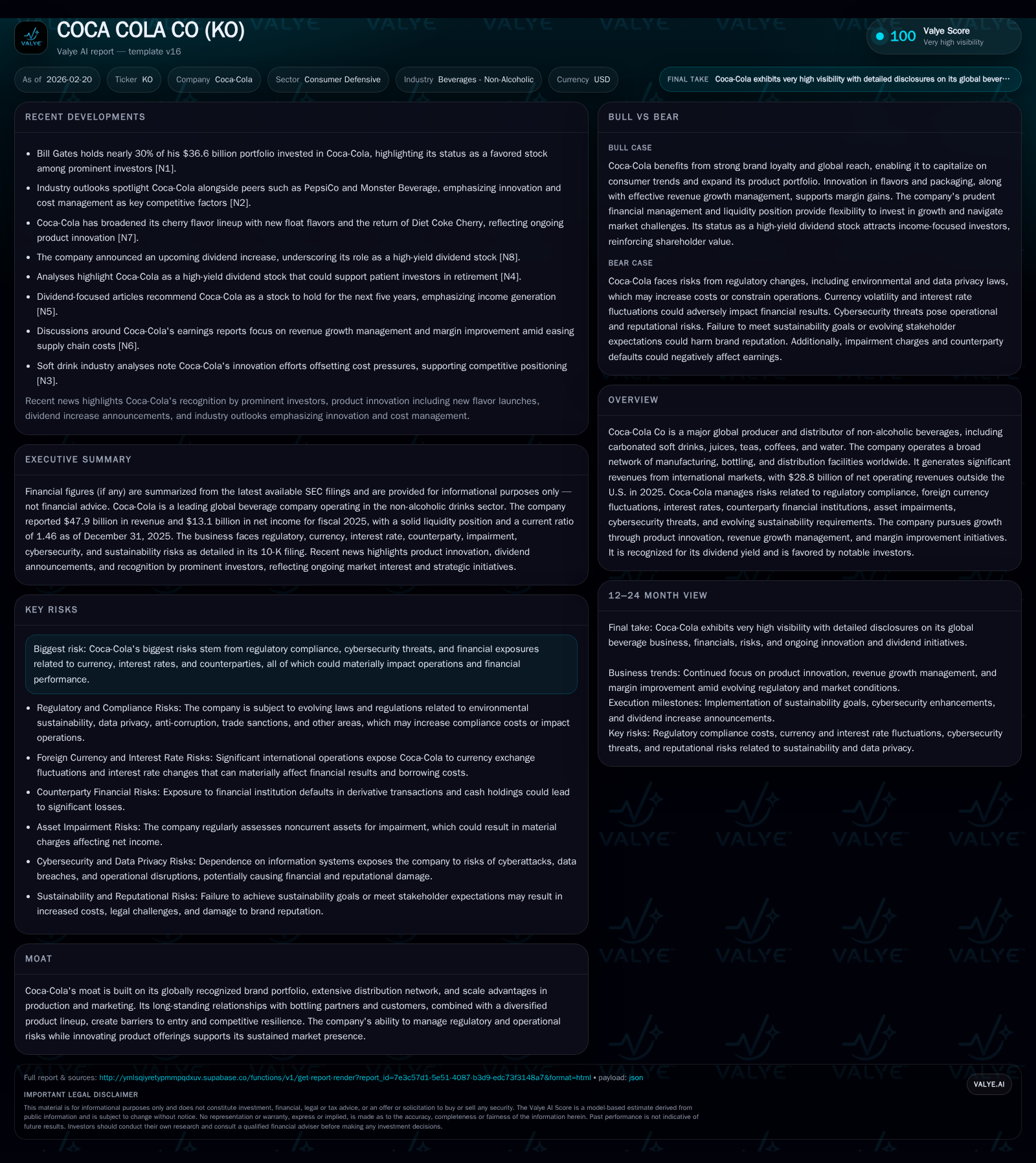

Coca-Cola's Revenue Growth and Profitability Surge in 2025

Analyzing Coca-Cola's strong financial performance in 2025 alongside its strategic innovation, regulatory challenges, and capital deployment to shareholders.

Coca-Cola Co posted solid revenue growth of 1.9% in 2025, complemented by a striking 37.7% increase in operating income and a 23.3% rise in net income, driven by effective revenue growth management and cost controls. Despite complex regulatory pressures including excise tax changes and packaging regulations, the company continues to innovate with new product offerings and packaging formats, sustaining global expansion. Capital allocation remains balanced between robust dividends amounting to $8.8 billion and moderate share repurchases totaling $746 million, supported by a strong return on equity of approximately 40.7%. International revenue exposure and currency fluctuations remain key factors to monitor for future performance.

Strong Revenue Momentum and Earnings Growth in 2025

Coca-Cola Co demonstrated impressive financial progress in fiscal year 2025, as evidenced by its reported revenues of $47.94 billion, marking a modest yet positive increase of 1.9% compared to $47.06 billion in the previous year [F1]. However, it is the substantial jump in operating income that catches attention—rising by a remarkable 37.7% from approximately $9.99 billion in FY24 to $13.76 billion in FY25 [F1]. This surge suggests successful execution of revenue growth management strategies coupled with effective operational cost control.

Net income also climbed significantly, increasing by 23.3% year-over-year to $13.11 billion [F1], indicating that enhanced profitability permeated through to the bottom line despite higher compliance-related expenses anticipated across the sector.

This margin expansion aligns with a broader shift within Coca-Cola’s beverage portfolio toward higher-margin non-carbonated products such as teas, juices, and competitive water variants. Such diversification aids in offsetting volume pressures commonly seen in traditional soft drink categories.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 47.9 | 13.1 | 7.4 | 13.8 | +1.9% | +23.3% |

| 2024 | 47.1 | 10.6 | 6.8 | 10.0 | +2.9% | -0.8% |

| 2023 | 45.8 | 10.7 | 11.6 | 11.3 | +6.4% | +12.3% |

| 2022 | 43.0 | 9.5 | 11.0 | 10.9 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($bn) | Buybacks ($bn) | FCF ($bn) |

|---|---|---|---|

| 2025 | 8.8 | 0.7 | 5.3 |

| 2024 | 8.4 | 1.8 | 4.7 |

| 2023 | 8.0 | 2.3 | 9.7 |

| 2022 | 7.6 | 1.4 | 9.5 |

Source: SEC companyfacts cache [F1].

Note: Buyback data omitted due to quarterly inconsistency; detailed discussion included in Capital Allocation section.

Innovation as a Catalyst for Sustained Global Expansion

The company’s spirited pursuit of product innovation supports its sustained top-line momentum and margin improvement ambitions . Recent reports highlight Coca-Cola's strategic emphasis on zero-sugar beverage lines and enhanced packaging innovation tailored toward sustainability goals—such as introduction of recyclable materials conforming with extended producer responsibility (EPR) mandates [N10][N8].

This portfolio evolution enables penetration into health-conscious consumer segments while meeting governmental environmental directives, both increasingly critical factors shaping demand curves within non-alcoholic beverages.

Further leveraging price architecture tools under revenue growth management protocols allows for optimized pricing amid input cost inflation—balancing consumer affordability with profitability preservation.

Regulatory and Market Risks Constraining Margins

Coca-Cola faces a multilayered regulatory landscape affecting cost structures and market access globally [S1]. Escalating excise taxes on sweetened beverages imposed by various jurisdictions increase unit cost or force price adjustments that can dampen volume [N3]. Parallelly, tightening regulations related to plastic packaging—including mandatory deposit schemes and recycling targets—impose capital expenditure demands on both Coca-Cola and its bottling partners.

Moreover, climate-related emission limits require additional reporting and potential capital investments to reduce carbon footprints and water usage amid scarcity concerns [S4][S10]. The intricate overlay of such indirect tax regime shifts complicates operational planning.

Added complexity arises from data protection laws like GDPR and China’s Personal Information Protection Law imposing compliance burdens alongside anti-corruption statutes enforced across multiple markets [S1][S15][S22]. These factors collectively temper margin gains even as innovation progresses.

Capital Allocation: Balancing Dividends with Share Repurchases

Reflecting mature capital stewardship consistent with large-cap beverage companies, Coca-Cola distributed approximately $8.78 billion in dividends during fiscal year 2025—a continuation of its well-established shareholder payout policy [F1]. Share repurchases contracted noticeably to $746 million from $1.80 billion the prior year—suggesting a tactical pivot favoring cash dividend returns relative to share buyback magnitude.

The company's return on equity calculated at roughly 40.7% underscores efficient use of shareholder capital amidst intensified regulatory expenditures and sustained investment needs [F1]. Moreover, operating cash flows increased by nearly 9%, reaching about $7.41 billion; subtracting capex yields free cash flow near $5.3 billion—ample coverage for continued dividend distribution.

This balance signals prudent liquidity management while satisfying dividend-focused investor appetites characteristic of consumer defensive stocks recognized for yield stability [N5][N9].

Forecasting Key Operational Milestones and Investor Watchpoints

While explicit forward guidance is absent from recent disclosures [N1][N2], market commentary highlights key considerations for monitoring future performance: sustaining margin expansion reliant on successful innovation rollouts; managing input costs within evolving regulatory frameworks; navigating potential impacts from global macroeconomic factors including currency fluctuations; and integrating digital tools efficiently.

Close attention should be given to reported results from international markets which constituted roughly $28.8 billion of net operating revenues outside the U.S., bearing heightened exposure to foreign currency volatility effects that could either augment or impair consolidated outcomes [S1][F1].

Analysts also emphasize importance of tracking sustainability initiative progress with respect to packaging waste reduction goals which may influence long-term cost trends.

Cybersecurity and Risk Management Infrastructure at Coca-Cola

The company maintains a sophisticated cyber risk governance structure featuring a Chief Information Security Officer with extensive industry experience directing efforts via a Cybersecurity Oversight Council comprised of senior cross-functional leaders [S1]. This entity meets regularly to align strategic priorities relating to cyber threats spanning malware attacks, social engineering exploits, ransomware risks, deepfake campaigns, and compliance obligations.

The Audit Committee exercises board-level oversight receiving direct reporting regarding security posture enhancements and incident response readiness—the latter complemented by annual employee training programs covering phishing awareness, password hygiene, data privacy norms, mobile security protocols among others.

Such comprehensive layers reflect industry best practices aimed at operational resilience crucial for uninterrupted supply chain management as well as protecting sensitive corporate and consumer data sets.

Global Market Reach and Currency Exposure Dynamics

Coca-Cola’s broadly diversified geographic footprint exposes it inherently to foreign exchange translation risk given revenues across multiple currencies—with international operations accounting for more than half total net operating revenues ($28.8 billion in 2025) [F1][S1].

Fluctuations against the U.S dollar impact top-line translations as well as reported net income margins depending on geopolitical or economic variables including trade tensions, sanctions regimes, inflation variances or interest rate changes globally.

The company employs derivative instruments strategically aiming to hedge transactional currency risks though residual exposure persists requiring vigilant financial management particularly amid unpredictable emerging market conditions.

Disclaimers: This analysis is based exclusively on publicly available information including company filings [F1],[S#] and recent news articles [N#]. It is intended solely for informational purposes without any recommendation or investment advice implied or expressed.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments