Dalrada Technology Group's Struggle with Losses and Legal Headwinds in Diversified Ventures

Dalrada’s revenue stabilizes modestly while escalating losses, legal conflicts, and liquidity constraints underscore operational challenges.

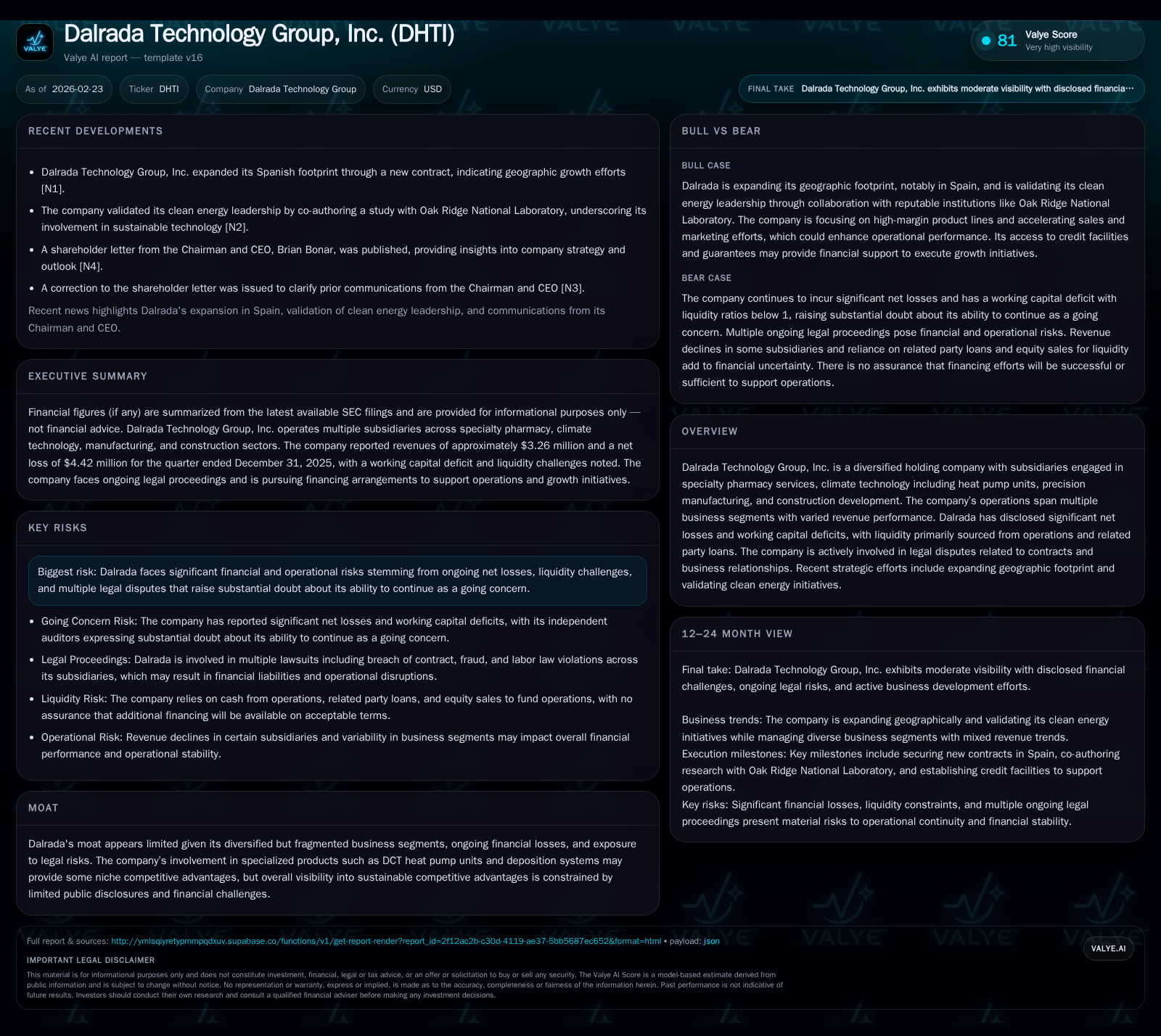

Dalrada Technology Group operates across specialty pharmacy services, climate tech, precision manufacturing, and construction but continues to report deepening net losses and a severe working capital deficit. This financial strain is compounded by several ongoing lawsuits involving material contract disputes, which may impact future cash flows and strategic flexibility. Growth efforts center on commercializing DCT heat pump technology validated by Oak Ridge National Lab research and expanding geographically into Spain. However, cash flow pressures and reliance on related party loans limit near-term operational leverage. Key milestones in 2026 include resolutions of major litigations and progress in niche clean energy commercialization.

Revenue Growth Amid Persistent Multi-Segment Losses

Dalrada Technology Group's financial trajectory underscores a precarious balance between revenue stabilization and sharply deteriorating profitability metrics. Over the four fiscal years ended FY2025 (June year-end), reported revenues showed marked volatility: dropping sharply from approximately $29.7 million in FY2023 to a stabilized $20.3 million in FY2025, reflecting a modest increase of 2.3% year-over-year from FY2024 to FY2025 [F1]. This stabilization belies intensified operating challenges as operating income worsened from -$10.4 million in FY2022 to -$20.5 million by FY2025 (a 23.8% YoY improvement compared to an even wider prior loss) [F1]. Net income followed a similar declining pattern, recording -$24.6 million at FY2025 with a marginal improvement of 14.9% YoY [F1].

Segment-level performance emerges unevenly from disclosed narratives: Dalrada Climate Technology’s construction arm (Bothof Brothers) secured multiple projects fueling increased cost of revenues yet failed to translate into positive operating leverage [S16], while Dalrada Precision Manufacturing experienced significant sales declines due to reduced deposition technology orders [S20]. Operating cash flow worsened significantly, reaching nearly -$18 million at FY2025 — more than double prior year outflows — reflecting the sustained negative free cash flow trend after accounting for capex of $374K (down ~14% YoY) [F1]. The sharp increase in cash burn precludes any near-term cushion for strategic investments without external financing.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 20 | -25 | -18 | -20 | +2.3% | +14.9% |

| 2024 | 20 | -29 | -8 | -27 | -33.3% | -42.7% |

| 2023 | 30 | -20 | -5 | -21 | +54.3% | -43.9% |

| 2022 | 19 | -14 | -10 | -10 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -18 | 364.9 | |

| 2024 | -8 | -841.5 | |

| 2023 | 14826 | -5 | -493.9 |

| 2022 | 14826 | -11 |

Source: SEC companyfacts cache [F1].

Note: Operating Income YoY % for FY2022 omitted due to lack of prior comparable data.

The lack of operating leverage despite capex reductions indicates structural weaknesses across business segments unable to leverage fixed overhead or scale their offerings profitably.

Complex Legal Landscape Impacting Core Operations

Dalrada confronts an intricate legal matrix that strains its resources and clouds near-term prospects. Among the most significant disputes is the Asset Group litigation surrounding a $3.24 million Purchase Order for IRIS Ear Loop Face Masks sold during the pandemic through Dalrada Health Products (DHP). Asset Group contests DHP's authority to sell these masks [S1][S8]. A cross-complaint filed by DHP alleges tortious interference involving Dimco Holdings with expected profits tied to this contract ($3.24M). These cases are scheduled for trial on January 31 and April 2026 respectively [S1][S8].

Another critical suit involves MDIQ's contractual failure relating to insurance claims processing for COVID-19 testing via Empower Genomics under Dalrada Financial Corporation (DFCO). DFCO is counter-suing for approximately $2 million in alleged unpaid claims resulting from MDIQ's non-performance [S1][S8]. No trial date has been set.

Further litigation arose between DFCO and former distributors/consultants Simon Gray and DePrey Company alleging intentional interference with contractual relations which compromised production ties with supplier Zhongshan Mide Hardware Products Co., Ltd., currently under discovery with tentative trial dates pending [S1][S8]. Additional suits include allegations against former executives regarding fraud and trade secret misappropriation related to UK subsidiaries [S27].

The financial disclosures highlight these litigations as material going concern risks that could impose unforeseen contingencies or settlements draining operating cash flow or restricting access to capital markets for refinancing [S28][S6][S8]. The overlapping timelines culminating around mid-2026 horizon sharpen attention on the firm’s legal expense burden and potential liabilities that weigh heavily on corporate governance decisions.

Clean Energy Validation and Geographic Expansion as Growth Catalysts

Within its fragmented portfolio lies Dalrada Climate Technology’s promising DCT heat pump unit line—one of its few emerging niche competitive advantages supported by third-party validation through Oak Ridge National Laboratory’s co-authored study released early 2026 [N4]. This academic endorsement serves as a commercial credibility cornerstone potentially enhancing contracting velocity amid green energy mandates.

Moreover,Late January witnessed Dalrada’s expansion into the Spanish market with new contracts via its Dalrada Technology Spain subsidiary aimed at broadening geographic reach beyond U.S.-centric operations [N3]. These moves align with management's described strategic intent to accelerate marketing efforts around high-margin products including DCT units alongside precision parts manufacturing [N2][S6].

Yet caution tempers optimism as these growth drivers mature within an organizational structure hampered by capital scarcity and administrative overhead spread thin across unrelated verticals lacking synergy or additive moat attributes beyond technological niches like heat pumps or deposition systems.

Liquidity Crisis: Cash Flows, Working Capital, and Capital Structure

Dalrada’s liquidity condition epitomizes acute stress consistent with its persistent net loss trajectory. At December 31, 2025 quarter-end balance sheet highlights included cash & equivalents below $100K ($70K), current assets totaling approximately $7.17 million versus current liabilities exceeding $22.5 million—translating into a razor-thin current ratio near 0.32 evidencing deep working capital deficits primarily fueled by related party accounts payable balances used tactically to fund payroll and vendor expenses [F1][S7][S4][S9].

Operating cash flow remains far negative; exacerbated over recent reporting periods due mainly to reduced accounts payable availability limiting liquidity buffer; investing activities modestly scaled down with capex hovering around low-to-mid hundreds of thousands per annum—a fraction of operating losses—with financing activities relying heavily on related party loans or equity issuances casting heavy dilution shadows [S11][S13][S15].

Corporate filings repeatedly state substantial doubt regarding going concern status hinging on successful execution of capital raises including recent Master Performance Standby Letter of Credit agreements signed January 21st , 2026 supporting limited liquidity extensions but clearly contingent on external debt or equity financing at yet unspecified terms [S3][N1]. Continued losses alongside stretched payables suggest acute funding gaps remain unresolved absent transformative operational improvement.

Capital Allocation, Returns, and Equity Dynamics

Capital deployment patterns reveal constrained discretionary capacity amid survival mode postures: annual capital expenditures have declined moderately from approximately $640K in FY2022 down to $374K in FY2025 aligning with curtailed growth investment mandates tied primarily to maintaining existing facilities rather than aggressive expansion [F1][S16]. Buybacks registered historically negligible (~$15K) while no dividends have been paid throughout recent periods reflecting zero yield focus amid fundamental earnings deficit.

Shareholders’ equity turned negative by end of FY2025 at roughly -$6.75 million following cumulative deficit accumulation despite episodic equity raises earlier maintaining small positive balances circa early fiscal years; this deterioration signals persistent erosion of book value complicating future capital raising given dilution risk concerns commonly associated with frequent share issuance as a lifeline strategy under liquidity duress [F1].

Returns on equity approximated from trailing net loss versus equity base result in statistically meaningless negative percentages illustrating absent profitability or capital efficiency domains requiring urgent strategic remediation or portfolio rationalization.

Dividends paid data is not available from provided tags; similarly buybacks are minimal historically.

Key Upcoming Milestones and Uncertainties to Monitor

Critical inflection points center around several foreseeable catalysts:

- Trial dates beginning January through April 2026 addressing major contract breach lawsuits involving Asset Group/DH Products and tortious interference claims could materially alter contingent liabilities exposure or recoveries impacting liquidity forecasts [S1][S8].

- The effectiveness of recently executed standby letter of credit agreements binding Genefic subsidiary negotiations set December deadlines will influence working capital runway extension possibilities amidst ongoing operating losses [S3][N1].

- Commercial traction within DCT clean energy units post-validation from Oak Ridge National Laboratory offers an evidence-based gating factor for scaling sales pipeline momentum particularly within environmental technology mandates favored globally but remains unproven at scale thus bearing execution uncertainty [N4][N2].

- Expanding footprint in Spain flagged as incremental revenue contributor warrants monitoring actual sales-to-orders conversion rates against management communications emphasizing cautious optimism amidst multi-segment struggles [N3][N2].

- Persistent dependence on equity issuance as primary liquidity source introduces execution risk amid possible shareholder dilution backlash given lack of dividend distribution capability or buyback cushions analogous to larger peers.

- Legal expenses continue weighing heavily on operating cost structure challenging any attempt at expense rationalization without resolution outcomes.

Disclaimer

This analysis is solely for informational purposes regarding Dalrada Technology Group Inc.'s operations and financial condition based on publicly available information as of February 23rd , 2026 or noted release dates without offering investment advice or recommendations. The information herein reflects historical data points together with qualitative assessments per provided filings and announcements without speculative projections beyond established company disclosures or verifiable evidence.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments