GLAUKOS Corp Faces Tradeoffs Between Commercializing New Ophthalmic Products and Operating Losses

GLAUKOS expands its glaucoma and corneal therapy portfolio with FDA approvals but contends with persistent losses and regulatory challenges.

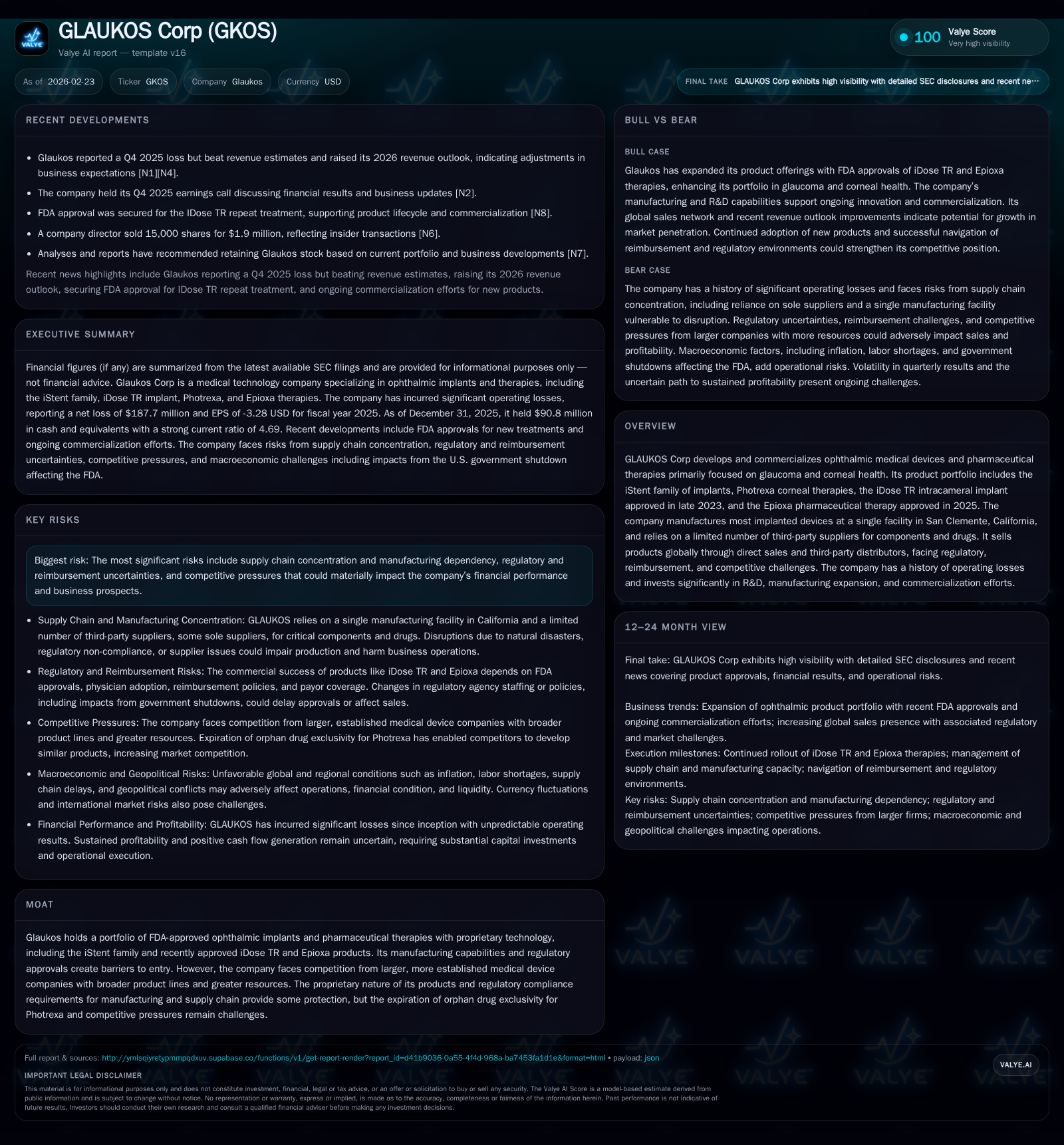

GLAUKOS Corp, a developer of ophthalmic implants and therapies focused on glaucoma and corneal health, reported operating losses for four consecutive years amid incremental product approvals. The company recently launched the iDose TR intracameral implant and Epioxa pharmaceutical therapy, both promising innovations, but commercialization hurdles and supply chain concentration weigh on margins. While raising its 2026 revenue outlook, GLAUKOS retains significant R&D and manufacturing investments. Reimbursement uncertainty, competitive pressures, and regulatory risks remain key factors influencing future growth trajectory and capital allocation decisions.

Historical Performance Overview

GLAUKOS Corp has endured persistent operating losses through FY2022 to FY2025. Operating income worsened from a loss of about $33.7 million in FY2022 to nearly $200 million in FY2025, indicating escalating investments that outpace current revenue generation [F1]. Meanwhile, net income follows a similar widening loss trajectory but improved slightly year-over-year from -$146.4 million in FY2024 to -$187.7 million in FY2025.

Operating cash flow also remained negative across this period, though the decline moderated significantly in FY2025 (-$14.8 million) compared to prior years (-$61.3 million in FY2024). This suggests some operational efficiency improvements or positive cash inflows linked to product sales growth [F1]. Capital expenditures declined sharply over the four-year window from $30.3 million in FY2022 to just $7.7 million in FY2025, potentially signaling completion of major capacity expansions or tighter CapEx discipline.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -188 | -15 | -200 | 8 | -28.2% |

| 2024 | -146 | -61 | -122 | 6 | -8.7% |

| 2023 | -135 | -58 | -129 | 20 | -328.0% |

| 2022 | -31 | -33 | -34 | 30 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -22 | -28.6 |

| 2024 | -68 | -19.1 |

| 2023 | -78 | -29.2 |

| 2022 | -63 | -5.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue data not available; Dividends and Buybacks data not available.

Product Portfolio and Commercialization Efforts

GLAUKOS specializes in ophthalmic implants and pharmaceutical treatments primarily targeting glaucoma and corneal diseases such as keratoconus:

- The iStent family remains a core implant offering for glaucoma treatment.

- The iDose TR drug-device combo implant, approved by the FDA in late 2023, represents a novel sustained-release travoprost delivery method aiming to improve patient adherence by reducing daily eye drops usage [S2][N9].

- The Epioxa pharmaceutical therapy was FDA approved in 2025 as an incision-free alternative addressing keratoconus care, a notable innovation compared to existing cross-linking procedures; commercialization began shortly thereafter [S2].

- Photrexa corneal therapies have faced generic competition following expiration of orphan drug exclusivity in 2023 [S20].

The company's manufacturing activities are centralized at a single San Clemente facility focused on implant production, while components such as drug formulations depend on a limited number of third-party suppliers, underscoring concentrated supply risk [S5].

Growth Prospects and Constraints

Future growth hinges critically on successful adoption of recently commercialized products iDose TR and Epioxa:

- Physician training, patient outcomes consistency, adequate reimbursement levels, pricing strategies, manufacturing scale-up capability, and regulatory compliance form key gating factors for revenue ramp prospects [S2].

- The competitive landscape includes entrenched multinational medtech firms with broader offerings that may pressure pricing power or limit market share gains [S20].

- Legislative reforms impacting healthcare reimbursement frameworks remain uncertain with the U.S government actively investigating drug pricing policies, raising risks related to coverage levels under Medicare/Medicaid and private payors [S11][S24].

- Additionally, expiration of orphan drug exclusivity for products like Photrexa opens potential competitive entry points threatening legacy revenues [S20].

- Trade tariff fluctuations present volatility exposure for component raw material costs despite predominant U.S.-based sourcing [S25].

Market acceptance of Epioxa as an incision-free keratoconus therapy could establish differentiation enabling expanded penetration internationally if regulatory clearances proceed efficiently under MDR/UKMDR frameworks; however, added complexities here could delay rollout or increase compliance costs significantly compared to domestic launches [S27][S24].

Forecasts And Milestones To Watch

Explicit future guidance remains sparse publicly; however recent commentary highlighted an upward revision of the full-year 2026 revenue outlook despite missing Q4 earnings expectations reflecting confidence in reaccelerated sales growth driven by new product adoption dynamics [N1][N4]. Key forthcoming milestones include:

- Expansion of physician usage training programs for iDose TR and Epioxa across key global markets.

- Scalability improvements in manufacturing throughput given prior concentration constraints.

- Regulatory progress for pipeline candidates or label expansions under FDA coordination between drug-device centers.

- Monitoring reimbursement status updates from CMS policies affecting both device implantation procedure coverage and pharmaceutical product inclusion within federal health programs.

Given no dividend payments or share repurchases were disclosed historically or recently, capitalization strategy appears focused on reinvestment into R&D, commercialization scale-up efforts, and balance sheet preservation per reported cash buffers [F1][N3].

Returns And Capital Allocation Dynamics

With ongoing net losses exceeding $180 million annually recently and negative free cash flow estimated around -$22 million for FY2025 (operating cash flow minus CapEx), GLAUKOS is far from profitability benchmarks typical in medtech sectors where double-digit ROEs predominate once commercial maturity is attained [F1]. Approximate ROE calculated at about -28.6% confirms this phase of operational investment over returns.

The company’s strong current ratio (~4.7x) suggests liquidity adequacy from existing assets including $90+ million cash holdings supporting near-term operational needs without evident financing distress despite operating losses [F1]. However, net equity declined notably last year indicating share issuance or accumulated deficits impact capital structure dynamics.

Capital expenditures have trended downwards post peak expansion phases possibly reflecting shift from platform build-out toward commercialization execution and efficiency optimization rather than capacity growth alone.

There has been no evidence of dividends or material buybacks since early years; thus capital allocation clearly prioritizes reinvestment into strategic R&D pipelines including clinical trials conducted under stringent regulatory frameworks that involve costly, prolonged approval cycles typical for ophthalmic drugs/devices with combined FDA oversight hurdles [S11][S17].

Regulatory And Competitive Risks

Regulatory risk is multifaceted given GLAUKOS’s dependence on approvals not only for new products but also additional indications or modifications requiring repeated clearance processes amid evolving legislation affecting FDA resourcing levels potentially delaying submissions or reviews [S25]. Ongoing mandatory post-market surveillance requirements impose significant operational overheads including adverse event reporting obligations.

Global expansion is constrained by variable international approval pathways including the EU MDR/UK MDR regimes which have become notably stringent increasing costs for CE marking compliance with possible market access implications if delayed [S27][S24]. Furthermore, price sensitivity responsiveness is intensified outside the U.S., with local payor dynamics often disadvantaging smaller entrants relative to established incumbents possessing regional scale advantages.

Competitive positioning is challenged by medical device conglomerates wielding extensive salesforces plus broad intellectual property moats outside Glaukos’s narrower specialty portfolio plus newer entrants developing alternative microinvasive glaucoma surgery (MIGS) technologies which could undermine market share if efficacy or cost advantages are proven clinically relevant promptly [S20][S16].

Additionally, expiration of exclusivities such as photrexa's orphan drug status exposes sales volumes to erosion via generics eroding pricing leverage long-term unless mitigated through lifecycle management efforts.

Industry Context Analysis

Microinvasive glaucoma surgery devices constitute a niche within the broader ophthalmology sector with growing demand driven by aging populations globally but mired by complex reimbursement coding challenges limiting swift procedural uptake rates particularly outside top-tier hospitals where MIGS adoption tends to concentrate initially before broader diffusion occurs. Manufacturing complexity around intracameral implants also stresses quality control imperatives due to stringent biocompatibility requirements enforcing adherence to FDA’s Quality System Regulation (QSR). Pharmaceutical-delivering implants add another layer necessitating rigorous Good Manufacturing Practices (cGMP) regime adherence covering both device assembly plus sterile drug formulation safeguards increasing capital intensity versus conventional standalone pharma products alone. These dual-regulatory burdens dictate a capital structure suitable for mid-to-long term horizon return realization typical for combination product developers.

Conclusion

GLAUKOS Corp operates at an inflection point balancing ambitious new product launches against prolonged historical losses accentuated by challenging regulatory environments and concentrated supply chains. Its focus on proprietary ophthalmic solutions like iDose TR and Epioxa diversifies addressing chronic glaucoma management versus corneal disease therapies—however effective commercialization execution coupled with favorable reimbursement outcomes will be decisive levers shaping financial sustainability going forward. While liquidity sampling indicates short-term stability supporting ongoing initiatives from a cash perspective strong capital discipline will be essential amid intensifying competitor landscapes involving multi-indication platforms backed by legacy giants well-established globally. Investors monitoring GKOS should watch upcoming quarterly results closely for meaningful shifts in operating margin trends or cash flow improvements alongside updates on regulatory milestones abroad that will influence product rollout pace across geographies. The company’s inherent tradeoff remains navigating high upfront R&D/manufacturing investment loads now with returns dependent on market adoption velocity catalyzed by physician training success coupled with payor acceptance variability across jurisdictions.

This analysis does not constitute investment advice or recommendations regarding GLAUKOS Corp securities but aims to provide a detailed understanding based on public disclosures up to February 23, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments