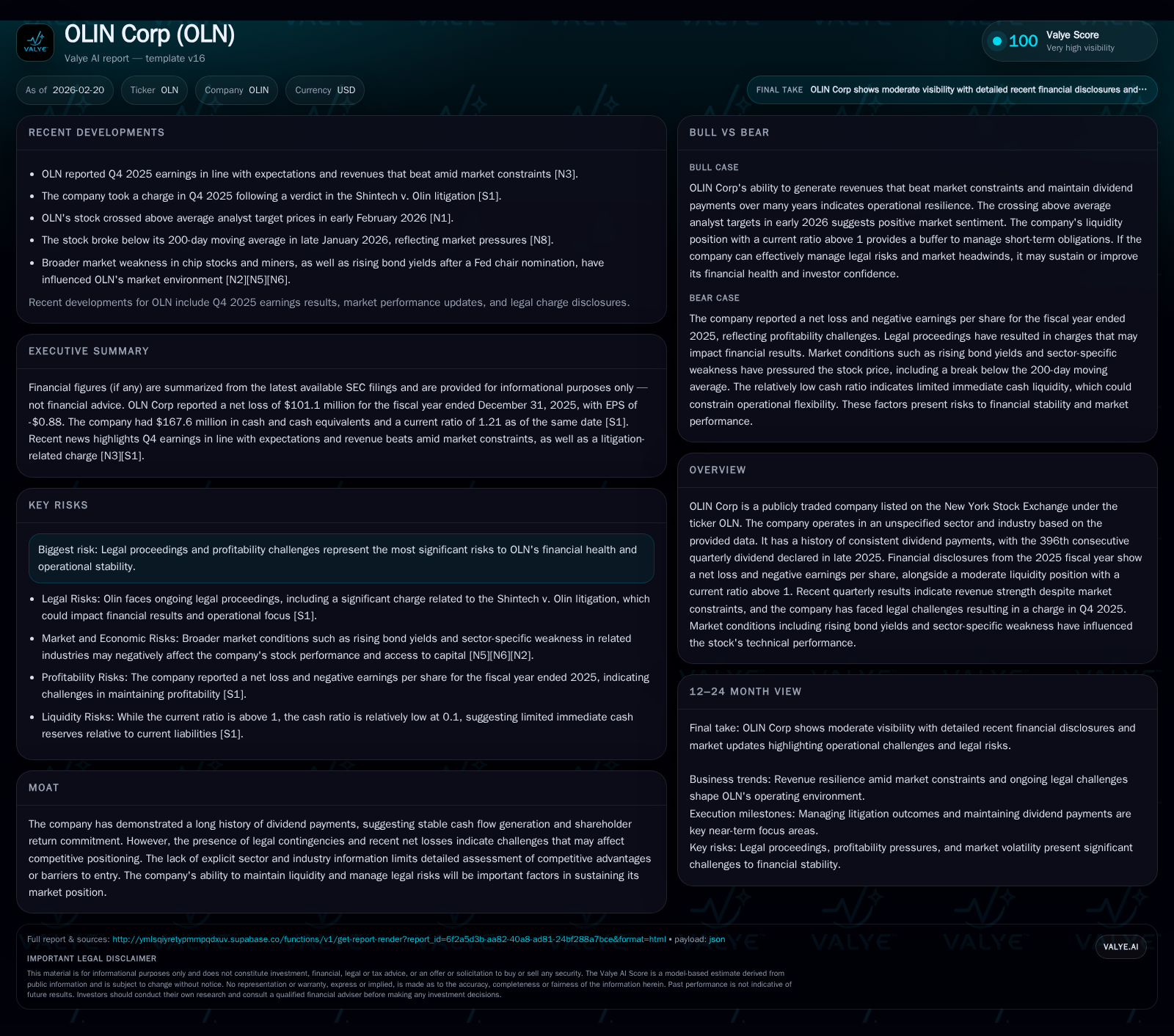

OLIN Corp Faces Profitability Pressure and Legal Charges While Sustaining Dividend Streak

Despite a sharp earnings decline and legal contingencies, OLIN maintains robust cash flow and a 397-quarter dividend record.

OLIN Corporation has encountered substantial earnings headwinds during the 2025 fiscal year, posting a net loss for the first time in recent years amid ongoing legal challenges. However, the company continues to generate strong operating cash flow and sustain its longstanding dividend payments, marking 397 consecutive quarters. Revenue gains in Q4 2025 contrasted with a charge stemming from litigation weigh on near-term profitability. The interplay between managing legal risks, maintaining liquidity, and capital allocation choices will shape OLN’s operational resilience moving forward.

Historical Performance Highlights

Over the past four fiscal years, OLN's earnings have displayed considerable volatility with operating income and net income experiencing dramatic swings. Operating income was notably high at nearly $1.78 billion in FY2022 but declined sharply each subsequent year to just $5.3 million in FY2025—a drop of over 98% from the previous year [F1]. Net income mirrored this trajectory, swinging from a peak of $1.33 billion in FY2022 down to a substantial loss of $101 million in FY2025.

Despite these earnings contractions, the company maintained strong operating cash flows above $474 million as of FY2025, only about 6% lower than FY2024 levels, suggesting resilient core cash-generating capability even as accounting profits suffered [F1]. Capital investment activities remained robust with capex rising modestly by 16% YoY to $226 million, signaling continued asset modernization or expansion efforts.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -101 | 474 | 5 | 226 | -196.3% |

| 2024 | 105 | 503 | 297 | 195 | -76.8% |

| 2023 | 452 | 974 | 712 | 236 | -65.9% |

| 2022 | 1327 | 1922 | 1779 | 237 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 92 | 51 | 248 |

| 2024 | 94 | 300 | 308 |

| 2023 | 101 | 711 | 738 |

| 2022 | 116 | 1351 | 1685 |

Source: SEC companyfacts cache [F1].

Note: Revenue data is not available in provided tags and thus omitted.

Future Growth Prospects

Explicit guidance on future performance remains limited amid current uncertainties; however, several factors may influence OLN's growth trajectory:

Revenue Dynamics: Recent Q4 results revealed revenue strength that beat estimates despite challenging market conditions such as sector-specific weakness and macroeconomic headwinds including rising bond yields [N1], which could signal some pricing power or volume resilience.

Legal Impact: The Shintech v.Olin litigation ruling resulted in a charge booked in Q4 2025 that materially affected net income [S15], which may linger as a financial and reputational overhang until resolved.

Capital Investment: Steady or rising capex trends point to investment in operational capabilities that could support future growth or efficiency gains but also impose short-term cost pressures [F1].

Dividend Sustainability: The company’s uninterrupted run of quarterly dividends suggests confidence in steady cash flows even if profitability is under pressure; continuing this trend depends on free cash flow generation staying healthy.

Forecasts and Milestones to Watch

OLIN has not issued explicit multi-year guidance recently; thus key indicators worth monitoring include:

- Quarterly revenue progression relative to market expectations

- Legal proceedings updates and their financial implications

- Operating margin recovery or further erosion signals

- Free cash flow trends given recent higher capex

- Capital allocation adjustments such as buyback scale changes beyond historically reduced activity

These factors combined will likely define investor sentiment and operational strategy adjustments.

Returns and Capital Allocation Review

Calculations based on latest figures show an approximate ROE of -5.5% for FY2025 due to net losses eroding equity returns [F1]. This contrasts sharply with prior profitable years when ROE was strongly positive.

The firm generated substantial free cash flow estimated around $248 million for FY2025 (operating cash flow less capex), allowing continued shareholder payouts despite challenging earnings [F1]. Dividends paid totaled approximately $91.6M, consistent with prior years though slightly lower than peak levels.

Meanwhile, share repurchases contracted dramatically from historical highs near or above $700M down to around $50M last year, reflecting more cautious capital return amid risk management priorities [F1]. Maintaining liquidity appears prudent given ongoing legal uncertainties and volatile profit metrics.

The liquidity position remains stable with a current ratio of approximately 1.21 (current assets roughly $1.97B vs current liabilities near $1.63B), providing reasonable short-term financial flexibility without excessive leverage concerns [F1].

Industry Context Analysis (Not Company-Specific)

While the sector specifics are not disclosed here, companies similar to OLN often operate within cyclical chemical manufacturing or industrial materials industries where commodity cost fluctuations and regulatory risks significantly impact margins. Recent industry-wide themes include inflationary cost pressures, supply chain recalibrations post-pandemic, and environmental compliance expenses escalating capital intensity.

Investors also monitor product mix shifts toward higher-margin specialty chemicals versus bulk commodities as a means of stabilizing earnings volatility in such sectors.

Summary Outlook

OLIN Corp is navigating a turbulent phase characterized by sharply compressed profitability driven by litigation costs and market headwinds but counterbalanced by solid operational cash flow generation and rigorous dividend discipline stretching back nearly four decades consecutively.

The company's ability to manage ongoing legal risks prudently while leveraging investments into asset bases amid challenging external conditions will be pivotal for restoring earnings vigor.

Capital allocation appears increasingly conservative with dividend payments prioritized over substantial share buybacks recently—a strategic tradeoff reflecting market uncertainty.

Key developments around revenue sustainability signals post-Q4 performance beats and resolution or mitigation of litigation impact will be critical milestones shaping OLN's near-term operational steadiness and investor confidence.

Disclaimer: This analysis is intended solely for informational purposes based on publicly available data and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments