Global Technologies Ltd’s Transition Through Growth Challenges and Capital Constraints

GTLL confronts significant liquidity pressures while pivoting to emerging health-tech subsidiaries to fuel sustainable growth.

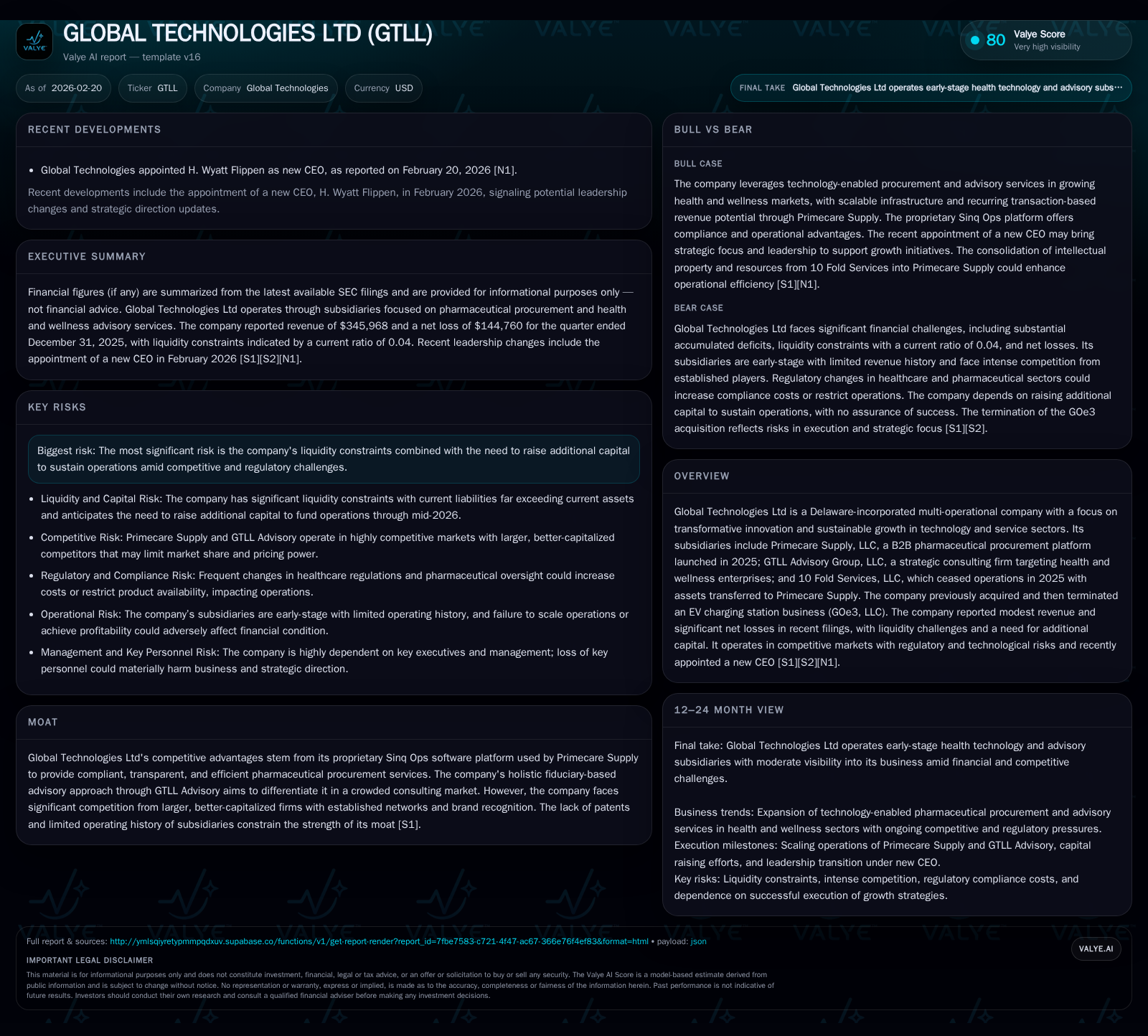

Global Technologies Ltd (GTLL) has faced a turbulent financial history marked by sustained net losses and liquidity stress but is now refocusing under new leadership on technology-enabled pharmaceutical procurement and fiduciary advisory services. Despite modest revenue declines recently, operating income improved significantly, driven by better control of expenses and operational efficiencies. Core growth prospects hinge on scaling Primecare Supply’s proprietary Sinq Ops platform and launching GTLL Advisory’s consulting services within competitive, regulated markets. However, constrained cash reserves and a critical need for capital injections represent substantial risks to execution.

Recent Leadership Change Signals Strategic Refocus

Global Technologies Ltd appointed H. Wyatt Flippen as CEO in February 2026, marking a strategic pivot focused on stabilizing the company's financial position while accelerating growth initiatives within its health-technology subsidiaries [N1]. Mr. Flippen's leadership is critical amid ongoing liquidity challenges and operational restructuring as the company seeks to scale Primecare Supply’s proprietary procurement platform alongside the launch of GTLL Advisory’s consulting services.

Historical Financial Performance Overview

The company’s fiscal performance over recent years reveals persistent net losses tempered by improving operational metrics:

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1045671 | -342681 | 354823 | 171468 | -1.1% | -142.2% |

| 2024 | 1057685 | 812081 | -38738 | -211984 | +178.5% | |

| 2023 | -1034040 | -392437 | -523212 | +19.1% | ||

| 2022 | -1278315 | -484410 | -499288 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 29.7 |

| 2024 | 53.0 |

| 2023 | 22.8 |

| 2022 | 134.9 |

Source: SEC companyfacts cache [F1].

Revenue peaked modestly in FY2024 before a slight contraction in FY2025. Notably, operating income swung from significant losses in prior years to positive territory in FY2025—a sign of improved expense management or operational efficiency gains. However, net income remained negative due largely to non-operating costs or interest expenses.

The accumulated deficit exceeded $167 million as of June 30, 2025 with stockholders’ equity deeply negative at approximately -$1.15 million—highlighting sustained balance sheet stress despite signs of operational progress [F1], [S1].

Operating cash flow turned strongly positive in FY2025 at $355K after continuous cash burn in previous years. Capital expenditures remain minimal reflecting a lean business model focused on technology platforms rather than heavy asset investments [F1], [S16].

Subsidiary Operations: Growth Engines Amid Uncertainty

Primecare Supply LLC

Established late 2024 with operations commencing in May 2025, Primecare Supply functions as a B2B pharmaceutical procurement platform connecting licensed "503B" outsourcing facilities with medical clinics across the U.S., leveraging the proprietary Sinq Ops software for compliant ordering and payment processing [S1], [S6]. The platform aims for scalable transaction-based revenue from direct clinic relationships and reseller networks.

Primecare Supply has quickly onboarded multiple manufacturers and hundreds of clinic users—an encouraging footprint for such an early-stage venture.

GTLL Advisory Group LLC

Founded May 2025, GTLL Advisory offers fiduciary-based consulting targeting medical spas and wellness clinics with an emphasis on measurable financial and operational improvements rather than traditional marketing services. Revenue generation is expected to begin during FY2026 as part of Global Technologies’ broader health-tech portfolio expansion [S6].

The prior subsidiary "10 Fold Services" ceased active operations in mid-2025 with assets transferred to Primecare Supply to consolidate strategic focus.

Competitive Landscape Challenges

Primecare Supply operates in a highly competitive pharmaceutical distribution sector dominated by established manufacturers and distributors possessing greater scale and brand recognition. The lack of patent protections for the Sinq Ops platform places further pressure on differentiation beyond service quality and regulatory compliance features [S5], [S7].

Similarly, GTLL Advisory faces intense competition from numerous well-funded consulting firms specializing in the fragmented medical spa market.

Maintaining competitive advantages through ease-of-use, transparent compliance workflows, and trusted fiduciary advisory will be essential for client acquisition and retention.

Liquidity Position and Capital Needs

The company faces acute liquidity challenges as evidenced by an extremely low current ratio of approximately 0.04 at December 31, 2025—indicating current liabilities vastly exceed current assets [F1], [S18].

Management anticipates raising about $500K by mid-2026 primarily to fund public company compliance costs and support scaling efforts within Primecare Supply and GTLL Advisory Group operations [S18].

Auditors have expressed substantial doubt about GTLL's ability to continue as a going concern absent successful capital raises—underscoring material execution risks related both to financing access and effective deployment.

Milestones & Outlook

While no formal financial guidance has been provided publicly, key milestones for FY2026 include expanding reseller partnerships within Primecare Supply’s network alongside growing clinic adoption rates driving recurring transaction revenues. Concurrently, GTLL Advisory aims to initiate revenue-generating consulting engagements targeting measurable client outcomes.

Monitoring quarterly results will be critical to assess whether these subsidiaries can transition from nascent ventures into consistent profit centers amid competitive pressures.

Returns Metrics & Capital Allocation Summary

Relevant returns metrics such as ROE are not explicitly disclosed in filings; however, approximate calculations using recent annual net income (-$342K) over negative equity (~-$1.15M) indicate a negative return context given ongoing losses despite operating improvements.

No dividends have been declared or paid historically nor are any anticipated given pressing funding needs. Share repurchases were last recorded in FY2022 but have since ceased aligning with preservation of capital priorities amid liquidity constraints [F1], [S20].

Free cash flow approximated at $318K (operating cash flow minus capex) reflects improving internal cash generation capacity despite overall financial stress.

Risks: Regulatory Compliance & Market Adoption Uncertainties

Primecare Supply faces stringent regulatory oversight tied to FDA licensing of "503B" pharmaceutical manufacturers; changes could materially impact product availability or increase compliance costs adversely affecting operations [S4], [S15].

Cybersecurity risks around data integrity pose additional reputational and financial threats given sensitive healthcare information handled via proprietary platforms [S14].

Competitive intensity from larger incumbents capable of price disruption or technological innovation heightens risk that scaling ambitions may not materialize fully or profitably.

Moreover, adoption risks remain significant given the early-stage nature of both subsidiaries within rapidly evolving healthcare procurement and advisory markets.

Disclaimer: This report is based solely on available SEC filings and news disclosures as of February 20th, 2026. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments