Global Industrial Co's Growth and Profitability Strengthen Despite Supply Chain and Integration Risks

GLOBAL INDUSTRIAL Co leverages product breadth and multi-channel sales, navigating cost pressures and acquisition integration.

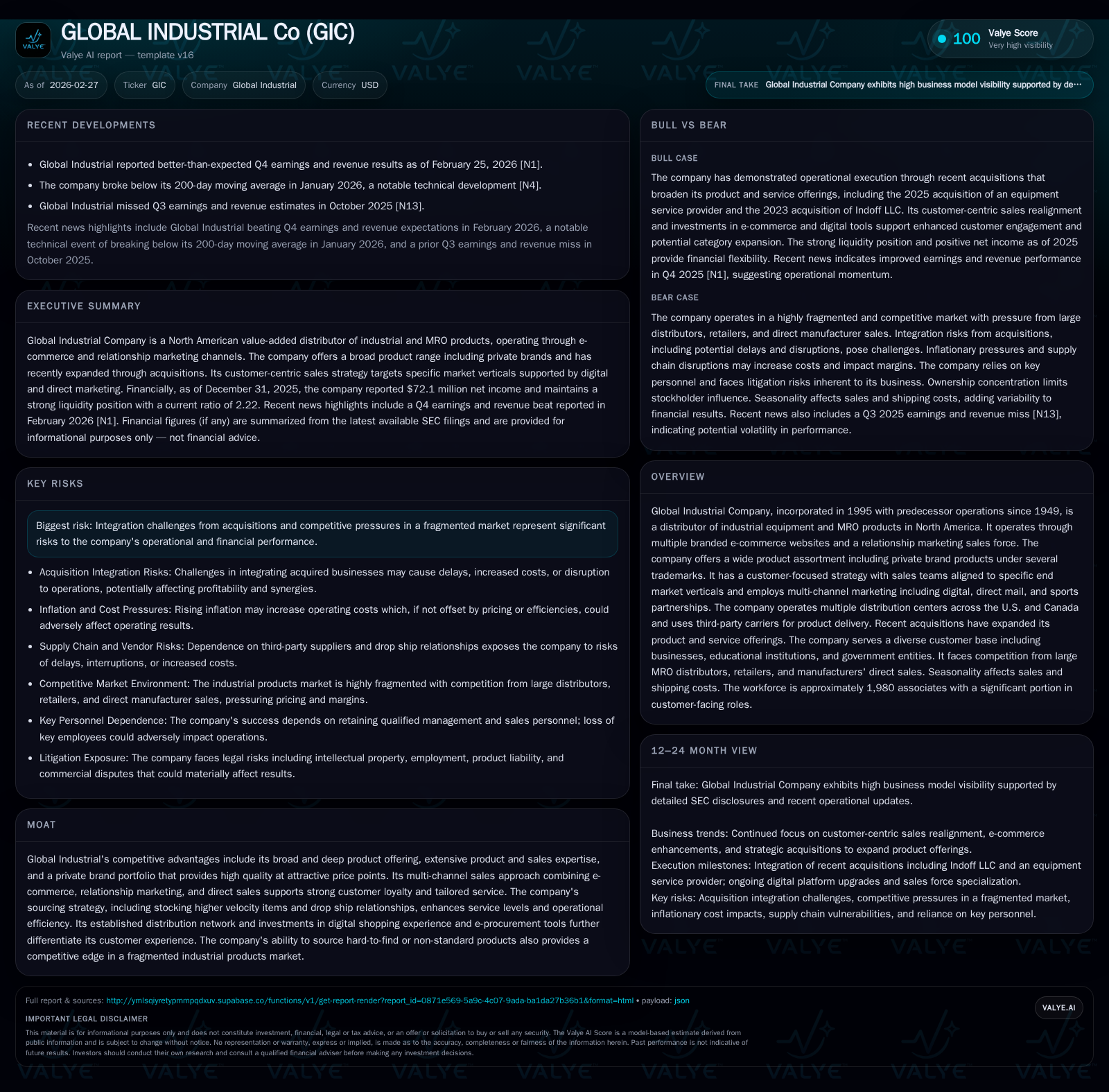

GLOBAL INDUSTRIAL Co, a long-established North American distributor of industrial and MRO equipment, showed solid financial growth in 2025 with operating income up 21.2% year-over-year amid ongoing supply chain challenges. The company’s diversified product portfolio, focused customer segmentation, and private brand expansion underpin its growth prospects, while recent acquisitions broaden service offerings. However, risks from market fragmentation, inflationary pressures, and integration of acquired businesses pose continuing operational challenges. Capital allocation reflects consistent dividend increases and modest share repurchases supported by strong free cash flow generation.

Company Overview and Market Position

GLOBAL INDUSTRIAL Co has been a value-added distributor of industrial equipment and MRO (maintenance, repair, operations) products in North America since its incorporation in 1995, with predecessor operations dating back to 1949 [S17]. It serves a broad customer base comprising businesses across manufacturing, construction, education, government entities, healthcare, retail, hospitality, and logistics sectors through both branded e-commerce platforms and a relationship marketing sales force aligned by end-market verticals [S22].

The company distinguishes itself via an extensive product portfolio that includes leading national brands as well as private label products marketed under several trademarks such as Global™, Nexel™, Paramount™, Interion™, and Absocold™ [S17]. These private brands enable GLOBAL INDUSTRIAL to offer differentiated value—combining quality with competitive pricing—and contribute higher gross margins relative to national brands.

MULTI-CHANNEL SELLING AND CUSTOMER STRATEGY

Its go-to-market strategy emphasizes customer centricity with specialized sales teams targeting distinct vertical markets such as public sector, industrial manufacturing, commercial enterprises, retail, healthcare, and hospitality/multi-family housing customers [S22][S11]. This vertical alignment strengthens product expertise and fosters closer customer relationships characterized by personalized service and tailored solutions.

Additionally, the company’s online presence integrates e-commerce websites supporting over 60% of transaction volume alongside direct mail campaigns, digital marketing initiatives, catalog mailings, telephone support centers, and field sales representatives [S5][S22]. This multi-channel approach enables effective penetration of both small/mid-sized accounts and large enterprise customers.

Historical Financial Performance

The company demonstrated improving profitability in recent years with operating income rebounding after a dip in 2024:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 72 | 78 | 98 | 3 | +18.2% |

| 2024 | 61 | 51 | 81 | 4 | -13.7% |

| 2023 | 71 | 112 | 97 | 4 | -10.3% |

| 2022 | 79 | 50 | 105 | 7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 40 | 9 | 75 |

| 2024 | 38 | 47 | |

| 2023 | 31 | 7 | 108 |

| 2022 | 28 | 0 | 43 |

Source: SEC companyfacts cache [F1].

Operating income improved significantly in FY2025 compared with prior year despite inflationary headwinds and supply chain volatility documented in filings [F1][S1]. Net income followed the same trend with an increase of over 18%. Operating cash flow surged notably by over half year-on-year reflecting improved working capital management or higher profitability before capex investments were slightly curtailed.

Dividend payments have grown steadily indicating discipline in returning capital to shareholders while buybacks remain opportunistic though modest in scale relative to free cash flow generation.

Growth Drivers and Strategic Initiatives

Acquisition-Led Expansion

Recent acquisitions anchored growth opportunities: the May 2023 purchase of Indoff LLC for $72.6 million expanded its footprint in the MRO space offering material handling products and commercial interior solutions across North America [S17][S23]. Followed by the April 2025 acquisition of an equipment service provider for $4.3 million broadening specialized equipment capabilities further amplifying value-added services beyond traditional distribution.

Private Brand Development & Category Expansion

Global Industrial continues to emphasize high-margin private brand lines which provide pricing flexibility amidst commodity cost fluctuations affecting steel or petroleum-based components impacting national brand pricing [S7][S20]. The company actively vets new private brand categories based on customer demand signals harvested via sophisticated multi-channel CRM systems driving category expansion especially focused on consumables maintenance & repair supplies that generate repeat orders driving wallet share gains.

Digital & Multi-Channel Sales Ecosystem

Investment in digital shopping experience including enhanced e-procurement tools like EDI integrations for large accounts facilitates convenience fostering new customer acquisition alongside strong retention of existing accounts through personalized follow-ups by relationship marketers assigned per industry vertical [S22].

Distribution Network Optimization

Operating from five main U.S.-based distribution centers plus one large Canadian facility supplemented by smaller regional warehouses ensures broad geographic coverage enabling shorter lead-times supporting high service levels [S5]. Strategic use of drop ship vendor relationships helps maintain inventory efficiency while stocking higher-velocity SKUs internally conserves working capital yet guarantees delivery reliability.

Risks Capping Growth Potential

While well-positioned structurally, the business faces acute risks:

- Supply Chain Disruptions: Heavy dependence on Chinese manufacturers for private label goods exposes vulnerability to pandemic-related shutdowns, tariff escalations, transportation bottlenecks including port congestion or container shortages leading to product delays or lost sales [S1][S13][S20]. Efforts to diversify supplier base mitigate but do not eliminate these risks.

- Market Fragmentation & Competition: The North American industrial distribution sector is extensively fragmented with competition from both broadline MRO distributors like Grainger Inc., Fastenal Inc., MSC Industrial Direct Inc., as well as online retailers including Amazon creating relentless pricing pressure coupled with consolidation trends forcing scale efficiencies difficult for mid-size players to achieve [S15][S16].

- Inflationary Pressures: Fluctuations particularly in commodity prices for steel or fuel impact procurement costs as well as freight expenses which are sometimes absorbed partially eroding gross margins if not fully passed along through price increases risking demand elasticity impacts [S7][S20][S18].

- Acquisition Integration Risks: Difficulties integrating acquisitions—such as Indoff LLC—could disrupt operations or dilute synergies thereby impairing anticipated benefits increasing working capital requirements or internal control challenges especially due to geographic dispersion of acquired entities [S23].

- Liquidity & Capital Access: Rising interest rates can affect financing costs both for Global Industrial’s operations as well as customers potentially impacting demand availability or pushback on payment terms requiring additional working capital funding commitments [S10][S24].

- Information Security Vulnerabilities: Heavy reliance on e-commerce technology platforms exposes operational risk to cyber-attacks or system outages that could disrupt order processing thereby affecting reputation and sales volumes [S24].

Capital Allocation & Returns Profile

GLOBAL INDUSTRIAL generated approximately $77.8 million in operating cash flow during fiscal year 2025 against capital expenditures of only $3.1 million yielding free cash flow around $74.7 million—a robust figure supporting dividend growth alongside share repurchases without stretching financial flexibility [F1]. Dividends climbed steadily reflecting confidence in earnings stability while repurchases implied selective deployment signaling opportunistic management behavior responding to valuation metrics or excess liquidity.

Shareholders should note the concentrated ownership structure whereby the Leeds brothers collectively command nearly two-thirds of voting power ensuring continuity but limiting broader shareholder influence on strategic direction or governance matters [S25].

Approximate ROE calculated at about 23% demonstrates attractive profitability levels consistent with prudent leverage enabled by solid equity base growth driven by retained earnings over time enhancing book value organically [F1].

Outlook & What To Watch (Analyst Perspective)

Given lack of explicit forward guidance disclosed recently [N1], observers should monitor:

- Effects of continued supply chain normalization post-pandemic relative to order fulfillment times influencing revenue cadence.

- Pricing strategies vis-à-vis inflation pass-through effectiveness sustaining margin integrity.

- Integration progress updates related to recent acquisitions especially operational synergies realization timelines.

- Competitive dynamics especially shifts caused by consolidation moves among peers or evolving digital disruptors.

- Variations in commodity input costs impacting product assortment profitability mix.

- Investments towards advanced analytics enhancing category expansion capability leveraging rich customer data insights.

- Capital return policy consistency balancing shareholder payouts against reinvestment needs amid economic uncertainties.

Conclusion

GLOBAL INDUSTRIAL Co presents an established industrial equipment distributor underpinned by broad product depth augmented by private brands with a nimble multi-channel selling model that effectively targets diversified North American markets through digitally supported relationship marketing teams focused on specific end sectors. Despite macroeconomic challenges such as inflationary headwinds and persistent supply chain disruptions mostly tied to China exposure plus risks inherent with expanding acquisitions integration the company demonstrates improving profitability metrics complemented by sizable free cash flow enabling shareholder returns via dividends and buybacks. Continued emphasis on category expansion within consumables combined with technological investment positions GLOBAL INDUSTRIAL well within the fragmented yet competitive landscape characterized by consolidation among larger peers as it seeks sustainable mid-single-digit top-line growth translating into solid earnings advancement for stakeholders.

This report is for informational purposes only and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments