Greenland Energy Co: Early Post-Business Combination Performance and Growth Prospects

A newly public energy company, Greenland Energy Co is navigating early-stage operational scaling following a March 2026 business combination.

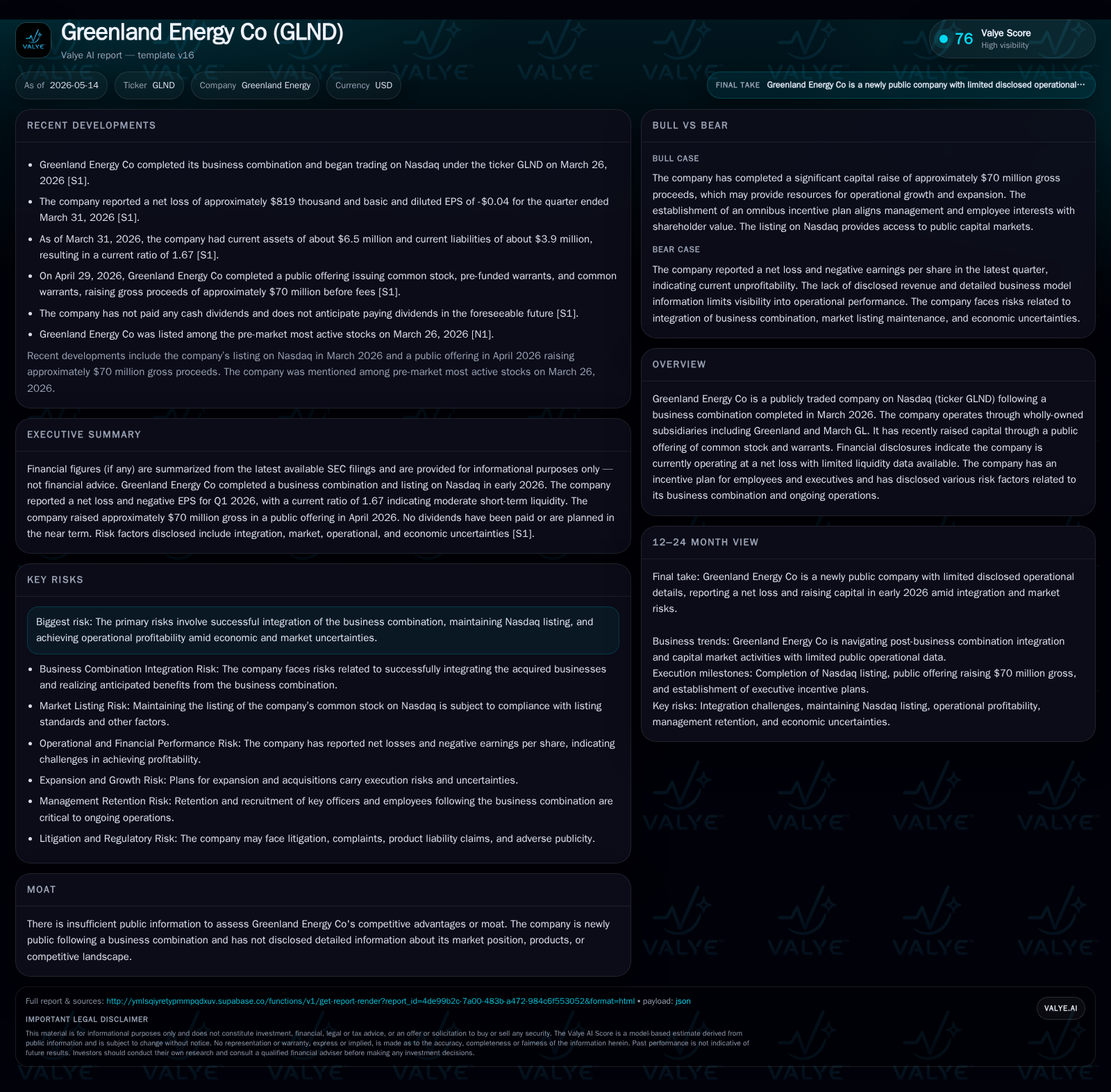

Greenland Energy Co emerged as a Nasdaq-listed entity in March 2026 through a business combination, marking the start of its public operating phase. Its latest quarterly filing reveals ongoing net losses but a manageable liquidity position supported by recent equity offerings. The company’s business model centers on wholly owned subsidiaries Greenland and March GL, though detailed product and market specifics remain limited in public disclosures. Uncertainties prevail around integration success, competitive positioning, and pathway to profitability amid industry regulatory challenges. Moving forward, monitoring operational traction and capital deployment will be critical to assessing growth momentum and risk mitigation.

Latest Quarterly Operating Update: Key Developments and Implications

Greenland Energy Co's debut as a publicly traded company on Nasdaq (ticker GLND) followed the completion of its business combination in March 2026. The latest quarterly report filed on May 13, 2026 (Form 10-Q) anchors our current understanding of the company's operational state post-merger [S2]. This filing reveals that Greenland Energy is operating at a net loss of $818,679 for the quarter ended March 31, 2026 [F1]. Despite this early-stage unprofitability typical of newly combined entities, the company maintains a current ratio of approximately 1.67 based on reported current assets ($6.5 million) against current liabilities ($3.9 million) as of that date [F1]. This indicates an adequate short-term liquidity cushion to fund ongoing operations.

Additionally, Greenland Energy closed a significant equity capital raise in late April 2026 through a public offering comprising common stock, pre-funded warrants, and common warrants totaling gross proceeds of about $70 million before fees [S3]. The offering’s combined purchase price was approximately $4.00 per share plus warrant unit, providing the company with fresh financial resources to support working capital needs and operational scaling.

This sequence—business combination closing in late March followed by capital infusion in April—signals Greenland Energy's transition from private operating stages to actively building public-market credibility while managing initial losses inherent to this phase. The retained liquidity will be critical as the company progresses beyond integration hurdles toward stable revenue generation.

Business Model and Product Overview: What Drives Greenland Energy Co?

Public documents indicate Greenland Energy operates through two wholly owned subsidiaries: Greenland and March GL [S6]. While detailed descriptions of the subsidiaries' exact product offerings or service scope are limited in the filings provided to date, the company's name and context suggest involvement in energy production or exploration-related activities.

Given industry conventions for such entities—especially within corporate structures involving exploration or energy resource subsidiaries—primary revenue sources likely derive from producing or trading physical energy commodities or providing related infrastructure services. Customers may include utilities, commercial energy purchasers, or industrial clients with long-term contracts influencing revenue volume and pricing dynamics.

Currently though nascent post-combination status means Greenland Energy has yet to reveal comprehensive go-to-market strategies or customer mix data publicly. This opacity makes it difficult to definitively assess product differentiation or embedded pricing power at this stage. However, strategic ownership consolidation under the parent entity hints at management’s intent to streamline operations for future growth scalability.

Industry Structure and Competitive Position: Unpacking Market Dynamics

The publicly available disclosures do not elaborate on Greenland Energy's competitive positioning or market share metrics, leaving its economic moat essentially indeterminate for now. Given its recent Nasdaq listing subsequent to the merger event and absence of detailed competitive references, it appears the company remains in early alignment phases within its industry segment.

Energy sector participants typically encounter entrenched incumbents with established contract pipelines alongside regulatory frameworks imposing compliance costs and operational restrictions. These factors often temper pricing power despite underlying structural demand for energy commodities.

Moreover, Greenland Energy acknowledges general risks common to companies undergoing business combinations—integrational challenges compounded by external market uncertainties—which may constrain swift realization of competitive advantages [S7]. Regulatory exposure in environmental compliance or licensing further complicates market entry barriers.

Without more granular disclosure on asset portfolio quality or proprietary technology advantage, Greenland's market position should currently be viewed as developing rather than defensibly strong.

Growth Drivers: Pathways to Scaling Operations and Market Presence

Key growth vectors for Greenland hinge fundamentally on successful execution of the recently consummated merger integrating Greenland and March GL into a cohesive whole [S4]. Smooth organizational assimilation will enable synergies that could improve operational margins and capacity utilizations—critical in capital-intensive energy sectors.

The fresh capital infusion raised through April’s equity and warrant offering equips management with resources necessary for working capital sustenance as well as potential near-term expansion initiatives such as capacity upgrades or selective acquisitions referenced broadly in prospectus disclosures [S3]. Further bolstering growth prospects is management's recruitment focus on experienced leadership roles tasked with driving profitable scaling post-merger [S4].

Market acceptance following Nasdaq listing expands avenues for visibility plus institutional investor engagement. Steady enhancement in financial reporting transparency combined with milestone achievements like contract backlog growth or utilization improvements will serve as tangible growth indicators going forward.

Risks and Constraints: Integration, Profitability, and Market Uncertainties

Investing interest in Greenland Energy must reckon with substantial risks tied directly to its early lifecycle stage post-business combination. Principal among them is the execution risk associated with integrating multiple subsidiaries into a single effective operation capable of generating sustainable profits [S7].

Ongoing net losses underline inherent challenges ahead before attaining break-even cash flow states; sustained unprofitability risks depleting liquidity absent further financing rounds.

Moreover, undefined competitive positioning amid entrenched industry players contributes strategic uncertainty around future market share capture possibilities [S7].

Additional constraints come from exposure to commodity price volatility typical of energy sectors plus regulatory policy shifts impacting emissions standards or drilling rights—all factors outside direct company control yet materially impactful.

Key Milestones and What to Monitor Next for Greenland Energy Co

Looking ahead, critical monitoring points include upcoming quarterly earnings reports expected to deliver updated clarity on operational progress beyond initial post-merger adjustments [S2]. Execution markers encompassing successful integration steps among subsidiaries—including consolidation of back-office functions—and early signs of revenue ramping rooted in contracting activity merit close attention.

Capital deployment outcomes post-April funding round offer insights into whether incremental resources translate effectively into scalable output rather than merely offsetting legacy operational deficits [S3]. Likewise, regulatory developments influencing sectoral norms might impinge on longer-term strategic planning horizons.

Investor focus should also track management commentary during earnings calls for signposts regarding potential secondary equity offerings or debt financing plans aimed at bridging remaining funding gaps during scale-up phases.

Disclaimer: This analysis is based solely on publicly available SEC filings up to May 13th, 2026, supplemented by company disclosures without any private insights. It does not constitute investment advice but aims to provide an informed perspective on Greenland Energy Co’s early-stage performance dynamics.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments