Genasys Inc.: Balancing Backlog Growth with Revenue Recognition and Liquidity Challenges

Genasys navigates the intersection of integrated tech offerings, complex ASC 606 revenue rules, and financial pressures amid expanding backlog visibility.

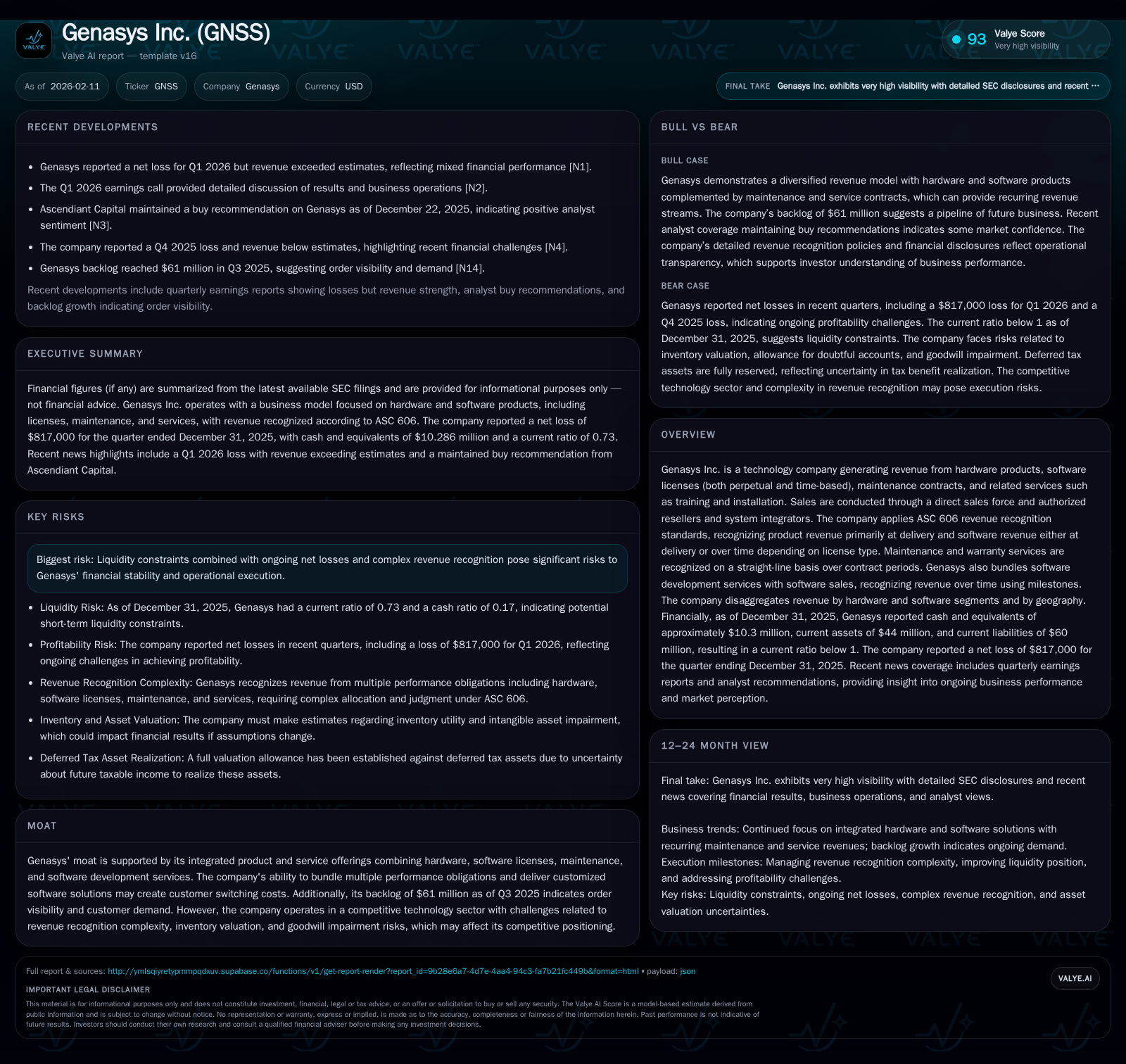

Genasys Inc. presents a paradox of accelerating revenues supported by a sizable $61 million backlog and an integrated product-service model, yet it grapples with recurring net losses and liquidity constraints. Its revenue streams are segmented between hardware shipped at point-of-sale and multifaceted software licenses recognized over time. The application of ASC 606 introduces significant accounting complexity, influencing revenue timing and margin transparency. While its bundled offerings foster customer stickiness, operational execution risks relating to working capital, inventory valuation, and goodwill remain key vulnerabilities to monitor.

Navigating Genasys’ Revenue Landscape: Hardware Meets Software

Genasys Inc. operates within a multifaceted technology model generating revenues primarily from hardware products alongside software licenses—both perpetual and time-based—as well as maintenance contracts and related professional services such as installation and training [S1]. This diverse product mix forms the backbone of its integrated solutions approach. Sales occur via a combination of direct sales personnel and authorized resellers or system integrators. Notably, these partners often hold minimal inventory due to firm end-customer commitments.

Revenue segmentation clearly delineates hardware performance obligations from software-related deliverables. Hardware revenues are typically recognized when control passes to logistics providers or customers upon delivery; meanwhile, software-related revenues depend on license structures—with perpetual licenses recognizing a portion upfront adjusted for associated maintenance fees—and subscription-like time-based licenses recognized on a straight-line basis over contract terms [S1]. Moreover, Genasys bundles standalone software development services with license agreements in some contracts, adding further complexity to how revenue is allocated across multiple performance obligations.

This business model aims not only to capture various customer needs but also to embed switching costs through turnkey solutions combining tangible products with ongoing software access and support services. Such bundling strategies form a pivotal element of Genasys’ commercial approach, supporting deeper customer engagement beyond single-product transactions.

Unpacking ASC 606: Complexity in Revenue Recognition and Its Consequences

Compliance with ASC 606 standards imposes demanding requirements on how Genasys recognizes revenue from its heterogeneous contracts [S1]. Under ASC 606’s five-step framework—encompassing contract identification through performance obligation satisfaction—Genasys must precisely determine when control transfers occur for each component.

Hardware product sales present less ambiguity: revenue is recognized generally at a point in time when products ship to customers or carriers who then assume control. Returns are historically immaterial due to limited customer return rights absent product defects.

Software licensing introduces additional layers of accounting nuance. Perpetual licenses combined with one-year maintenance necessitate bifurcation of fees so that embedded maintenance components are deferred and amortized linearly over service periods. Time-based licenses—essentially subscriptions bundled with mandatory maintenance—are fully recognized ratably across contractual terms.

Additionally, long-term contracts exemplified by the Puerto Rico Early Warning System Project follow an input cost model reflecting progress over time. Here, hardware costs contribute zero margin initially with margin recognition phased based on labor cost percentages toward completion [S1].

This complexity can impair transparency regarding the timing and quality of revenues: upward spikes from hardware deliveries can contrast markedly with smoother but deferred software license income streams. Furthermore, milestones achieved in bundled service arrangements affect periodic revenue computations dynamically, enhancing challenges for investors parsing reported results.

Financial Health Under the Microscope: Liquidity, Losses, and Working Capital Dynamics

Financially, Genasys faces constraints reflected in liquidity ratios that raise caution flags about short-term solvency. As of December 31, 2025, cash and equivalents stood at approximately $10.3 million while current liabilities exceeded $60 million resulting in a current ratio around 0.73—a metric indicating potential challenges meeting near term obligations without bolstered cash inflows or external financing [F1][valye_report_excerpt].

Moreover, the company continues to register net losses (-$817k in FY2025) despite exhibiting revenue growth momentum [F1]. Loss absorption reflects sustained operational pressures including investment in R&D, selling general administrative expenses aligned with maintaining direct sales forces and channel partners, as well as costs stemming from inventory carrying or impairment risks.

Inventory valuation serves as a crucial lever affecting working capital efficacy; misestimates here could precipitate write-downs impacting earnings unpredictably. Similarly, goodwill balances on the balance sheet pose potential impairment risk should business forecasts or competitive positioning deteriorate unexpectedly [valye_report_excerpt]. Thus managing liquidity extends beyond cash flow discipline into precise asset valuation exercises governed by evolving market conditions.

The Strategic Edge: Bundle Offerings, Backlog Growth, and Customer Stickiness

Central to Genasys’ competitive positioning is the synergy derived from bundling hardware equipment with complementary software licenses, maintenance plans, and bespoke development services [valye_report_excerpt]. This approach not only enhances revenue per customer but significantly raises barriers for client attrition by intertwining multiple performance obligations.

Backing this strategy is an order backlog valued at $61 million as of Q3 2025 that provides clear forward-looking visibility into demand trajectory [valye_report_excerpt]. Such backlog acts as an important signal affirming market acceptance of integrated offerings while underpinning future revenue streams subject to successful project execution.

By customizing solutions aligned closely with customer operational needs—particularly mission-critical early warning systems—the firm reinforces its moat amid intense sector competition that includes both traditional hardware vendors transitioning into software ecosystems and emerging pure-play tech companies targeting cloud-centric models.

However, reliance on backlog conversion also introduces execution risk should timelines slip or capital constraints limit fulfillment capacity — factors warranting close monitoring alongside commercial success indicators.

Risks, Mitigants, and the Road Ahead: Accounting Challenges and Market Competition

From regulatory filings [S1][S2], prominent risk factors persist around the application of complex accounting judgments under ASC 606 impacting reported financial outcomes reliability. The necessity to estimate completion percentages on long-term contracts or allocate transaction prices precisely among bundled elements demands frequent revisiting assumptions which may be influenced by evolving customer behavior or economic conditions.

Liquidity restrictions compound these vulnerabilities given the mismatch between sizable current liabilities versus available cash reserves—raising questions about funding options for ramping operations or pursuing growth initiatives without undue dilution or leverage increases [S1].

Competitive dynamics add another layer of uncertainty; Genasys competes against larger incumbents benefiting from scale advantages as well as agile newcomers exploiting rapid innovation cycles in both hardware design efficiencies and cloud-enabled software architectures [valye_report_excerpt].

Management has indicated steps addressing these headwinds—such as tighter working capital controls or prioritization of higher margin contract segments—but tangible offsets remain largely prospective requiring continued scrutiny [S2].

Earnings Analysis Q1 2026: Beats Amidst Pressure

The company’s Q1 2026 earnings report illustrates this delicate balance between top-line expansion juxtaposed with bottom-line struggles. Revenues exceeded consensus estimates signaling sustained market traction yet net losses persisted reflecting ongoing investments into growth areas alongside fixed cost absorption challenges [N1][N2][S2].

Management commentary during earnings calls highlighted optimism around backlog fulfillment pipeline while acknowledging volatility driven by timing differences inherent in multi-element contracts under ASC 606 intricacies [N2]. This underscores operational subtleties where beating headline numbers masks underlying margin compression factors attributable partly to accounting treatment nuances and partly to economic pressures such as component cost inflation or supply chain disruptions.

Investors should view these quarterly results through a prism acknowledging transient fluctuations within structural financial resilience issues still unresolved materially.

Investor Takeaways: Valuation, Moat Sustainability, and Execution Risks

For stakeholders evaluating Genasys' prospects beyond pure financial metrics lies an intersectional appraisal incorporating qualitative moat durability against quantitative balance sheet realities [valye_report_excerpt][F1][N1][S1]. The ability to maintain customer lock-in through bundled solution sophistication offers tangible long-term value if operational execution remains disciplined.

Nevertheless, valuation considerations must integrate liquidity constraints compounded by recurring negative earnings which inherently cap near-term upside absent clear inflections toward positive free cash flow generation.

Critical monitoring parameters include shifts in cash burn rates relative to backlog conversion velocity; adherence to stringent internal controls surrounding ASC 606 compliance given its outsized impact on reported results; plus sensitivity to macroeconomic factors influencing client spending patterns within critical infrastructure verticals served.

Ultimately Genasys embodies a case where product-service integration delivers differentiated market positioning tempered by financial hurdles mandating strategic focus on cash flow optimization coupled with transparent investor communications clarifying revenue recognition impacts.

Disclaimer: This analysis presents factual information synthesis based on public filings and news sources without offering investment advice or price projections.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments