McGraw Hill's Digital Evolution and Financial Resilience Amid Post-IPO Leadership Transition

McGraw Hill navigates the crossroads of its rich educational legacy and aggressive digital innovation against a backdrop of financial and regulatory challenges.

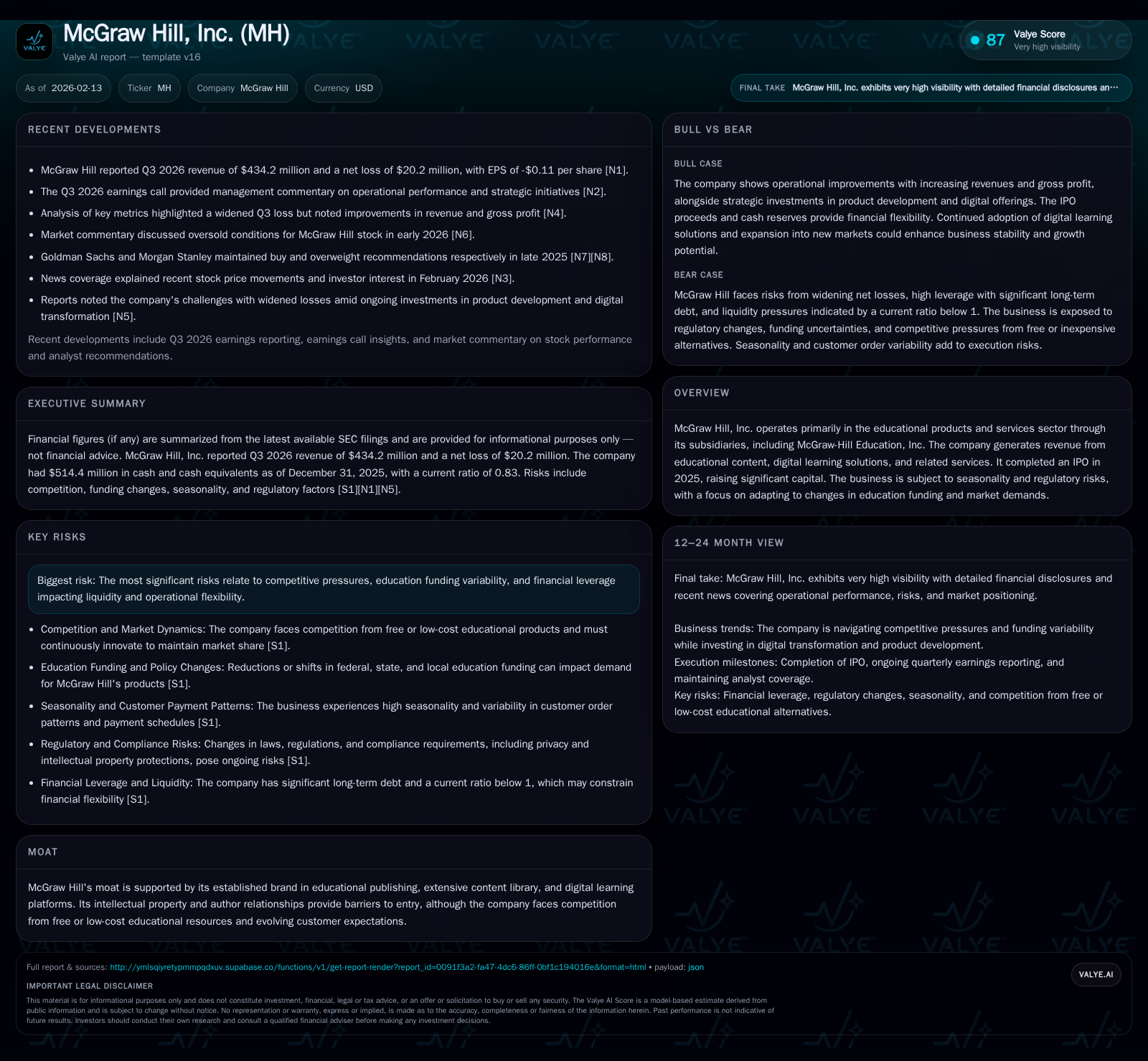

McGraw Hill, long a pillar in educational publishing, is accelerating its digital transformation while managing operational pressures visible in recent financial results. The transition from CEO Simon Allen to Philip Moyer signals potential strategic recalibration amid market competition and technology-driven change. The company’s moat, anchored by its intellectual property and robust digital platforms, faces challenges from free alternatives and shifting funding landscapes. Financially, McGraw Hill contends with seasonal revenue swings and leverage constraints post-IPO, while regulatory complexities add layers of risk shaping future priorities.

Legacy Meets Innovation: McGraw Hill’s Educational Heritage and Digital Pivot

McGraw Hill stands as one of the oldest and most recognizable names in education, boasting over 135 years of influence on learning worldwide. Historically synonymous with textbooks and printed educational materials, the company has decisively pivoted into the digital era by committing over $2 billion toward developing market-leading digital learning solutions. These investments have forged powerful platforms such as ALEKS that harness machine learning and data analytics to personalize education at scale.

This melding of deep content expertise with modern technology reflects a broader trend reshaping education technology: the drive toward adaptive learning powered by AI. By embedding learning science into product design—utilizing continuous feedback loops generated from user data—McGraw Hill sustains relevance among a diverse user base exceeding 60 million learners annually [S2]. This duality of heritage strength paired with tech innovation forms the foundational narrative driving the company's strategic positioning in an evolving landscape.

Decoding Q3 2026 Earnings: Growth Amid Operational Hurdles

In Q3 2026, McGraw Hill reported revenue growth to $434 million, up modestly from prior periods—signaling resilience in demand for its expanded digital offerings [N1][F1]. Yet this topline strength masked deeper operational complexities; net losses widened sharply to approximately $20.2 million for the quarter ended December 31, 2025 [F1], underscoring tensions between scaling efforts, investment intensity, and margin pressures.

Adjusted EBITDA trends reveal a similar dynamic where incremental gains are absorbed by higher operating expenditure largely linked to continued R&D spend and marketing investments needed to capture share in competitive digital marketplaces [N3][S2]. Seasonality further compounds these results given educational purchasing cycles tied closely to academic calendars that create front-loaded revenue inflows followed by leaner periods—a characteristic referred to internally as ‘seasonal tidal flows.’

Leadership Transition: From Simon Allen to Philip Moyer – What It Signals

December 2025 marked a pivotal moment with founder-era CEO Simon Allen announcing his retirement effective February 9, 2026. The Board swiftly appointed Philip Moyer as successor CEO [S2], who began his tenure alongside an $8 million restricted stock unit grant symbolizing confidence coupled with an expectation to drive sustained innovation while managing operational discipline.

Moyer's compensation structure includes eligibility for significant stock purchases aligned with restricted awards—indicative of alignment incentives geared towards long-term value creation within McGraw Hill’s controlled company framework. While details on Moyer's strategic vision remain emergent, this leadership change suggests cautious evolution rather than abrupt overhaul given Allen's continuing role as Chair [S2]. The transition underlines ongoing refinement of corporate culture integrating legacy knowledge with forward-looking digital ambitions.

Digital Learning Platforms: Investments, AI Integration, and Market Adaptation

At the heart of McGraw Hill’s transformation lies the continuous enhancement of flagship digital platforms like ALEKS—a product proven over 25 years that combines artificial intelligence with rigorous learning science principles [S2]. This platform exemplifies the company’s approach: iterative design powered by real-time data analytics enabling personalized instruction tailored to individual learner trajectories.

Such sophistication allows McGraw Hill to differentiate itself amidst proliferating edtech alternatives by emphasizing outcome-driven solutions rather than mere content delivery. The underpinning shared technology infrastructure supports scalable deployments across K-12, higher education, and professional sectors—areas targeted for expansion through innovation pipelines managed by roughly 300 software engineers [S2].

Generative AI capabilities further extend personalization beyond static content norms. However, balancing these technological advancements with usability remains critical as educators seek intuitive tools integrated smoothly into varied instructional contexts.

Moat and Competitive Pressures: Navigating Free Alternatives and Customer Expectations

McGraw Hill’s moat traditionally derives from a vast intellectual property library accumulated over decades alongside contractual relationships with celebrated authors and institutions. This serves as a fortress guarding against new entrants unable to match content breadth or brand trust.

Nevertheless, growing availability of free or very low-cost educational resources disrupts historical pricing paradigms—forcing McGraw Hill to justify premium pricing via demonstrable efficacy embedded in its adaptive platforms [N6][S2]. Customer expectations now extend beyond mere access toward seamless integration capabilities coupled with measurable learner impact.

Competition also manifests within proprietary offerings from large technology firms incorporating AI-driven tools disrupting standard curriculum models. Consequently, McGraw Hill must continuously innovate while safeguarding intellectual property protections against unauthorized copying or distribution as highlighted among risk factors [S2].

Financial Health Deep Dive: Liquidity, Leverage, and the Seasonal Revenue Cycle

The company's liquidity profile presents mixed signals—the current ratio stands at approximately 0.83 [F1], indicating tighter short-term asset coverage relative to liabilities than ideal benchmarks suggest. Cash reserves remain solid at over $514 million yet must contend with working capital demands intensified by seasonality effects typical across education markets where bulk orders cluster ahead of term starts.

Leverage concerns are accentuated by post-IPO capital structure dynamics; outstanding indebtedness constrains operational flexibility especially as reinvestment needs into R&D remain elevated [S2]. Management acknowledges these constraints openly within risk disclosures but views them as manageable via disciplined cash flow optimization strategies implemented during slower revenue quarters.

In essence, financial stewardship balances sustaining innovation momentum without jeopardizing solvency amid cyclic revenue intake fluctuations characteristic of textbook replacements transitioning to subscription-based digital models.

Regulatory Landscape and Funding Risks: The External Forces Shaping Strategy

Operating within complex governmental frameworks exposes McGraw Hill to multifaceted regulatory vulnerabilities ranging from variability in public education funding sources—both federal and state—to evolving privacy regulations governing student data [S2]. Additionally, political discourse around education policy reform injects uncertainty around budget allocations which can materially affect adoptions.

Further complicating matters are compliance demands such as General Accessibility Requirements (GAR), export controls impacting international sales channels, cybersecurity standards defending against hacking attempts detailed among risk factors [S2], plus ongoing litigation risks intrinsic to its global IP portfolio management.

These external forces necessitate agile strategy adaptations balancing proactive legal compliance initiatives without sacrificing competitive edge or slowing product deployment schedules fundamental to retaining institutional customer loyalty.

Future Outlook: Balancing R&D, Market Expansion, and Shareholder Value

Looking ahead, McGraw Hill faces the challenge of optimizing substantial R&D investments targeting enhanced AI functionalities alongside expanding geographic footprints primarily within professional training sectors aligned with healthcare and technical verticals [N4][N7][S2]. User endpoint growth targets remain ambitious yet realistic when weighed against competitive landscapes that prize scalability backed by evidence-based learning outcomes.

Simultaneously, shareholders face a governance environment defined by ‘controlled company’ status limiting conventional shareholder activism avenues while constraining near-term capital return policies notably absent dividends or stock repurchases [S2]. Thus value creation efforts emphasize reinvestment efficiency combined with measured market positioning strategies designed to preserve long-term competitive advantage without overstretching limited financial slack.

Investor’s Takeaway: Valuation Versus Risk in a Controlled Company Environment

Navigating McGraw Hill requires appreciation for intrinsic sector nuances blending traditional publishing heft with cutting-edge edtech innovation underpinned by AI-driven personalization promises juxtaposed against inherent risks linked to funding variability, legal exposures, competitive pressures from both established incumbents and emerging disruptors owning low-cost/free models [N6][N7][S2].

Investors must weigh volatile equity performance reflective of these interplay dynamics compounded under a controlled ownership regime curtailing typical shareholder influence mechanisms while deferring dividend returns indefinitely [S2]. Ultimately McGraw Hill embodies both opportunity seeded in intellectual property-rich foundations bolstered by technology investments as well as caution warranted given operational complexity reflective in recent widened losses despite top-line growth signals.

This analysis synthesizes publicly available information without presenting investment recommendations or price guidance. Readers should consider additional sources and professional advice before making financial decisions related to McGraw Hill or industry sectors discussed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments