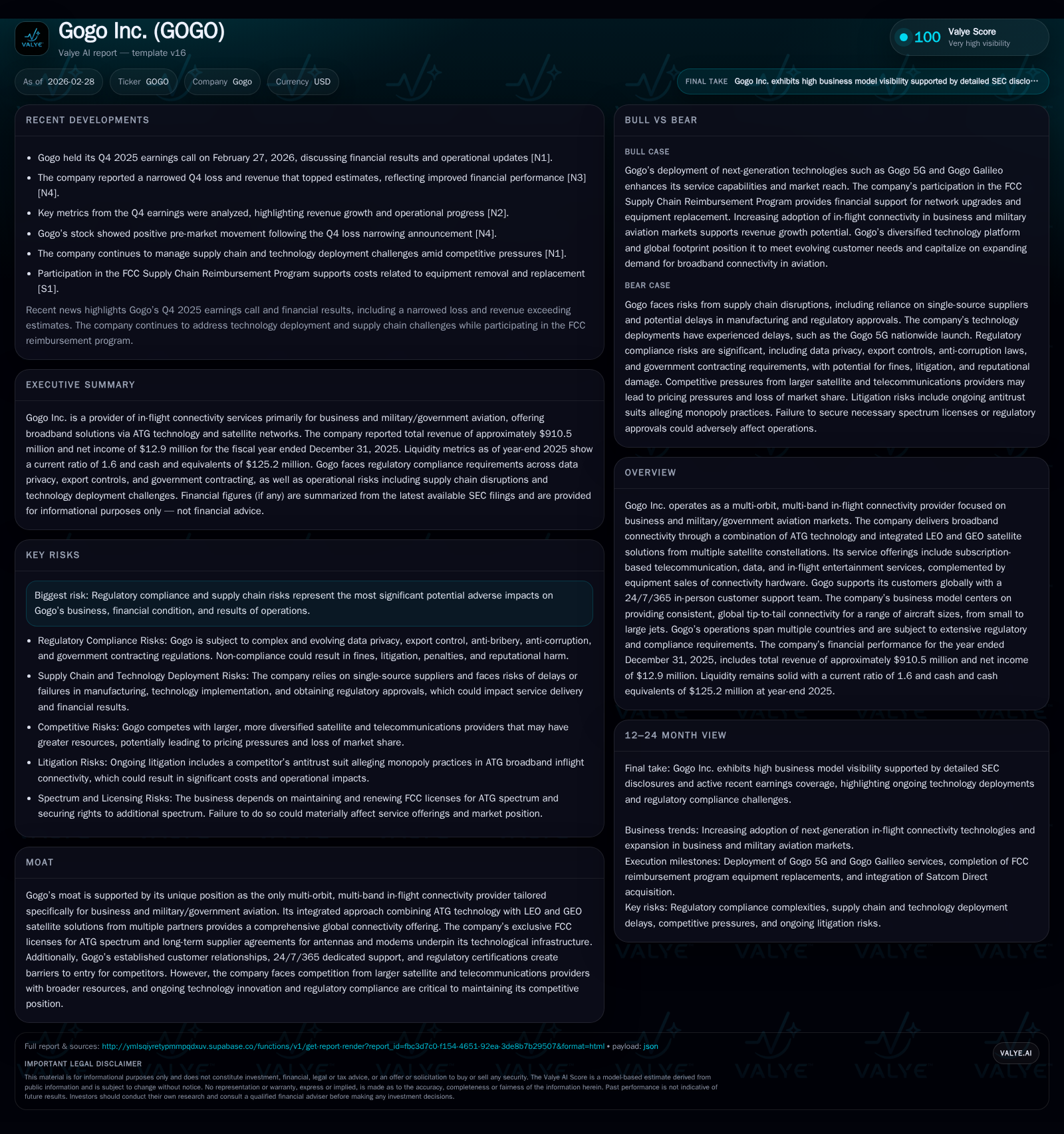

Gogo Inc. Charts Growth Through Satellite-Powered Aviation Connectivity

Gogo leverages a unique multi-orbit satellite and ATG network to drive growth in business and government aviation connectivity.

Gogo Inc. has transitioned from a primarily Air-to-Ground (ATG) connectivity provider to a comprehensive multi-orbit satellite solution integrator, combining legacy ATG technology with low-earth orbit (LEO) and geostationary earth orbit (GEO) satellite services. This hybrid approach has supported robust revenue growth and a sharp rise in operating income through 2025, although net income remains relatively flat due to financing costs and regulatory challenges. The company maintains a substantial debt load that constrains financial flexibility but is investing heavily in expanding its service capabilities amid evolving industry demand. Regulatory compliance, supply chain stability, and customer contract renewal dynamics remain key risks that could shape Gogo's future trajectory.

Historical Growth: Revenue and Operating Income Shifts Over the Last Decade

Since its earlier years focused on Air-to-Ground (ATG) broadband services for business aircraft, Gogo Inc. has demonstrated notable top-line growth culminating in a revenue level of approximately $188 million as far back as 2017 [F1]. More recently, from 2023 to 2025, Gogo has shown accelerated momentum with a reported 17.5% year-over-year increase in revenue by the end of fiscal 2025 [F1]. This uptrend coincides with intensifying deployment of multi-orbit satellite solutions complementing its traditional ATG platform.

Profitability exhibits greater volatility yet reflects operational leverage benefits. Operating income soared by over 122% year-over-year to about $114 million at FY2025-end compared to roughly $51 million in FY2024 [F1]. This surge outpaces revenue growth rates, suggesting disciplined cost management and scaling benefits. However, net income remains comparatively muted at $12.9 million for FY2025, declining slightly by 6% year-over-year [F1], indicating elevated interest expenses and other non-operating items restraining bottom-line expansion.

Table: Gogo Inc. Historical Financial Metrics (2017-2025)

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 13 | 124 | 114 | 59 | -6.0% |

| 2024 | 14 | 41 | 51 | 14 | -90.6% |

| 2023 | 146 | 124 | 16 | +58.2% | |

| 2022 | 92 | 142 | 44 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 65 | 12.8 |

| 2024 | 33 | 28 | 19.8 |

| 2023 | 5 | 357.7 | |

| 2022 | 18 | -90.4 |

Source: SEC companyfacts cache [F1].

Note: Operating income figures skip some years due to reporting granularity; net income reflects mostly stable results despite operating leverage.

Evolution of Technology: Integrating Multi-Orbit Satellite Solutions with ATG Legacy

At its core, Gogo's competitive advantage derives from blending an established FCC Air-to-Ground spectrum license—allowing exclusive operation of terrestrial cell sites—with cutting-edge multi-orbit interoperability architecture incorporating Low Earth Orbit (LEO) satellites and Geostationary Earth Orbit (GEO) constellations [S1]. This dual-mode approach mitigates the long-standing aviation bandwidth constraints endemic to legacy systems by dynamically routing traffic between terrestrial links for continental coverage and satellites for global reach.

This integration requires proprietary hardware—antennas and modems developed under long-term supplier arrangements—that can seamlessly transition connections across ATG and multiple satellite bands without user disruption . This technology stack supports differentiated offerings including Gogo’s emerging Gogo Galileo system leveraging Galileo satellites for precise global positioning and improved connectivity reliability [S1]. Implementing such a complex multi-orbit constellation solution demands significant R&D investment but creates formidable entry barriers against larger telecommunications or single-mode satellite providers unable to match this global tip-to-tail coverage.

Revenue Mix and Customer Base Dynamics in Business and Government Aviation

Subscription-based telecommunication services now account for approximately 84% of total revenues as of FY2025 [S1][F1], underscoring the strategic emphasis on recurring customer streams largely composed of individual aircraft owners or fractional operators with contracts typically one to three years in duration. Such contract lengths introduce substantial renewal risk given market competition offering alternative or lower-cost connectivity options [S1]. Fleet-wide agreements are less prevalent but tend to enhance revenue visibility when present.

Equipment sales comprise roughly 15% of annual revenue, principally driven through OEMs and aftermarket dealer channels under at-will contracts that can be terminated on short notice by either party [S1][F1]. More than ninety percent of equipment revenues have been sourced via these partnerships, which exposes Gogo to volume unpredictability given non-binding production schedules and cost overruns absorbed internally when developing next-generation hardware [S1]. Certain OEM contracts contain clauses allowing retroactive pricing adjustments favoring distribution partners which may cap margin expansion potential.

Financial Health and Capital Structure Under Leverage Constraints

Carrying approximately $848 million of consolidated debt comprised primarily of two term loan facilities—the $601 million drawn under the original 2021 Term Loan Facility and an additional $247 million under the HPS Term Loan Facility initiated in late 2024—Gogo operates within a highly leveraged framework with stringent credit agreement covenants governing incurrence ratios and debt service obligations [S1][S4][S9]. The Credit Agreements restrict dividend payments, incurrence of additional indebtedness beyond specified thresholds, asset sales freedoms, merger prospects, and affiliate transactions unless explicit financial tests are met [S5][S6][S10].

Interest expense burden is variable-rate linked with floors on term SOFR rates plus fixed margins ranging from roughly 3.75%-6%, partially mitigated by purchased interest rate caps covering a portion of exposure through mid-2027 [S4][S14]. Still, rising rate environments pose material risk to cash flow sustainability given operating cash flows must prioritize principal plus interest repayments reducing capital openness for network investment or shareholder distributions.

Assessing Growth Catalysts and Headwinds: Market Demand and Regulatory Risks

The primary growth drivers rest on continuing expansion of global business aviation activity coupled with increasing digital reliance onboard fleet assets demanding uninterrupted high-bandwidth connectivity irrespective of geography . Military/government aviation segments further bolster demand given stringent requirements for secure communications worldwide.

On the flip side, regulatory compliance introduces complex challenges: evolving data privacy regimes impose steep notification duties along with expensive security safeguard implementations that may not uniformly shield against cyber intrusions or inadvertent breaches [S17]. Spectrum management entails heightened scrutiny regarding usage rights subject to FCC licensing trajectories amid antitrust lawsuits alleging monopolistic practices over the ATG broadband space filed against Gogo since late 2024 [S19][S20]. These risks carry reputational consequences alongside potential legal costs.

Outlook and Analyst Watch-points for Future Milestones

Although explicit corporate guidance remains sparse as per recent earnings calls through early 2026 [N1][N3], investor attention should focus sharply on metrics such as:

- Scalability pace of Gogo's next-generation satellites deployments including Gogo Galileo rollouts,

- Fleet penetration velocity among regional versus large cabin jets,

- EBITDA margins improvement trends reflecting mix-shift toward higher-margin subscription services,

- Refinements in loss narrowing expected from recent quarterly operating results suggestive of trajectory toward consistent profitability [N5].

Technology adoption speed combined with maintenance or improvement in customer contract renewal rates will be key bellwethers.

Capital Allocation Strategy: Cash Flow Generation, Dividends, and Buybacks

Operating cash flow exhibited remarkable growth doubling from approximately $41 million in FY2024 to about $124 million in FY2025 while capital expenditures simultaneously ballooned over threefold reaching nearly $60 million as the company invests aggressively into network infrastructure scaling capacity across ATG and satellite layers [F1][S22]. Despite higher capex spending diluting free cash flow somewhat, positive free cash flow near $65 million was generated showcasing underlying cash-generative resilience even amidst funding frontier innovations.

Share repurchases paused entirely during FY2025 contrasting with prior buybacks aggregating over $33 million completed the year before — implying prioritization of deleveraging or capex needs over equity returns currently [F1]. Dividends have remained consistent though finance disclosures indicate tight board discretion governed by covenant limits restricting distribution freedom absent financial improvement [S4][S16]. Return on equity approximated at around 12.8% signals moderate efficiency capital use from an equity perspective given ongoing reinvestment demands.

This analysis synthesizes publicly filed financial data together with disclosed strategic insights as per recent SEC filings and earnings commentary without providing investment recommendations. The reader should consider this document as informational only regarding Gogo Inc.’s business progressions within the aviation connectivity sector into early 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments