Global Payments Inc. Seeks Renewal After Major Structural Shift and Strategic Trades

Global Payments' comprehensive business transformation, including the Worldpay acquisition and Issuer Solutions divestiture, redefines its trajectory amid industry challenges.

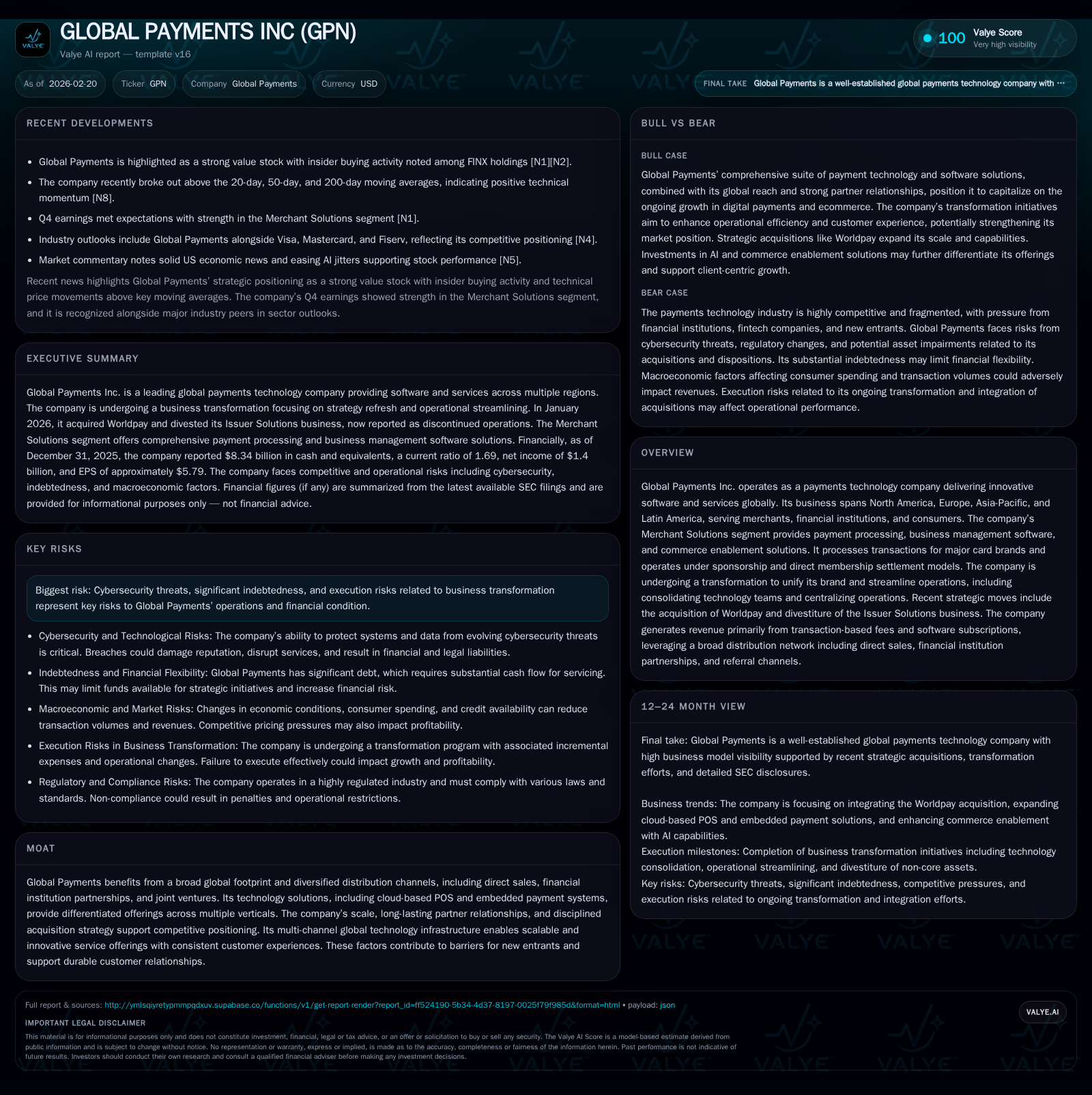

Global Payments Inc. has undergone a profound transformation since 2024, marked by a holistic business model overhaul and pivotal transactions such as acquiring Worldpay while divesting its Issuer Solutions unit. These moves signify a strategic sharpening towards merchant-focused payment solutions with streamlined technology and operations. Despite a striking 52% revenue decline in 2025 influenced by portfolio changes, the company maintained robust profitability and cash flow. Looking ahead, success hinges on efficient integration, managing ongoing transformation expenses, navigating a complex regulatory landscape, and capitalizing on growth from cloud-based software subscriptions and embedded payment technologies.

Historical Growth Dynamics: Scale Through Consolidation and Innovation

Global Payments Inc.'s recent financial history reflects dramatic shifts driven by transformative acquisitions and divestitures. After a rapid growth phase leading up to 2024—demonstrated by operating income rising from $640 million in 2022 to $2.33 billion in 2024—the company experienced a stark reversal in top-line figures in 2025. Annual revenues plunged approximately 52% year-over-year due to substantial portfolio reshuffling following the massive acquisition of Worldpay coupled with the simultaneous divestiture of its Issuer Solutions business [F1]. This repositioning sharpened focus on merchant-oriented payment processing but led to temporary decreases in reported revenue.

Despite this contraction in sales, operational income remained robust at nearly $1.75 billion in 2025 (down about 25% YoY), highlighting enhanced margin control amid transitional pressures [F1]. This profitability resilience partly owes to the consolidation of legacy businesses and streamlining initiatives carried out since 2024.

Historical performance (annual)

| FY | Net ($mm) | CFO ($bn) | OpInc ($bn) | Net YoY |

|---|---|---|---|---|

| 2025 | 1400 | 2.7 | 1.8 | -10.8% |

| 2024 | 1570 | 3.5 | 2.3 | +59.2% |

| 2023 | 986 | 2.2 | 1.7 | +784.6% |

| 2022 | 111 | 2.2 | 0.6 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Capex, Div, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($bn) | ROE% |

|---|---|---|

| 2025 | 1.2 | 6.1 |

| 2024 | 1.6 | 7.0 |

| 2023 | 0.4 | 4.3 |

| 2022 | 2.9 | 0.5 |

Source: SEC companyfacts cache [F1].

*Annual revenue figures post-2018 are not directly provided in available XBRL data; YoY inferred from related disclosures [F1]. Dividends paid data is limited post-2019.

Transformation Initiatives Streamlining Operations and Technology

Starting in early 2024, Global Payments embarked on a comprehensive strategic review aimed at consolidating its vast portfolio into a unified global operating platform [S1]. This initiative entailed integrating disparate technology teams under common leadership—a move targeted at accelerating product development cycles with enhanced customer focus.

Operational centralization includes harmonizing support functions to better service clients and reduce overhead costs, reinforcing the company's competitive edge through superior customer experience consistency worldwide [S1]. The ambition to solidify the Global Payments brand identity across various acquired assets promises marketing clarity and reduced internal complexity.

Notably, investment in scalable cloud-native point-of-sale (POS) platforms dovetails with this organizational consolidation, reflecting strategic pivoting toward software-enabled commerce solutions favored by modern merchants [S8].

Impact of Worldpay Acquisition and Issuer Solutions Divestiture

January 2026 marked two landmark transactions for Global Payments: the full acquisition of Worldpay Holdco LLC from Fidelity National Information Services (FIS) and GTCR for approximately $6.2 billion in cash plus over 43 million GPN shares; simultaneously, it divested its Issuer Solutions business back to FIS for roughly $7.7 billion cash consideration along with ownership interest exchanges [S1][S4].

These parallel deals underscore a deliberate exit from issuer-side digital processing toward intensified focus on merchant solutions encompassing payment acceptance technologies worldwide. Post-acquisition reporting aligned segment disclosures accordingly to reflect this modernization [S4].

The Worldpay purchase enhances scale significantly within the payments technology space while relying on transaction-based pricing—a function of volumes processed—and subscription fees derived from embedded software offerings that fortify recurring revenue streams [S8][S4].

Current Financial Performance: Revenue Decline Amidst Expansion

The paradoxical FY2025 financial results demonstrate Global Payments maintaining solid profitability despite top-line pressures induced by structural changes. Operating income at $1.75 billion—against dramatically lower revenues—evinces effective margin management amidst elevated expenses tied to transformational initiatives such as integration costs and asset amortization revisitations [F1][N1].

Management's commentary emphasizes robust momentum within the Merchant Solutions segment powered by sustained card transaction volumes and resiliency of cloud-based software subscriptions underpinning fee stability versus precedent legacy fee compression trends [N1]. This suggests an enduring core generating positive cash flow even amid broader market uncertainties.

Evolving Revenue Model: Transition From Legacy Fees to Software Subscription Focus

Central to Global Payments’ reshaped strategy is shifting revenue mix away from volatile transaction-dependent interchange fees toward stable subscription models anchored by advanced cloud POS software solutions labeled under the "Genius" brand umbrella globally [S8][S4].

Embedded payments integrated within diverse vertical market management platforms—including education, real estate, hospitality, among others—form chronic revenue streams supplementing typical transaction fees [S8]. Leveraging expansive distribution channels—from direct sales teams renowned for relationship strength to financial institution partnerships—further facilitates penetration into both new geographies and sectors.

This dual approach of recurring SaaS-like income coupled with variable transaction fees exemplifies modern payment tech enterprises seeking durability against fluctuations inherent in pure transactional pricing mechanics.

Capital Allocation Strategy: Managing Debt, Buybacks, and Dividends

Following costly acquisitions primarily financed through debt issuance—the company ended FY2025 with cash & equivalents totaling roughly $8.34 billion alongside current assets at $12.6 billion against liabilities near $7.46 billion yielding a current ratio around 1.69 indicating liquidity adequacy [F1].

Despite high leverage loads consequent from the Worldpay deal ($6+ billion cash outlay), Global Payments continued capital return programs including nearly $1.19 billion share repurchases in FY2025 complemented by consistent dividends (data post-2019 limited) illustrating balancing shareholder interests against deleveraging priorities [F1][S3].

Approximate return on equity stands near a moderate ~6%, reflective of transient integration-related earnings pressure but affirming positive capital productivity considering transformation phase adversity [F1].

Regulatory Environment and Cybersecurity Challenges

Global Payments operates under increasingly complex regulatory oversight spanning U.S., European Union, UK, Asia-Pacific and Latin American jurisdictions given its extensive footprint [S5][S6][S10]. Its subsidiaries hold multiple payment institution licenses—subject to evolving directives like the EU’s Digital Operational Resilience Act effective since early 2025 enforcing stringent ICT risk controls particularly around cybersecurity safety nets [S25].

Privacy laws such as GDPR, GLBA and expanding state-level U.S regulations compel continuous adaptation especially concerning data governance practices impacting cost structures [S16]. The advent of artificial intelligence adoption introduces further layers of uncertainty around compliance burdens relating to new AI-specific rules emerging globally that could affect innovation pipelines if not adeptly managed [S27].

Cybersecurity remains a critical risk domain encompassing incident prevention responsibility not only internally but extending into vendor ecosystems where breaches can cause reputational damage, lost merchant trust, fines or legal consequences severely disrupting business continuity [S26][S29]. The company has invested materially into information security infrastructure but warns of persistent vulnerability given dynamic threat landscapes.

Outlook: Key Growth Drivers, Operational Hurdles, and Market Indicators to Watch

Going forward, critical performance indicators include realization of merger synergies anticipated into mid-2027 timeframe as Global Payments completes consolidation efforts without service disruptions or customer attrition [N3][N1][S1]. Monitoring operating expense trends will indicate whether transformational overheads are subsiding as projected or remain extended pressures.

Merchant solutions transaction volumes represent real-time barometers of underlying commerce ecosystem health influencing fee revenues while cloud POS subscription uptake rates will validate recurring model effectiveness.

Externally, geopolitical tensions or evolving fintech competitive dynamics might pressure pricing power or client retention necessitating agile innovation adoption backed by well-integrated backend infrastructure suites.

Regulatory developments especially regarding cross-border trade compliance or AI governance rules warrant vigilance due diligence given potential escalations causing investment recalibrations or operational constraints.

This analysis synthesizes SEC filings and market disclosures up through February 2026 without offering investment advice or price-related forecasts. Readers should consider inherent uncertainties attached to sector transformations and global economic factors impacting merchant payments technologies alongside ongoing corporate restructuring challenges.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments