Hyatt Hotels Corp: Strategic Resilience Navigating 2025’s Hospitality Sector Volatility

Despite ongoing hospitality headwinds, Hyatt’s latest financials and brand portfolio reveal nuanced strengths and liquidity challenges.

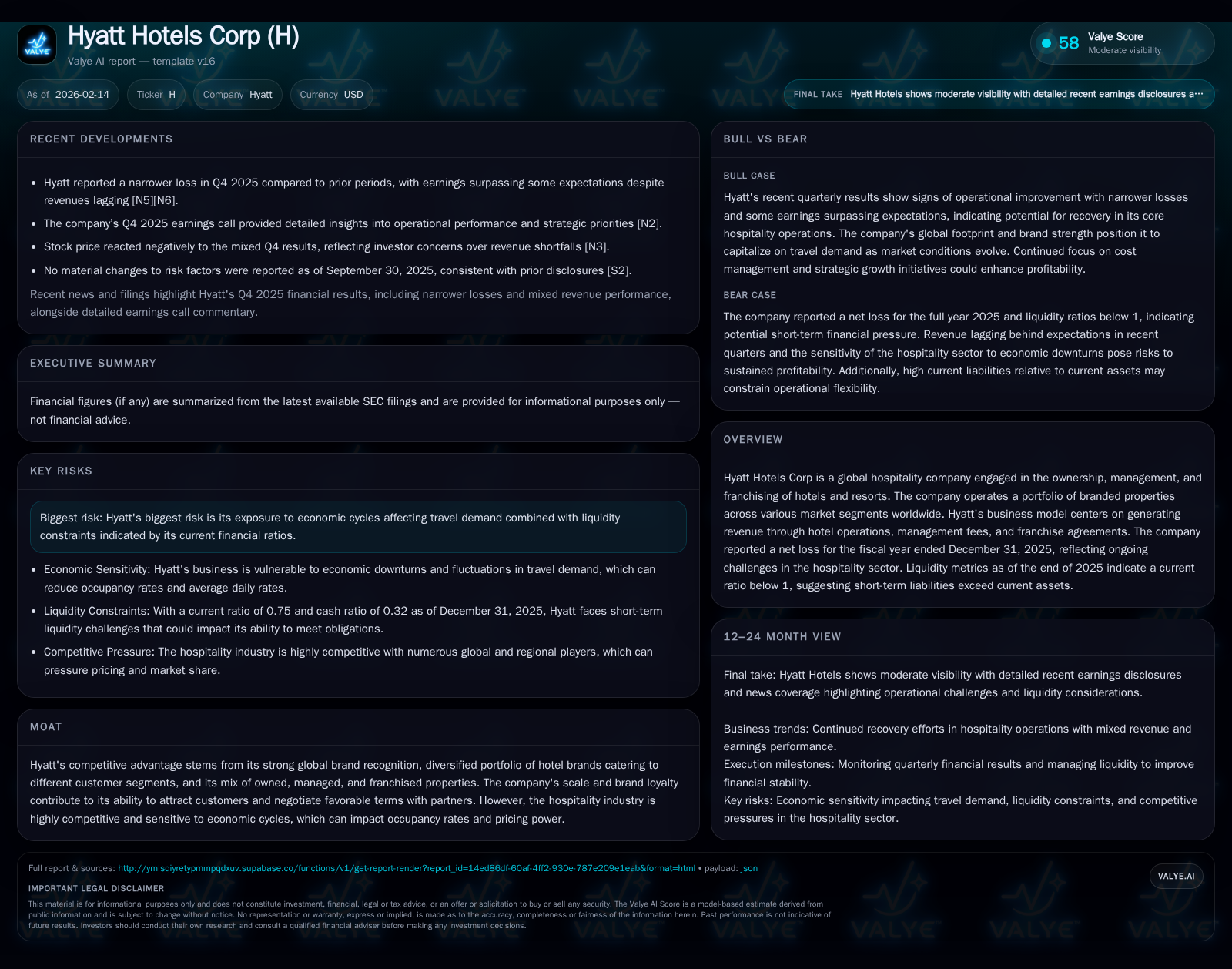

The global hospitality industry continues grappling with post-pandemic volatility and economic uncertainty, creating a demanding backdrop for major players like Hyatt Hotels Corp. In fiscal 2025, Hyatt reported a narrower net loss amid mixed revenue performance, reflecting the sector’s uneven recovery. The company’s diversified brand portfolio and hybrid ownership-management-franchise model provide resilience, though liquidity constraints highlight ongoing operational pressures. As Hyatt moves into 2026, management’s strategic focus on cost control and fee growth underscores efforts to manage cyclical risks while leveraging brand strength.

Hospitality Industry Volatility Sets the Stage

The global hospitality sector remains one of the most volatile post-pandemic industries, caught between recovering travel demand and lingering economic uncertainties. Inflationary pressures, geopolitical tensions, and fluctuating consumer confidence continue to shape travel patterns unevenly. Entering 2026, this environment demands that hotel companies like Hyatt Hotels Corp navigate complex headwinds impacting occupancy rates, room pricing, and ancillary revenue streams.

Against this backdrop, Hyatt's recent financial disclosures offer a window into how a large global operator balances resilience amid ongoing sector turbulence. The fiscal year ended December 31, 2025 blended modest operational improvements with significant challenges reflected in profitability and liquidity metrics.

2025 Financial Performance: Narrowing Losses in a Demanding Market

Hyatt's full-year 2025 results culminated in a net loss of approximately $52 million [F1], signaling that while progress was made from earlier pandemic-impacted years, profitability remains elusive. Notably, Q4 exhibited a narrower loss compared to prior quarters [N9], suggesting some traction in operational recovery.

Earnings per share outperformed expectations during the quarter even as revenues fell short of consensus forecasts [N3]. This dichotomy points to increased cost discipline or improved margin management offsetting top-line softness. However, the sustained net loss across the year underscores that underlying market dynamics have yet to fully normalize for Hyatt.

This financial outcome fits within an industry-wide narrative where occupancy gains are tempered by uneven regional travel rebounds and softer group/convention business segments—areas critical for upscale brands such as Hyatt.

Revenue and Fee Breakdown: Dissecting the Core Drivers

Hyatt’s revenue composition reveals an evolving interplay between owned hotel operations and increasingly important fee-related income streams delivered through management contracts and franchising arrangements [S1][F1].

Base management fees, incentive fees linked to property performance, along with franchise fees constitute substantial portions of Hyatt’s total fee pool. While owned properties generate direct room revenues subject to variable operating costs, fee income offers higher margin stability less sensitive to capital expenditure demands.

Despite this strategic tilt towards asset-light segments to mitigate capital intensity risk, the recent quarterly revenue miss [N3] indicates pressure on both operational volumes and fee growth catalysts. Industry-wide softness in transient leisure travel during select periods contributes to this weakness. Nonetheless, franchise-based royalties tend to provide steady cash flows which cushions overall revenue volatility.

Balance Sheet Under Pressure: Liquidity and Leverage Challenges

Analysis of Hyatt's balance sheet as of December 31, 2025 reveals current assets totaling approximately $2.18 billion against current liabilities near $2.89 billion [F1]. This yields a current ratio close to 0.75—a level below the conventional benchmark of one—highlighting potential short-term solvency constraints.

Cash and equivalents stood at about $787 million [F1], indicating substantial liquidity reserves but still underscored by immediate obligations outpacing working capital. This imbalance raises questions about operational flexibility especially if travel demand disruptions persist or escalate.

Such liquidity pressure is not uncommon in hospitality companies with extensive lease or debt commitments compounded by cyclical revenue declines. Hyatt’s management must therefore prioritize efficient working capital management alongside exploring refinancing or capital raising options as needed.

Brand Portfolio and Operational Model: Strengths Amidst Competition

A cornerstone of Hyatt’s moat lies in its diversified hotel brand portfolio spanning luxury (Park Hyatt), upscale (Hyatt Regency), lifestyle (Andaz), select service (Hyatt Place), among others [valye_report_excerpt]. This segmentation allows tailored offerings across different traveler demographics—from corporate customers to millennials seeking boutique experiences.

Crucially, Hyatt operates through a hybrid model involving direct ownership of some properties complemented by managed hotels and franchises globally. This model facilitates scalability without extensive capital deployment across all locations while maintaining control over brand standards via management agreements.

The combination positions Hyatt advantageously within a highly fragmented hospitality market where brand differentiation and customer loyalty can drive pricing power even in pressured environments.

Economic Cycles and Travel Demand Exposure: Industry Risks Materialized

Hyatt explicitly recognizes its exposure to economic cycles—travel demand being closely linked to consumer discretionary spending patterns—which have crystalized as risks during recent reporting periods [valye_report_excerpt][S2].

While no new material risk factors emerged as of late 2025 filings [S2], financial impacts interrogate these vulnerabilities with revenue misses and net losses reflecting dampened global travel sentiment during parts of the year.

Corporate travel hesitancy due to recession fears or remote work persistence further complicates demand recovery scenarios affecting midweek occupancy traditionally lucrative for large hotels.

This sensitivity underscores that external macroeconomic factors remain key determinants for Hyatt's financial trajectory despite robust brand fundamentals.

Management Commentary and Strategic Initiatives from Q4 Call Insights

Insights gleaned from Hyatt's Q4 2025 earnings call emphasize management’s proactive stance addressing prevailing challenges [N2][N7][N8].

Executives detailed tactical cost containment measures alongside prioritization of fee-based revenue growth through pipeline expansion in managed/franchised locations. Capital expenditure spending was carefully calibrated aiming at selective reinvestments supporting long-term competitiveness rather than broad expansion.

Moreover, management reaffirmed focus on enhancing operational efficiencies within owned hotels amid labor cost inflation pressures.

Wall Street outlooks expressed cautious optimism ahead of these results [N6][N8], underscoring belief in sustained improvement tempered by attentive monitoring of travel consumption trends globally.

Valuing Hyatt’s Moat: Brand Loyalty and Scale in an Uncertain Landscape

Hyatt's competitive moats manifest through well-established global brand equity combined with an asset-light operational footprint which generally offers more consistent cash flow profiles than purely owned real estate models [valye_report_excerpt].

Nonetheless, liquidity pressures expose vulnerabilities as cyclical downturns limit pricing leverage impacting base/incentive fees tied to property performance metrics.

Continued investment in loyalty programs enhances customer retention dynamics which may help buffer market dislocations but debt levels necessitate vigilant financial stewardship.

Hence, while brand strength affords notable advantages versus smaller competitors or independent operators, sustaining this moat requires balancing growth ambitions with prudent balance sheet management under fluctuating economic conditions.

Looking Ahead: Forecasts, Liquidity Strategies, and Market Expectations

Entering FY26, analysts project improving earnings trajectories premised on gradual normalization of global travel patterns [N6][N8]. Yet consensus reflects caution about near-term volatility given inflationary risks potentially constraining discretionary spend outside core leisure clientele segments.

Liquidity optimization strategies will likely remain front-and-center including possible deleveraging maneuvers or refinancings intended to elevate the current ratio closer toward healthy thresholds enhancing capital structure resilience.

Operational priorities could include further emphasis on fee segment enhancements via new partnerships or brand extensions targeting emerging lodging preferences post-pandemic.

In sum, Hyatt stands at an inflection point where foundational strengths meet real-world cyclicality requiring astute strategic execution along multiple fronts to restore sustainable profitability amid an inherently uncertain hospitality landscape.

This analysis is based on publicly available data as of February 14, 2026. It is intended for informational purposes only without any investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments